Investment Summary

Company Profile

Xinyi Solar Holdings Limited (hereinafter referred to as "Xinyi Solar" or the "Company"), established in 2006, is the world's largest photovoltaic (PV) glass manufacturer and one of the two oligopolies in the industry. Major products include ultra-clear patterned solar glass (raw and tempered), anti-reflective coating glass, and back glass.

The parent company, Xinyi Glass Holdings Limited (Xinyi Glass) (868.HK), is a global leader in automotive glass, float glass, and architectural glass. It entered the field of PV glass in 2006, by raising HKD191 million through a placement, and then constructed multiple production bases successively in Anhui, Tianjin, Malaysia, and Beihai. Xinyi Solar was spun off from the parent company and got listed in the way of introduction in 2013. Then, it raised HKD11.78 billion for capacity expansion through seven placements or rights issues.

The Company began the operations of solar farms in 2014, set foot in the Engineering, Procurement, and Construction (EPC) of solar farms in 2015, and span off its subsidiary operating solar farms-- Xinyi Energy Holdings Limited (Xinyi Energy) (3868.HK)--for listing in 2019. As of December 31, 2023, the Company held 51.6% of shares in Xinyi Energy. The Company (with a shareholding ratio of 52%) and Xinyi Glass (48%) jointly established Xinyi Crystalline Silicon in 2021 to march into the crystalline silicon production industry. Meanwhile, the Company was included in the Hang Seng Indices in the same year. Lee Yin Yee, the de facto controller of Xinyi Solar, and the other eight shareholders act in concert, who directly and indirectly hold 49.24% of shares in the Company in total.

The Company's revenue mainly comes from two core business, namely the sales of PV glass and the operations of solar farms. They contributed to 88.5% and 11.2% of the total revenue, respectively, (according to the 2023 annual report) and 71% and 29% of the gross profit, respectively. Polysilicon business (under development and construction) and EPC business are not core business. At present, Xinyi Solar has four major PV glass production bases, which are located in Wuhu City of Anhui Province, Beihai City of Guangxi Province, Zhangjiagang City of Jiangsu Province, Tianjin City in China, and Malaysia, as well as 13 solar farms.

Competitive Advantages: Continue to Consolidate the Advantages in Scale and Leadership

Xinyi Solar has deeply engaged in PV glass for more than a decade, and gained a leading position in several aspects (e.g. scale, technology, yield, revenue, and profitability) of PV glass, due to the forward-looking layout for technology R&D, the capital advantage brought by the early listing, and the capacity expansion plan going through cycles. Moreover, the glass business of the parent company has a synergistic effect on the Company, especially the advantage of scale in the centralized procurement of raw materials, energy costs, and transportation. The two major costs of PV glass lie in raw materials and fuel energy, each representing 30-40% of the production cost. Most of the plants of the two companies are adjacent, so they can strategically purchase bulk raw materials, such as quartz sand and sodium carbonate, together. The Company adopts piped natural gas and has signed long-term agreements to reduce costs. Additionally, the Company took the lead in the industry in using large-scale furnaces (with a daily capacity of 1,000 tons). Compared with smaller furnaces, larger ones can significantly reduce electricity and natural gas consumption per unit and also feature high automation and high yield.

Financial Analyst

From the listing in 2013 to 2023, Xinyi Photovoltaic quickly raised its revenue and net profit, thanks to the rapid growth of the PV industry. Meanwhile, its ten-year compound annual growth rates of the total revenue and the net profit were 29.8% and 30%, respectively. As of the end of 2023, its daily melting capacity of PV glass amounted to 25,800 tons, nearly 13 times the 2,000 tons at the end of 2013. At the end of 2023, the Company's cumulative grid-connected installed capacity reached 5,944MW, wherein 3,695MW was indirectly held through Xinyi Energy.

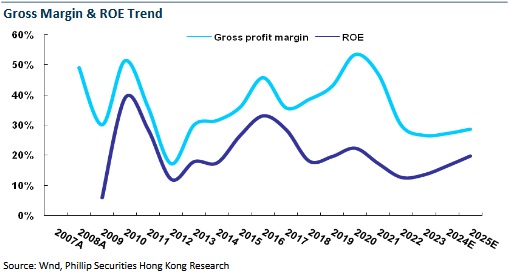

Over the past eight years, the gross profit margin maintained between 26% and 54%. Specifically, the fluctuations in the gross profit margin of solar farm operations business were relatively small and between 68% and 77%. Because of the greater impacts of the industry cycle, the fluctuations of PV glass business were between 21% and 50%. Especially, driven by short supply in 2020, the gross profit margin of PV glass used to reach 49%, and the diluted ROE was between 18% and 42%. However, the figures have fallen in recent years. Besides the impact of the industry cycle, the Company reduced financial leverage, and the asset-liability ratio declined from 55.8% in 2016 to 37.4% in 2023.

FY2023H1 Was Lower and Higher in H2; the Production of PV Glass Continued to Expand

The FY2023 result report revealed that, the Company's annual revenue stood at HKD26.63 billion, up by 29.6%yoy, and the annual net profit attributable to the parent company was HKD4.19 billion, rising by 9.6%yoy, exceeding the previous market expectations. In the second half of the year, the revenue reached HKD12.94 billion with yoy and hoh increases ratio of 29% and 16%. The net profit attributable to the parent company amounted to HKD2.51 billion. Different from the year-on-year decrease of 27% in the first half of the year, the figures in the second half sharply grew by 41% and 96%yoy and hoh.

The main reason for the lower and then higher results is that the PV glass business in the first half of the year was affected by the increased raw material and energy costs and the decreased average selling price (ASP). Yet, the sharp fall in the prices of polysilicon and PV components from the second quarter triggered the accelerated downstream demand for installed capacity in the second half of the year. Coupled with a slowdown in the growth of PV glass capacity, the supply and demand in the PV glass market was improved. Due to the declined ASP, higher raw material prices, and unfavorable exchange rate direction, the overall gross margin dropped by 3.4 percentage points to 26.6% from 30% in 2022.

Geographically, the revenue from the Chinese Mainland stood at HKD18,115 million, growing by 34.5%yoy and accounting for 77% of the total revenue. The revenue from the rest of Asia amounted to HKD4,496 million, which went up by 39%yoy and represented 19% of the total revenue. The revenue from North America and Europe was HKD904 million, which was the same as that of the previous year and accounted for 3.8% of the total revenue. Lastly, the revenue from the rest of the world amounted to HKD18 million, down by 66%yoy.

By segment, PV glass sales rose by 49.3%yoy. The Company's domestic market share of PV glass was 24.0% with an increase of 0.4 percentage points. As of the end of 2023, the capacity reached 25,800 tons. Furthermore, six new production lines of 1,000 tons each were added, two of which were put into operation in the first half of the year, and the rest four in the second half. Nevertheless, given the decreased ASP and foreign exchange losses, the revenue from PV glass climbed by 33%yoy to HKD23.5 billion, which was lower than the growth rate of the sales volume. Fortunately, benefiting from the volume growth following the rapid release of capacity and the improved supply and demand, the gross profit of the segment rose from 15.24% in the first half of the year to 26.41% in the second half. With respect to future planning, the Company will continue to maintain an aggressive pace of capacity expansion. A total of six production lines with a capacity of 6,400 tons are planned to be launched in 2024, including four in Anhui Province and two in Malaysia. Moreover, the Company intends to build new production lines in Yunnan and Jiangxi Provinces as well as Indonesia after 2025.

In regard to solar farms, the Company added 1,094MW of new grid-connected solar farms throughout the year, a record high. The cumulative grid-connected installed capacity stood at 5,944MW (including 5,541MW from centralized power plants and 78MW from distributed power plants). The revenue from this segment in the period was HKD3 billion, increasing by 8%yoy. The gross profit margin was 68.5% with a year-on-year decrease of 1.9 percentage points, mainly due to the loss of limited power supply arising from grid consumption and the higher operating costs because of the regulations for energy storage safety. Considering policy and market uncertainties, Xinyi Solar has decided to set up more prudent objectives for installed capacity, and planned to add 300MW of grid-connected capacity in 2024.

As a result, the Company's overall capital expenditure for 2024 is planned to be HKD7 billion, significantly declining from HKD9.9 billion in 2023, and a higher weight is given to PV glass business.

Investment Thesis

After two consecutive years of unprecedented growth, it is expected that the global PV installed capacity will continue to grow in 2024, but the growth rate will be slower or not as high as that in the past two years but still higher than the long-term historical average. However, PV glass is expected to grow faster than the PV installed capacity. For capacity expansion, Xinyi Solar adopts a positive attitude. It is expected that the cost advantage will be reinforced, and the leading position will be consolidated. Moreover, the Company's overseas capacity is expected to double this year, and its overseas products enjoy a high premium. If expanded smoothly, overseas products will become another growth point for the Company.

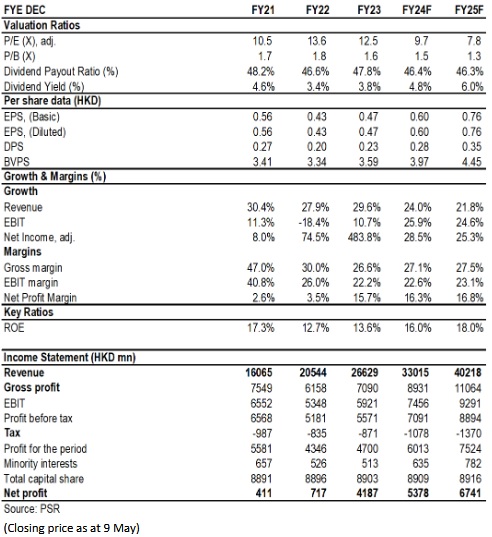

We are optimistic about the Company's future in consideration of the alleviated pressure in PV glass inventory, the stabilized selling price, and the weak prices of sodium carbonate and natural gas in the medium term. We estimate that the Company's earnings per share (EPS) in 2024 and 2025 will be HKD0.60 and HKD0.76. Taking into account the Company's leading advantage and new capacity to build, P/E ratios in 2024 and 2025 are expected to be 12x and 9.6x, with Target Price of 7.26 HKD, BUY rating. (Closing price as at 9 May)

Risk

Declining demand in the photovoltaic industry and price wars

Rising raw material costs

Overseas market risk

Domestic policy risks

Financials

Click Here for PDF format...