After 24 years, Alibaba (NYSE: BABA and HKEX: 9988) is evolving from a single company into a new governance model of ŕ+6+N" in which major business groups and various companies have independent operations. ŕ" represents Alibaba Group's holding company, Ś" refers to six major business groups - Cloud Intelligence Group, Taobao and Tmall Group, Local Services Group, Alibaba International Digital Commerce (AIDC) Group, Cainiao Smart Logistics Network Limited, and Digital Media and Entertainment Group, and "N" refers to various businesses such as Alibaba Health, Sun Art Retail, and Freshippo. Each entity in the Ś+N" will establish its own board of directors that will provide oversight and support to the chief executive officer of the business.

Starting from the quarter ended June 30 2023, Alibaba has implemented a new organizational and governance structure. The six major business groups are: Taobao and Tmall Group, which includes Taobao, Tmall, Xianyu, 1688.com and other businesses; Alibaba International Digital Commerce Group, which includes Lazada, AliExpress, Trendyol, Alibaba.com and other businesses; Local Services Group, which mainly includes the "To-Home" business of Ele.me and the "ToDestination" business of Amap; Cainiao Smart Logistics Network Limited; Cloud Intelligence Group, which includes Alibaba Cloud, DingTalk and other businesses; and Digital Media and Entertainment Group, which includes Youku, Damai and Alibaba Pictures.

1QFY2024, 4QFY2023 and FY2023 results review

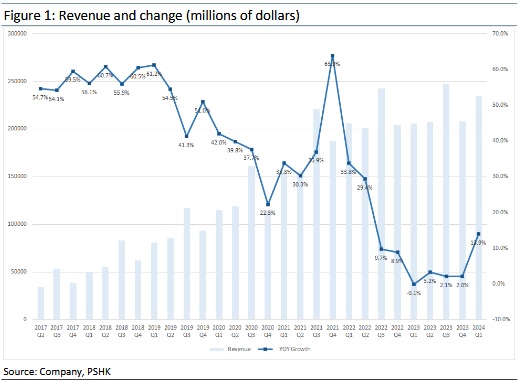

In FY2023, revenue was RMB868,687 million, an increase of 2% YoY. In FY2023, revenue was RMB868,687 million, an increase of 2% YoY. Adjusted EBITA increased 13% YoY to RMB147,911 million. Net income attributable to ordinary shareholders was RMB72,509 million, showing YoY increases of 17%. Non-GAAP net income was RMB141,379 million, an increase of 4% YoY.

In the quarter ended March 31, 2023 (4QFY2023), revenue was RMB208,200 million, an increase of 2% YoY. Adjusted EBITA increased by 60% YoY to RMB25,280 million. Net income attributable to ordinary shareholders was RMB23,516 million, turning a loss into a profit. Non-GAAP net income was RMB27,375 million, an increase of 38% YoY.

In the quarter ended June 30, 2023 (1QFY2024), revenue was RMB234,156 million, an increase of 14% YoY, which was better than the consensus. Adjusted EBITA increased 32% YoY to RMB45,371 million. Net income attributable to ordinary shareholders was RMB34,332 million, an increase of 51 YoY. Non-GAAP net income was RMB44,922 million, an increase of 48% year-over-year, which was also better than the consensus.

By segments, China commerce segment mainly includes China commerce retail businesses such as Taobao, Tmall, Taobao Deals, Taocaicai, Freshippo, Tmall Supermarket, Sun Art, Tmall Global and Alibaba Health, as well as wholesale business including 1688.com. Revenue from China commerce in 4QFY2023 was RMB136,073 million, a decrease of 3% YoY. The online physical goods GMV on Taobao and Tmall, excluding unpaid orders, declined mid-single digit year over year. China's consumption gradually recovered throughout the quarter ended March 31, 2023. In the month of March, online physical goods GMV growth on Taobao and Tmall, excluding unpaid orders, turned positive, driven by strong growth of fashion & accessories and healthcare categories. During the quarter, both Taobao Deals and Taocaicai continued to narrow losses YoY. Paid GMV ofM2C products grew 26% YoY on Taobao and Taobao Deals. For the twelve months ended March 31, 2023, 62% of Taocaicai's annual active consumers were first-time fresh produce buyers on our various platforms. Direct sales and others revenue was RMB71,788 million, decreasing slightly by 1% YoY, mainly due to decrease in offline store sales, which was negatively affected by COVID-19 disruption in January and seasonal volatility from an earlier Chinese New Year, as well as normalizing grocery demand due to decrease in consumer hoarding behavior post-COVID-19. Worth noting, Freshippo continued to strengthen its merchandising capabilities and improve its operating efficiency that resulted in positive operating results.

Revenue from International Commerce in 4QFY2023 was RMB18,541 million, a decrease of 3% YoY. The International commerce retail businesses include Lazada, AliExpress, Trendyol and Daraz platforms. The combined order volume of these businesses grew 15% YoY. The adjusted EBITA was a loss of RMB2,330 million, compared to a loss of RMB2,563 million in the same quarter of 2022.

Revenue from Local consumer services, which includes "To-Home" and "To-Destination" businesses such as Ele.me, Amap and Fliggy, was RMB12,549 million in 4QFY2023, an increase of 17% YoY. Starting in February, Ele.me's GMV growth and order growth substantially increased due to improving consumer demand, increasing number of active merchants and effective scaling of delivery capacity. The adjusted EBITA was a loss of RMB4,153 million, compared to a loss of RMB5,568 million in the same quarter of 2022.

Revenue from Cainiao, after inter-segment elimination, grew 18% year-over-year to RMB13,619 million in 4QFY2023, primarily driven by increasing revenue per order from international fulfillment solution services as well as increasing demand for consumer logistics services. In this quarter, 72% of Cainiao's total revenue was generated from external customers. Cainiao adjusted EBITA was a loss of RMB319 million, compared to a loss of RMB912 million in the same quarter of 2022.

Revenue from Cloud segment, after inter-segment elimination, was RMB18,582 million in 4QFY2023, a decline of 2% YoY. The decrease in revenue of Cloud segment reflected delays in delivery of hybrid cloud projects given the COVID-19 resurgence in January and normalization of CDN demand compared to the same period last year. During the quarter, revenue from non-internet industries grew healthily, driven by financial services, retail, media and automobile industries. Revenue contribution from non-Internet industries to Cloud segment revenue was 55%. Cloud adjusted EBITA was RMB385 million, grew 39% YoY.

Revenue from our Digital media and entertainment segment was RMB8,273 million, an increase of 3% YoY. Youku's total subscription revenue grew 13% year-over-year, primarily driven by increasing ARPU as well as benefiting from high-quality original content such as Who Is He and The Blood of Youth. Digital media and entertainment adjusted EBITA was a loss of RMB1,102 million, compared to a loss of RMB1,966 million in the same quarter of 2022.

Revenue from Innovation initiatives and others was RMB563 million, an increase of 47% YoY. The adjusted EBITA was a loss of RMB1,830 million, compared to a loss of RMB2,452 million in the same quarter of 2022.

1QFY2024 results growth momentum and profit margins improved

In 1QFY2024, Revenue from Taobao and Tmall Group was RMB114,953 million, an increase of 12% YoY. Among, revenue from China commerce retail business was RMB109,828 million, an increase of 13% YoY. Customer management revenue increased by 10% year-over-year, primarily due to the increase in merchant's willingness to invest in advertising and increase in online physical goods GMV generated on Taobao and Tmall, excluding unpaid order. The growth also reflected a successful 6.18 Shopping Festival that generated solid growth in order volume and average order value. Direct sales and others revenue was RMB30,167 million, an increase of 21% YoY, primarily due to strong sales driven by the consumer electronics category. Revenue from China commerce wholesale business was RMB5,125 million, an increase of 1% YoY. Taobao and Tmall Group adjusted EBITA increased by 9% to RMB49,319 million. Adjusted EBITA margin fell 1.2 percentage points to 42.9%. Taobao app grew average daily active users (DAU) by 6.5% YoY, resulting from effective user acquisition programs and improving retention of Taobao app users during the quarter.

In Alibaba International Digital Commerce Group, Revenue from International commerce retail business was RMB17,138 million, an increase of 60% YoY. The increase was primarily due to strong combined order growth of retail businesses driven by solid performance of all major retail platforms, and improvements in monetization. Revenue from International commerce wholesale business was RMB4,985 million , which remained stable compared to RMB4,979 million in the same quarter of 2022. The adjusted EBITA was a loss of RMB420 million, compared to a loss of RMB1,380 million in the same quarter of 2022. Adjusted EBITA margin improved 6.9 percentage points to -1.9%. Losses significantly narrowed year-over-year primarily because of improved margins of Trendyol and Lazada, partly offset by the increase in investments in new business, such as Miravia, and AliExpress.

Revenue from Local Services Group was RMB14,450 million, an increase of 30% YoY, driven by strong revenue growth in both Ele.me and Amap businesses. During this quarter, order growth of Local Services Group exceeded 35% year-over-year. The adjusted EBITA was a loss of RMB1,982 million, compared to a loss of RMB2,834 million in the same quarter of 2022, reflecting the continued narrowing of losses driven by Ele.me's order growth and positive unit economics per order, as well as rapid order growth of Amap driven by market demand. Adjusted EBITA margin improved 11.7 percentage points to -13.7%.

Revenue from Cainiao Smart Network Logistics Limited was RMB23,164 million, increased by 34%, primarily contributed by the increase in revenue from international fulfillment solution services and domestic consumer logistics services. In June 2023, Cainiao commenced operation of three new international sorting centers, bringing the number of overseas sorting centers in operation to 18. The adjusted EBITA was a profit of RMB877 million, compared to a loss of RMB185 million in the same quarter of 2022. The adjusted EBITA margin improved 4.9 percentage points to 3.8%. Profitability turned positive year-over-year primarily because of improved operating results from international fulfillment solution services and domestic consumer logistics services.

Revenue from Cloud Intelligence Group was RMB25,123 million, increased by 4% YoY. The adjusted EBITA increased by 106% to RMB387 million. The adjusted EBITA margin improved 0.8 percentage points to 1.5%, primarily due to reduced colocation and bandwidth costs of DingTalk as a result of normalization of usage as compared to the same quarter last year.

Revenue from Digital Media and Entertainment Group was RMB5,381 million, an increase of 36%, primarily driven by growth in online entertainment business and strong recovery of offline entertainment business. During the quarter, Youku's total subscription revenue grew 5% year-over-year, primarily driven by increasing ARPU as well as benefiting from high-quality original content. In addition, revenue from Alibaba Pictures` movie and online platform business grew strongly year-over-year due to the launch of several blockbusters and robust China box office demands. Lost in the Stars, a movie for which Alibaba Pictures is a co-producer and the leading promoter and distributor, was the top performer in terms of box office in China during the quarter. The adjusted EBITA was a profit of RMB63 million, compared to a loss of RMB907 million in the same quarter of 2022. The adjusted EBITA margin improved 24.0 percentage points to 1.2%.

Revenue from all others segment was RMB45,541 million, which increased slightly by 1% YoY, primarily due to the revenue growth contributed by Alibaba Health, Fliggy, Freshippo and Intelligent Information Platform, partly offset by the decrease in revenue from Sun Art due to decrease in ticket size resulted from the decrease in consumer stockpiling behavior. Adjusted EBITA was a loss of RMB1,204 million, compared to a loss of RMB2,275 million in the same quarter of 2022. The adjusted EBITA margin improved 2.4 percentage points to -2.6%.

Income from operations was RMB42,490 million, an increase of 70% YoY; operating margin 18%, improved 6 percentage points. Excluding the reversal of share-based compensation expense, income from operations would have increased by 43% year-over-year to RMB35,589 million. Free cash flow was RMB39,089 million, an increase of 76% compared to the same quarter of 2022. Company repurchased repurchased 35.6 million ADSs (the equivalent of 284.4 million ordinary shares) for US$3.1 billion under the share repurchase program, and US$16.3 billion remained under the current share buyback program which is effective through March 2025.

�Company valuation

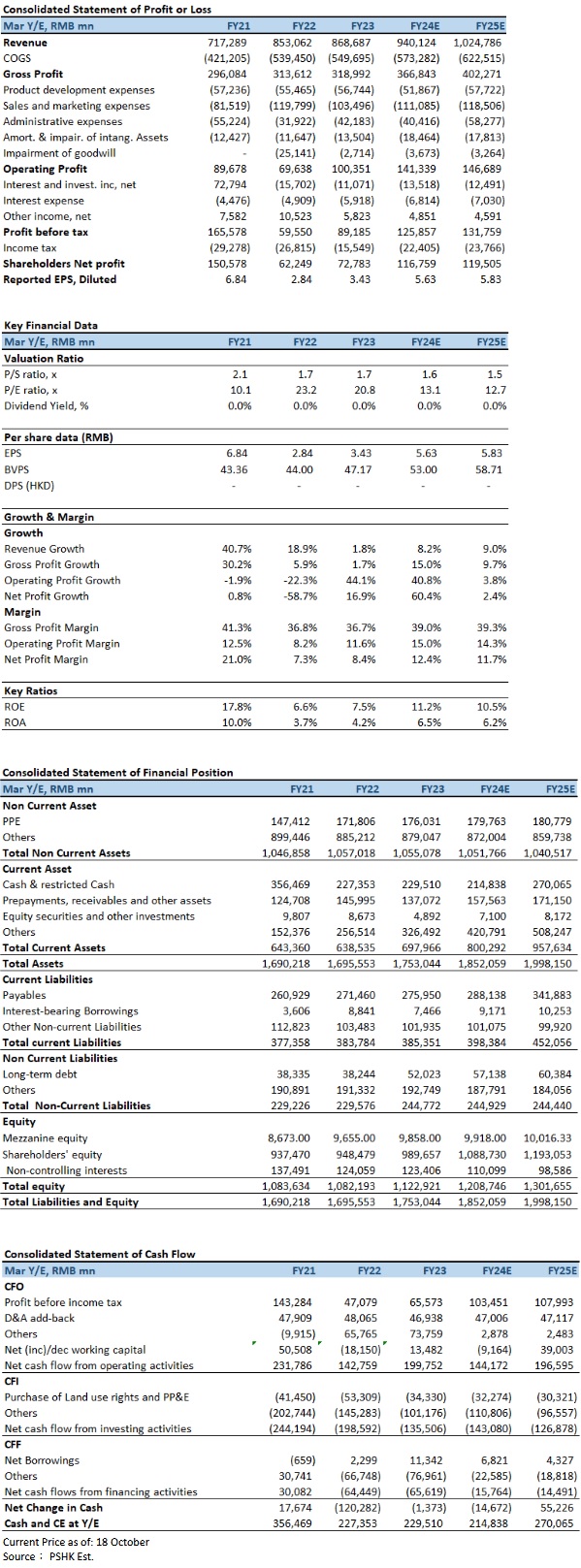

Since Alibaba announced major changes under the ŕ+6+N" group organization and governance structure, better than expected results achieved this quarter have also initially reflected the results of this change. On the other hand, the AI (artificial intelligence) revolution may also bring incremental opportunities; according to company management on the conference call, companies will use artificial intelligence to improve their services and invest in their own applications. On the other hand, as a cloud service provider, another monetization model for Alibaba is to let other AI companies and their models use Alibaba Cloud's infrastructure, especially Alibaba's cloud technologies, products and services at the three layers of IAAS, PAAS and MAAS, all have full-stack technologies and products that are relatively leading in the market. Although Cloud Intelligence Group's revenue growth in 1QFY2024 was only 4%, it is still expected to become the company's main long-term growth engine in the future. Alibaba completed the handover of group management responsibilities in September, but Daniel Zhang Yong left Alibaba Cloud just as the appointment took effect, which inevitably surprised the market. However, Alibaba's new CEO Eddie Yongming Wu acts as his deputy. He holds important positions in multiple consumer-related business groups and has deep insights into Alibaba's core commercial business. At the same time, he has a strong technical background, which may help Alibaba in technology. Discover new opportunities in the field, especially Alibaba Cloud's development in AIGC (generative artificial intelligence). In addition, although Alibaba's retail business Freshippo has suspended its listing plan in Hong Kong, Cainiao, which operates the express delivery business, has taken the lead in announcing a spin-off and listing in Hong Kong. In addition, the market also believes that management will once again focus on the growth momentum of Alibaba's various businesses. We believe it will better reflect the value of Alibaba. Of course, the valuation level may depend on the market's views on China's geopolitical risks, domestic consumption recovery risks and profitability risks, so it will be difficult to fully reflect the company's fundamentals in the long term. We expect FY2024E & FY2025E estimated EPS to be RMB$5.63 & RMB$5.83, respectively, and our target price is HK$118.95 (19.2x FY2024E P/E, in line with its 5 years average), with an "Buy" rating.

Risk factors

1) Weak domestic growth and slowdown in consumer spending (including online consumption); 2) Other large domestic Internet players pose a threat to the company's local services; and 3) GMV and overall revenue growth are lower than expected.

* The analyst has a financial interest in the listed corporation covered in this report.

Financial

Click Here for PDF format...