Perfect Medical Health Management (“Perfect Medical”) is a comprehensive medical beauty and medical healthcare service provider, through integrating and developing its “Medical + Beauty” operational model, offering customers safe and effective medical services. Perfect Medical has a presence throughout Hong Kong, China, Australia, Singapore and Macau. The company principally engages in the provision of providing one-stop “Medical + Beauty” services and provides a full range of services, including “Medical (Pain Management)”, “hair growth treatment”, “Gynaecological medical service”, “men's beauty and weight management”, “Medical Beauty services” and etc.

Overall business restore the growing momentum, overtaking the pre-pandemic interim revenue in Hong Kong

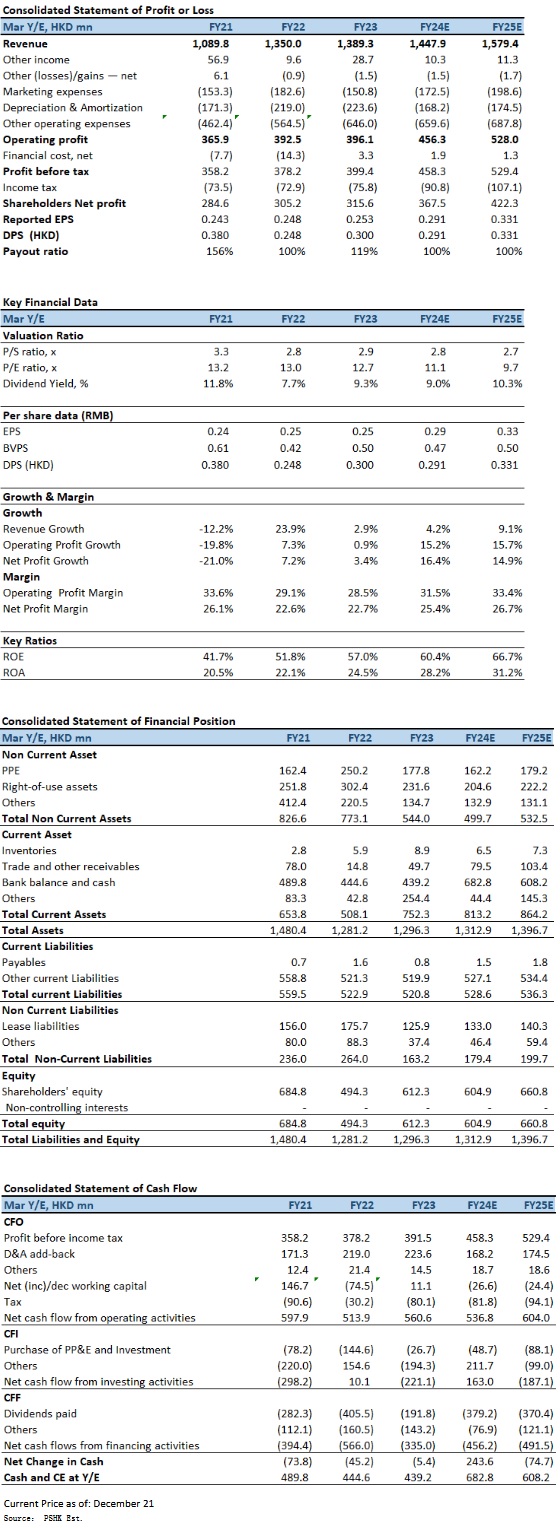

In 1HFY2024 (for the six months ended 30 September 2023), Perfect Medical's revenue increased by 7.5% to HK$718mn. Profit attributable to equity holders was HK$ 166.4mn, increased by 10.4% YoY. If excluding the Hong Kong government subsidies, the revised net profit after tax increased by 27.1%. Basic earnings per share increased by 9.1% to HK13.2 cents. The interim dividend and special dividend are HK13.2 cents and 1.0 cent per share, with total dividend of HK14.2 cents per share and dividend payout ratio of 107.6%.

For the period under review, the company has proactively reshaped its operations in Hong Kong, taking advantage of the changing consumer behavior and the relatively affordable rental situation. By further increased its market penetration in Hong Kong through a combination of mega shops and the newly established residential shops business model to tap the demand in the local neighborhood and to further increase its market share. Business performance was particularly appealing for the residential shops in which company was able to obtain a high proportion of new customers into its ecosystem. Aesthetic medical business continued to be the company's core business for the period, contributing to around 80.7% as measured by the value of sale contract. The overall average spending per individual client increased by 16.1% YoY to HK$27,540. Regarding cost control, the employee benefit expenses increased by 3.3% YoY to HK$238mn, in line with the revenue growth. The marketing expenses increased by 10.0% YoY to HK$85.5mn, as a result of the resumption of marketing campaign to boost the brand awareness. The rental lease related expenses decreased by 4.4% YoY to HK$83.2mn, due to the consolidation of service area in regions outside Hong Kong YoY. The operating profit margin remained at 28.1%, and the net profit margin increased of 0.7 percentage points to 23.2%.

By regions, revenue from Hong Kong operation increased by 11.6% YoY to HK$549.6mn, overtaking the revenue of Hong Kong operation before pandemic in FY2019/20 interim by 7.2%, thanks to the improvement in shop utilization and the contribution from the newly established residential shops in Hong Kong. As of 30 September 2023, the company has a well-established network of service centres in Hong Kong covering a total of 192,000 square feet, with an increase of two shops in Tsuen Wan and Taikoo. Currently, revenue from Hong Kong operation accounted for 76.5% of the company's revenue (1HFY2023: 73.7%).

Revenue from regions outside Hong Kong decreased by 4.2% YoY to HK$168.5mn, significantly dampened the consumer confidence in mainland China and the sustained inflationary environment and the high living expenses in Australia and Singapore, may take some time for the market to recover. Revenue from the regions outside Hong Kong accounted for 23.5% of the company's revenue (1HFY2023: 26.3%). As of 30 September 2023, the company has an extensive network in mainland China, Macau, Sydney, Melbourne and Singapore, covering a gross service area of 105,000 square feet, no change when compared to 31 March 2023.

Investment Thesis

Over the past three years, there have seen a series of closures of the smaller beauty clinics who were hard-hit by the prolonged pandemic outbreak. Against this backdrop, the pandemic has also presented a golden opportunity for well-established industry players to further increase the market penetration into the neighborhoods and their surrounding areas where there was pent-up demand. Through the introduction of residential shops in medium-to-high end shopping malls and residential locations, the company has recalibrated its business model to further expand its geographical reach in Hong Kong. In addition to continuing to accelerate expansion through a combination of mega shops and the newly established residential shops, the rebound in tourist arrivals in Hong Kong this year will bring along additional cross-border customers to the company. Furthermore, Perfect Medical stated that it will form a new company with Goku SPA, a 15-year-old Japanese company famous for its Japanese-style "deep sleep" head massage, and will provide services in its current 53 service centers. The store-in-store expansion is expected to contribute approximately HK$600mn annual revenue contribution. The company also plans to open 60 standalone shops in next three years in Greater Bay Area and 1st tier cities of mainland China, which is expected to contribute more than HK$1.2 billion annual revenue contribution after 3 years. In fact, at its non-aesthetic medical business, the company includes a range of supplementary healthcare management services, including hair growth treatment, pain treatment, health screening service as well as other beauty and wellness services, which are expected to help increase customer stickiness and increase cross-sales. We expect FY2024E-FY2025E EPS to be HK$0.291 (similar to our research report forecast in February) and HK$0.331 respectively, with PT of HK$4.37, implies a FY2025E P/E of 13.2x (similar to past two years average P/E ratio + 1 standard deviation), and the rating is upgraded to “Buy”.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand; 4) Tighten regulatory policies related to medical aesthetics.

Financial

Click Here for PDF format...