Overview

Yankuang Energy (1171.HK) takes mining, high-end chemical new materials, new energy, high-end equipment manufacturing, and smart logistics as its leading industries. It is the only extra-large company in China listed in four places at home and abroad including Shanghai, Hong Kong, New York, and Australia. The group's origin coal resources reach 13.7 billion tons (JORC standard), ranking among the top in the industry. The Group actively leads the transformation and upgrading of the industry, including maintaining high-quality and efficient development of the mining industry; accelerating chain extension and expansion for the high-end chemical new materials industry; actively promoting multiple projects to accelerate the rapid development of the new energy industry; strengthening and upgrading the equipment manufacturing industry, and integrating breakthrough intelligent Logistics industry. The Group's overseas mineral resources deployment highlights its competitive advantages. It is one of the most internationalized energy companies in China, which also greatly highlights the company's competitive advantages. At the same time, the group has strong strength and actively promotes scientific and technological research and development.

Company Performance review

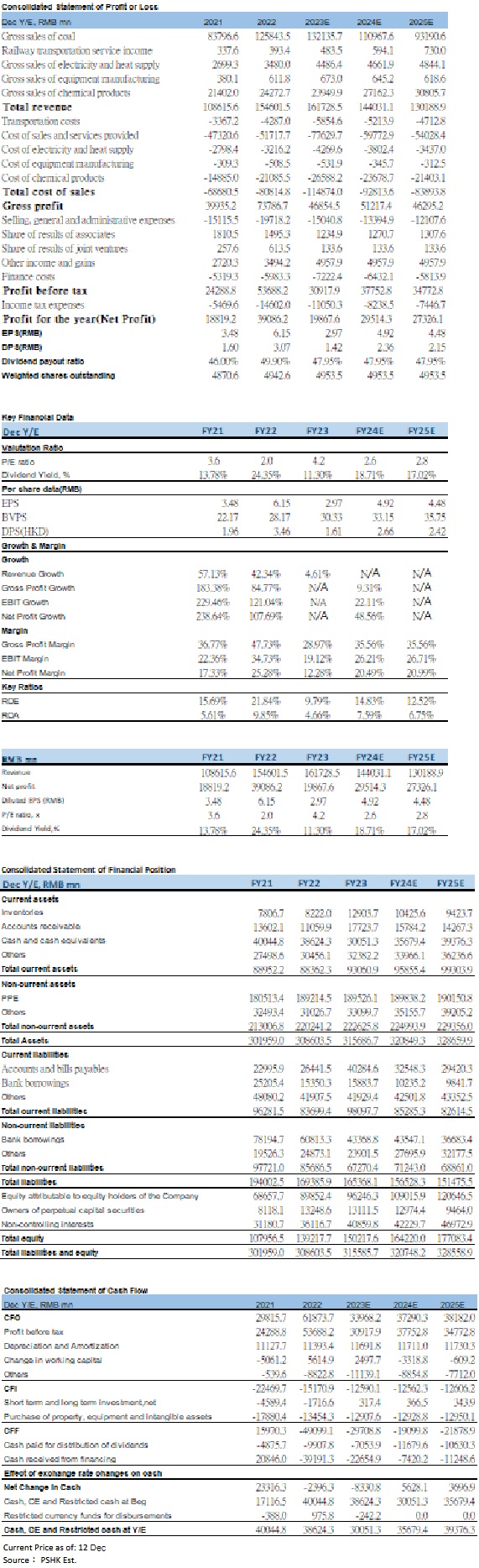

From the first to the third quarter of 2023, the group achieved operating revenue of 135.038 billion yuan (RMB, the same below), a decrease of 34.082 billion yuan YOY, a decrease of 20.15% YOY; the group achieved net profit attributable to shareholders of the listed group of 15.525 billion yuan, a decrease 13.657 billion yuan YOY, a decrease of 46.80% YOY. Basic earnings per share were 2.08 yuan, a decrease of 47.83% YOY, mainly due to a year-on-year decrease in the prices of major products such as coal and chemicals. The net cash flow generated by the group's operating activities was 19.007 billion yuan, a decrease of 50.05% YOY. The net amount of financial services such as deposits and loans provided by Yankuang Group Finance Co., Ltd. ("Yankuang Finance") to external parties increased by 11.036 billion yuan YOY. If excluding the influence of Yankuang Finance Division to the cash flow from operating activities, the group's net cash flow from operating activities was 18.028 billion yuan, still a decrease of 30.084 billion yuan YOY which was mainly due to the following two reasons: 1) Sales of goods and cash for rendering of services received decreased by 26.319 billion yuan YOY; 2) Cash used to purchase goods and receive services increased by 1.650 billion yuan YOY. The group released a profit distribution policy report on June 30, 2023. The group's profit distribution plan will increase the cash dividend ratio from 50% to 60%. In 2022, the group distributed annual dividends and special dividends totaling 4.3 yuan per share. This announcement reflected the group's commitment to improving shareholder returns.

Industry Analysis

Coal business

From the first to the third quarter of 2023, the Group achieved coal business sales revenue of 83.405 billion yuan, a decrease of 23.9% YOY; the Group produced 97.3 million tons of commercial coal, a decrease of 2.5% YOY; the Group sold 99.17 million tons of coal, a decrease of 2.0% YOY. The group's coal business sales cost was 44.105 billion yuan, an increase of 0.1% YOY. The Group's coal business is mainly distributed in China's Shandong Province, Shaanxi Province, Inner Mongolia Autonomous Region and Australia; its products

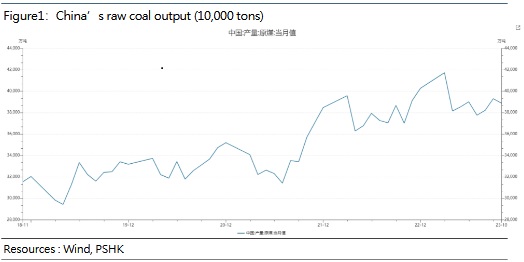

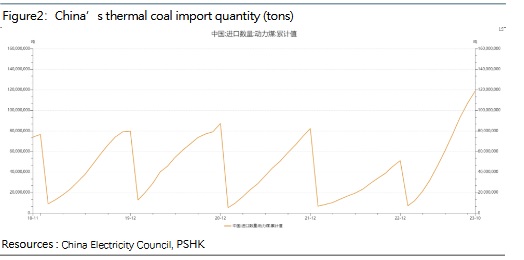

mainly include thermal coal, PCI coal and coking coal applicable to electric power, metallurgy and chemical l industry, etc., which are mostly sold to East China, South China, North China, Central China, Northwest China and other regions of China, as well as Japan, South Korea, Thailand, Australia and other countries. The Group is one of the major coal producers, sellers and traders in China and Australia. It is the largest coal producer in East China and a leading domestic thermal coal enterprise. Its subsidiary Yancoal Australia is the largest exclusive coal producer in Australia. In the first half of 2023, the coal industry continued to promote clean and efficient utilization of coal and safe and efficient mining, and the industry's supply security capabilities steadily improved. The release of high-quality coal production capacity is accelerating, imports continue to grow, the supply and demand situation has turned loosing, and price fluctuations are very obvious.The supply and demand of China's raw coal market will loose in 2023. China's raw coal production has been rising in fluctuations in the past five years (Figure 1). Data from the National Bureau of Statistics showed that from January to October 2023, enterprises above designated size produced 3.83 billion tons of raw coal, an increase of 3.1% YOY. In October, 390 million tons of raw coal were produced, an increase of 3.8% YOY. From January to October 2023, China imported 380 million tons of coal, an increase of 66.8% YOY. As of late November, Mongolia had exported a total of 60 million tons of coal, hitting a record high. The figure exceeded the 50 million tons of coal exports originally expected by the Mongolian government for the whole year, and also exceeded the 36.7 million tons of exports in 2019 before the epidemic. According to the latest data released by the General Administration of Customs of Mongolia, from January to October 2023, Mongolia exported 51.7221 million tons of coal to China, an increase of 139.87% YOY, accounting for 99% of Mongolia's total coal exports. The coal market is expected to improve in 2024, especially the thermal coal market supply and demand pattern may tighten. From January to September 2023, China imported a total of 261 million tons of thermal coal, an increase of 77.62% YOY (Figure 2), which showed that the thermal coal market is adequately supplied.

Thermal coal refers to coal used as raw material for power. Generally speaking, in a narrow sense, it refers to coal used for thermal power generation, but in a broad sense, any coal used to generate power for the purpose of power generation, locomotive propulsion, boiler combustion, etc. belongs to thermal coal. The terminal power demand directly affects thermal coal demand, the electricity consumption of the whole society has maintained growth, and the demand for thermal coal has also increased. Although the market has encouraged an increase in the use of clean energy in recent years, and the proportion of thermal power has shown a certain downward trend, overall, China's current power generation method is still dominated by thermal power. The cumulative installed capacity of thermal power this year has increased by 67.3% YOY. Therefore, the demand for coal related to power generation is still larger. In the short term, it is already in winter, the weather is turning colder, and the intensity of cold air continues to increase, which may drive the growth of coal power demand in winter.

In recent years, with the increasing expansion of domestic steel production capacity and the continuous progress and improvement of key technologies for blast furnace pulverized coal injection, market demand has gradually expanded. Especially with the increasing shortage of high-quality coking coal resources in China, PCI coal has played an important role in the steel smelting process and its position is increasing day by day. PCI coal can replace part of the coke. On the one hand, it can save coking investment, building fewer coke ovens, and reduce air pollution caused by coking; on the other hand, it can also greatly alleviate the tight supply and demand of coking coal. PCI coal has gradually become one of the indispensable furnace materials for steel enterprises. Coking coal is the material used to make coke, which is mainly used for steelmaking. Recently, there is news that supervision is considering allowing banks to provide unsecured working capital loans to real estate companies for the first time. In addition, Shenzhen will reduce the minimum down payment ratio for second homes to 40% starting from November 23, 2023. The real estate industry continues to introduce favorable policies, which will help promote the growth of steel demand. Preliminary data released by the World Steel Association show that in October 2023, the world's crude steel output in 71 countries included in World Steel Association statistics was 150 million tons, an increase of 0.6% YOY. Among them, China's crude steel output was 79.1 million tons, a decrease of 1.8% YOY; India's crude steel output was 12.1 million tons, an increase of 15.1% YOY; Japan's crude steel output was 7.5 million tons, an increase of 2.6% YOY; the United States` crude steel output was 6.8 million tons, an increase of 3.4% YOY. From January to October 2023, global crude steel production totaled 1.567 billion tons, an increase of 0.2% YOY. Among them, the crude steel output of China, India, Japan, the United States and Russia were 875 million tons, 116 million tons, 72.9 million tons, 67.4 million tons and 63.5 million tons respectively, with year-on-year changes of 1.4%, 12.1%, -3.0% and -0.8 % and 5.3%. Overall, it is expected that global steel production will continue to increase in the future, so the demand for PCI coal and coking coal will still grow.

It is believed that as the supply and demand pattern of the coal market becomes tight in 2024 and coal prices rise steadily, the Group's coal business revenue is expected to improve significantly.

Coal chemical business

From the first to the third quarter of 2023, the group achieved sales revenue of 19.703 billion yuan from its coal chemical business, an increase of 0.3% YOY. The group produced a total of 6.495 million tons of related coal chemical products, an increase of 14.0% YOY; the group sold a total of 5.895 million tons of products, an increase of 10.5% YOY; the group's coal chemical business sales cost was 15.863 billion yuan, an increase of 1% YOY. The Group's coal chemical business is mainly distributed in China's Shandong Province, Shaanxi Province and Inner Mongolia Autonomous Region; its products mainly include methanol, acetic acid, ethylene glycol, etc.; its products are mainly sold to North China, East China, Northwest China and other regions. The group has multiple complete coal chemical industry chains including coal gasification and coal liquefaction, and the largest single coal liquefaction unit in the country. It is the only domestic enterprise that masters both low-temperature FT synthesis and high-temperature FT synthesis technologies. The Group's coal chemical industry is accelerating its development towards high-end, diversified and low-carbon directions. The industrial chain continues to extend and expand, and the industrial structure continues to transform and upgrade. Affected by the macro economy, downstream demand in the coal chemical industry remains weak, and prices are under downward pressure. However, the group insists on flexible production, adjusts the product structure, and releases production capacity to marketable and high value-added products. It strives to increase the annual chemical product output by more than 10% year-on-year, and the proportion of high-end chemical products reach 20%.

Electric power business

From the first to the third quarter of 2023, the group achieved sales revenue of 1.993 billion yuan in power business, a decrease of 2.5% YOY. The group's total power generation reached 6.64 billion kilowatt-hours, an increase of 5.6% YOY; the group's electricity sales totaled 5.49 billion kilowatt-hours, an increase of 3.59% YOY; the group's power business sales cost was 1.803 billion yuan, an increase of 4.2% YOY.

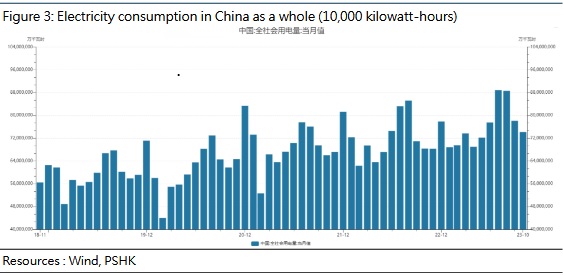

From January to October 2023, the total electricity consumption in the whole society was 7,605.9 billion KWh, an increase of 5.8% YOY. In terms of industries, the primary industry consumed 107.6 billion kWh of electricity, an increase of 11.4% YOY; the secondary industry consumed 4,991.2 billion kWh of electricity, an increase of 5.8% YOY; the tertiary industry consumed 1,380 billion kWh of electricity, an increase of 10.4% YOY; the domestic electricity consumption of urban and rural residents was 1,127.1 billion kWh, an increase of 0.4% YOY. As can be seen from Figure 3, the electricity consumption of the whole society has increased steadily year by year in the past five years, so the group's electricity sales are expected to continue to increase.

Valuation and recommendation

The coal industry may start a new upward cycle in 2024. Safety accidents have occurred frequently in domestic coal production areas recently. Production safety supervision has been continuously strengthened in production areas, and the growth rate of the supply side is subject to certain restrictions. At the same time, the demand for non-electrical coal is stable. With the coming of cold winter, the demand of winter electricity consumption will rise and demand for thermal coal will increase, the coal market is expected to return to tight pattern of supply and demand again, which will support coal prices.

We predict that the group's revenue will be 161.729 billion yuan, 144.031 billion yuan and 130.189 billion yuan respectively in 2023-2025, with EPS of 2.97/4.92/4.48 yuan, corresponding to P/E of 4.2/2.6/2.8x. The group's average P/E in the past three years is about 4.69, giving that 5 times P/E in 2023, and giving it HK$16.30, giving it an "accumulate" rating. (Current price as of December 12)

Risk factors

Energy policy impact, geopolitics, power demand, safety accidents

* The analyst has a financial interest in the listed corporation covered in this report.�

Financial

Click Here for PDF format...