Founded in 1994 and listed on the Hong Kong Stock Exchange in 2016 (stock code: 03306), JNBY is designer group in China and is headquartered in Hangzhou, China. JNBY design and sell fashion apparel, footwear, accessories and home products under a portfolio of brands in three stages, including mature brand representing JNBY, younger brands representing CROQUIS, jnby by JNBY and LESS, and emerging brands representing POMME DE TERRE, JNBYHOME. As of December 31, 2023, the total number of standalone retail stores around the world is 2,036 (including "JNBY Group +" multi-brand collection stores), sales network has covered all provinces, autonomous regions and municipalities in Mainland China and across nine other countries and regions around the world.

GM increased attributable to the enhancement of the brand power

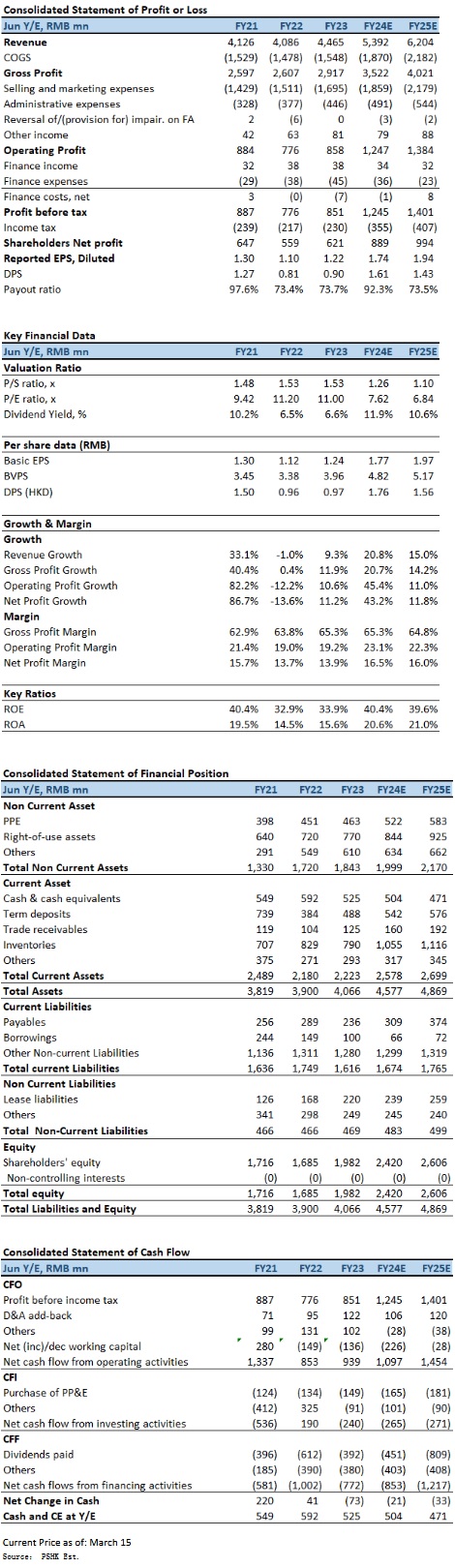

For the year ended June 30, 2023 (FY2023), the total revenue amounted to RMB4,465 million, an increase of 9.3% YoY. The net profit amounted to RMB621 million, an increase of 11.2% YoY. Net profit margin increased by 0.2 percentage points YoY to 13.9%. The basic EPS were RMB1.24, an increase of 10.7% YoY, with a final dividend of HK$0.67 per share (equivalent to RMB0.63 per share), together with the interim dividend of HK$0.30 per share, the total dividend of HK$0.97 per share for the year. The company's gross profit increased by 11.9% to RMB2,917 million; The overall gross profit margin increased from 63.8% for FY2022 to 65.3% for FY2023. In percentage terms, the selling and marketing expenses accounted for 38.0% (FY2022: 37.0%), the increase in the expense ratio as compared to the previous year was mainly attributable to the increase in the investment in long-term brand power building.

The total revenue for the six months ended December 31, 2023 (1HFY2024) amounted to RMB2,976 million, an increase of 26.1% YoY. The increase in revenue was mainly due to the increase in same store sales of offline shops, the growth in the sales of online channels and the increase in the scale of offline stores. Net profit was RMB574 million, representing an increase of 54.5% YoY; Net profit margin increased by 3.5 percentage points to 19.3%. The basic EPS were RMB1.14, an increase of 54.1% YoY, with an interim dividend of HK$0.46 per share (equivalent to RMB0.42 per share) and a special interim dividend of HK$0.39 per share (equivalent to RMB0.36 per share), totaling HK$0.85 per share.

1HFY2024, the gross profit increased by 27.6% YoY to RMB1,948 million; The overall gross profit margin increased by 0.8 percentage points to 65.5% , which was mainly attributable to the enhancement of the comprehensive brand equity. The selling and marketing expenses accounted for 31.1% (1HFY2023: 34.6%). The decrease in the expense ratio as compared to the first half of fiscal year 2023 was mainly attributable to the increase in the overall revenue and the improvement of operating efficiency.

Offline customer traffic recovered

By brand portfolio, the revenue generated from mature brand with a history of approximately 30 years (JNBY) increased by 24.0% YoY to RMB1700 million, accounting for 57.1% of total revenue. The number of standalone retail stores worldwide was 935, an increase of 14 YoY. The gross profit of related products was RMB1,138 million, an increase of 25.2% YoY; the gross profit margin was 67.0%, an increase of 0.7 percentage points YoY.

For the Younger brands portfolio, it consists of brands which were successively launched from 2005 to 2011, namely CROQUIS, jnby by JNBY and LESS. Revenue generated from the Younger brands portfolio increased by 29.7% to RMB1,228 million, accounting for 41.3% of total revenue. The number of standalone retail stores worldwide is 1,043, an increase of 24 YoY. The gross profit was RMB788 million, an increase of 32.2% YoY; the gross profit margin was 64.1%, an increase of 1.1 percentage points YoY.

For the Emerging brands portfolio, it consists of various new brands, such as POMME DE TERRE and JNBYHOME. Revenue from the Emerging brands portfolio totaling RMB48.0 million was recorded, increased by 12.9% YoY. The number of standalone retail stores worldwide is 38, an increase of 7 YoY. The gross profit was RMB21.688 million, an increase of 4.3% YoY; the gross profit margin was 45.2%, a decrease of 3.7 percentage points YoY.

As China's economy fully resumed normal operation, the offline customer traffic recovered. By sales channels, the same store sales of offline retail shops for 1HFY2024 recorded an increase of 23.9%; of which revenue generated through offline channels increased by 26.5% to RMB2,442 million, accounting for 82.1% of the total revenue; and the revenue generated through online channels increased by 24.2% to RMB534 million, accounting for 17.9% of the total revenue.

As of December 31, 2023, the company had over 7.4 million membership accounts (without duplication) (as of June 30, 2023: over 6.9 million). The retail sales contributed by the members of the company accounted for over 80% of the total retail sales. The number of active members accounts of the company (without duplication) was over 550,000 (2022: over 420,000), and the number of active members accounts was significantly higher than that in 2022. The number of membership accounts with annual purchases totaling over RMB5,000 was over 300,000 (FY2022: over 220,000), and the retail sales contributed by those membership accounts reached RMB4.33 billion (FY2022: RMB2.93 billion), accounting for over 60% of the total retail sales from offline channels.

Company valuation

The group of people who pursue distinguished lifestyles continues expanding. As the demand of customers for personalized and fashionable products continues to rise and the younger consumers` preference for products and brands with strong brand awareness is increasing, the segmented market where the designer brands operate has great potential, and the designer brands operate has shown a competitive trend of inclining to the leading brands. Despite the backdrop of various uncertainties such as continuous changes in the retail environment and consumer behavioral habits, by continuously launching new consumption scenarios or products such as "Box Project" and "JNBY Group+" multi-brand collection stores, which successfully provide customers with more comfortable shopping experience. However, the China CPI has experienced four consecutive months of contraction (with a 0.7% increase in February due to the Lunar New Year), indicating that the deflationary cloud in the mainland has yet to dissipate. It remains to be seen whether the declining consumer desire of citizens has stabilized. If unfortunately, the situation turns negative again, a vicious cycle cannot be ruled out. In view of the above impact, we expect FY2024E & FY2025E estimated basic EPS to be RMB$1.77 & RMB$1.97 respectively, with TP is HKD15.27, implies a FY2024E P/E of 7.9x and FY2024E dividend yield of ~11.6%. Our investment rating is “Neutral”.

Risk factors

1) Deterioration of the mainland macroeconomic conditions; 2) Intensified industry competition; and 3) Slower-than-expected brand sales.

Financial

Click Here for PDF format...