FSE Lifestyle Services (��FSE��) are a lifestyle services conglomerate with 3 major business segments: property & facility management services, city essential services and E&M services. FSE's services are being delivered through 8 major groups of companies which include Urban Group, Kiu Lok Group, Waihong Services Group, FSE Environmental Technologies Group, Hong Kong Island Landscape Company Limited, General Security Group, Nova Insurance Group and FSE Engineering Group. FSE offer comprehensive ��one-stop shop�� professional services to its clients who are engaged in a wide diversity of projects, including property developments, public infrastructures, education and transportation facilities, as well as entertainment and travel industries in Hong Kong, Macau and the Mainland China. FSE clientele includes the HKSAR Government, multinational corporations, owners and investors of properties, theme parks, universities, hotels and hospitals covering both private and public facilities.

Core np recorded a considerable growth, with total outstanding contract sum of 10.7B

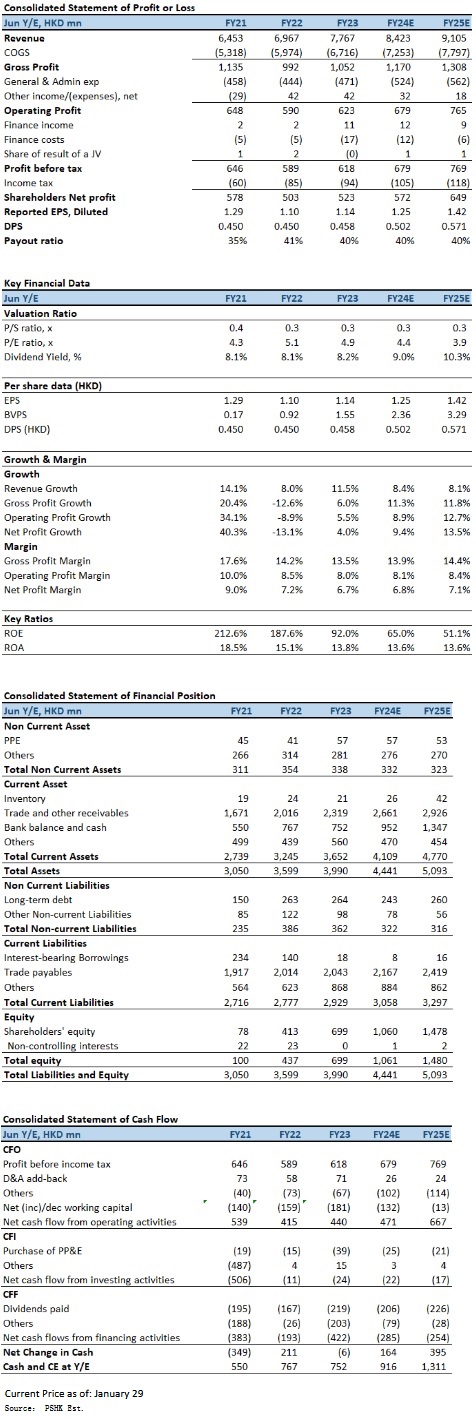

In FY2023 (for the year ended 30 June 2023), FSE's recorded revenue amounting to HK$7,767.2mn, representing an increase of 11.5% YoY. Profit attributable to shareholders was HK$522.9mn, representing an increase of 4.0% YoY, mainly resulted from the strong performance of the cleaning & pest control, technical support & maintenance, insurance solutions, environmental solutions and E&M businesses, partly offset by the effects of a lower contribution from the security guarding & event services business, a decrease in government grants and higher corporate finance costs. If excluding the effects of government grants, FSE recorded an increase in adjusted net profit of 7.5% to HK$445.9mn (i.e. after excluding government grants of HK$77.0mn from profit attributable to shareholders of HK$522.9mn) as compared to its adjusted net profit of HK$414.7mn for FY2022. Basic EPS was HK$1.14, an increase of 3.6% YoY. The final dividends for FY2023 was HK$21.3 cents (FY2022: HK$24.1 cents) per share, total dividends will be HK45.8 cents (FY2022: HK$45.0 cents) per share, the dividend payout ratio (calculated based on the adjusted profit) is 40.1% (FY2022: 41.0%, calculated based on the adjusted profit).

The gross profit increased by HK$59.1mn or 6.0% to HK$1,051.6mn from HK$992.5mn in FY2022, with an overall gross profit margin decreased to 13.5% from 14.2%. If excluding the effects of government grants, adjusted gross profit margin would decrease to 13.1% from 13.6% FY2022, mainly caused by a lower gross margin of the city essential services segment, principally driven by the higher labour costs in the security guarding & event services business.

By business segment, city essential services segment revenue grew by 15.8% YOY to HK$3,766.8mn, contributed 48.5% (FY2022: 46.7%) of the total revenue. The growth is mainly reflected many new general cleaning service contracts, encompassing a wide range of buildings and facilities, including government leisure facilities, shopping malls, clubhouses, exhibition centres, airport ancillary building, government clinics and buildings, residential and commercial properties; higher revenue from its technical support and maintenance services business for system replacement and upgrading works including various shopping malls in Tseung Kwan O and Lei Yu Mun, a residential property in Central and term contract works for a number of government departments and facilities; higher revenue from its environmental solutions business, especially its provision of ELV device installation services for 11 SKIES project in Chak Lap Kok and an increase in new insurance contracts for general insurance and insurance for construction projects awarded. Segment profit increased by 7.1% YoY to HK$215.9mn, with its gross profit margin decreased to 12.4% from 13.4%. This was caused by the higher labour costs.

Property & facility management services segment revenue grew by 1.8% YoY to HK$708.6mn, contributed 9.1% (FY2022: 10.0%) of the total revenue. Such growth was mainly driven by newly awarded property management contracts for residential and industrial buildings in Hong Kong and property management income from a property management project in Shanghai. Segment profit increased by 1.6% YoY to HK$138.5mn, with its gross profit margin increased to 32.6% from 31.5%. This was caused by higher property management remuneration income from a commercial complex in Wanchai.

E&M services segment revenue increased by 9.1% to HK$3,291.8 million, contributed 42.4% (2022: 43.3%) of the total revenue. Such growth reflected the substantial progress of a number of E&M engineering installation projects this year including Immigration Headquarters in Tseung Kwan O, redevelopment of an office building in Wan Chai, a public rental housing project in Tai Po and Ningbo New World Plaza Comprehensive Development project, partly offset by a lower revenue contribution from the InIand Revenue Tower project in Kai Tak and Macau Studio City Phase 2 which had significant progress last year. Segment profit increased by 7.0% YoY to HK$186.6mn, with its stable gross profit margin at 10.8%, principally reflected a higher gross profit contribution from its Immigration Headquarters project in Tseung Kwan O, partly offset by a decrease in government grants.

As of 30 June 2023, the property & facility management services segment has a total gross value of contract sum of HK$1,905mn with total outstanding contract sum of HK$963mn; the city essential services segment has a total gross value of contract sum of HK$9,857mn with a total outstanding contract sum of HK$6,196mn; the E&M services segment has a total gross value of contract sum of HK$11,378mn with a total outstanding contract sum of HK$5,857mn. The total gross value of contract sum of the above-mentioned is HK$23,140mn, and the total outstanding contracts sum of HK$13,016mn. With the sufficient reserve of outstanding contracts project, future revenue growth would be guaranteed.

Investment Thesis

FSE's compound annual growth rate (CAGR) of revenue and profit from FY2017 to FY2023 reached 13% and 20%, respectively. In fact, according to the government's policy on increasing the supplies of residential units by the coming 10 years, the increasing supply of both private and public housing units, hence, creates a growing demand and necessities of professional property management services in the territory; in addition, Kai Tak and the Northern Metropolis, and the demand for professional cleaning and hygiene services is expected to increase. At the same time, the municipal solid waste charging scheme will be enacted in the second quarter of 2024, and the company's waste management team has also expanded fleet scale and business mode to deal with the anticipated market demand. Finally, looking forward to the large number of business opportunities on sizeable infrastructure and building projects expected to arise in Hong Kong, Mainland China and Macau in the coming years, it is also expected to bring many business opportunities to FSE's E&M services business. The net cash balance increased by HK$106.4 million to HK$469.9 million, and the financial and liquidity position was stable. We expect FY2024E-FY2025E EPS to be HK$1.25 and HK$1.42 respectively, with PT of HK$6.45, implies a FY2024E P/E of 5.15x (~2-yrs historical average). Our investment rating is ��Accumulate��.

Risk factors

1) Market competition intensifies; 2) Soaring in operating cost; and 3) Unexpected slowdown in service demand.

Financial

Click Here for PDF format...