Overview

COSCO Shipping Holdings (01919.HK) is the listed flagship enterprise and capital platform of COSCO Shipping Group's main business of shipping and terminal operations. The company has global routes, with more than 263 international routes, being attached at 594 ports in 144 countries and regions around the world, with a self-operated shipping capacity of approximately 3 million TEUs. As for ports, the company operates and manages 224 container berths around the world, with a total annual design and processing Capacity of 141 million TEUs; the company's SynCon Hub platform provides customers with one-stop digital supply chain services.

Company Performance review

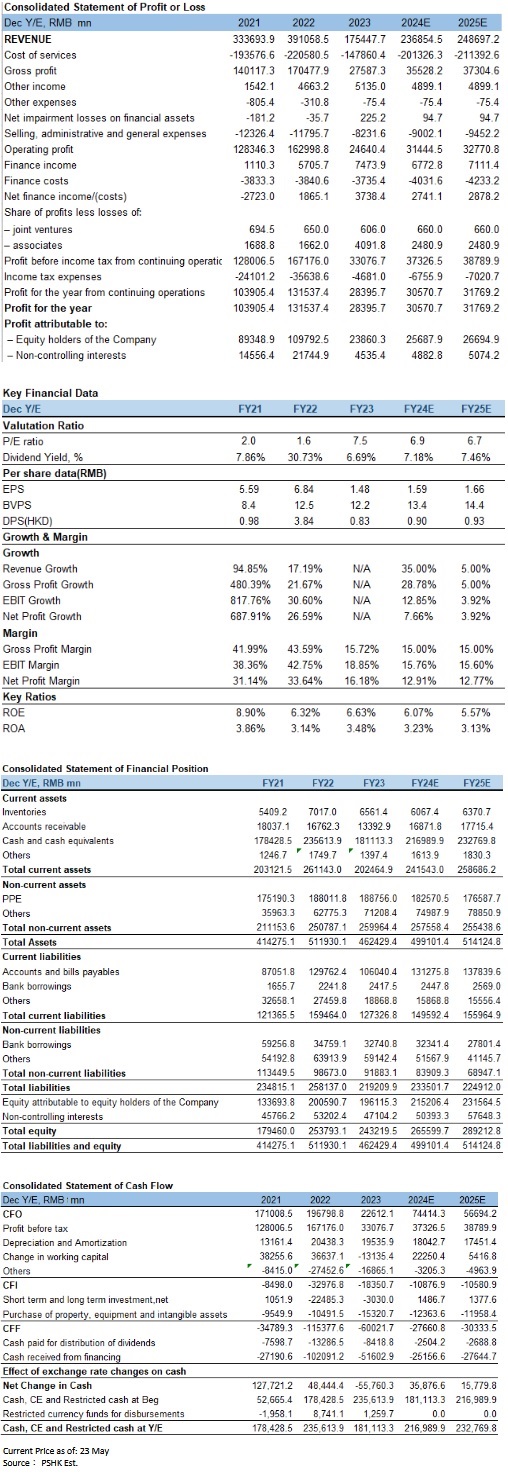

The company's Q1 revenue in 2024 was 48.27 billion yuan (RMB, the same as below), an increase of 1.94% YoY; the net profit attributable to shareholders of listed companies was 6.76 billion yuan, a decrease of 5.23% YoY; EPS was 0.42 yuan, a decrease of 4.55 % YoY. The decrease in profits was mainly due to the fact that the container shipping industry was facing many challenges such as weakening transportation and demand, rising capacity supply, and geopolitical tensions. The market freight level has dropped significantly compared with 2022. Since the growth in demand is far less than the growth in shipping capacity, the container shipping market shifted from a weak balance between supply and demand to oversupply from 2023. At the end of 2023, tensions in the Red Sea continued to escalate, and the supply and demand relationship had been improved in the short term, but it did not change the situation of wide supply and weak demand in the container shipping market.

Industry Analysis

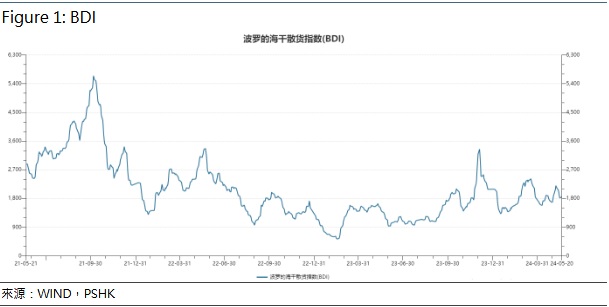

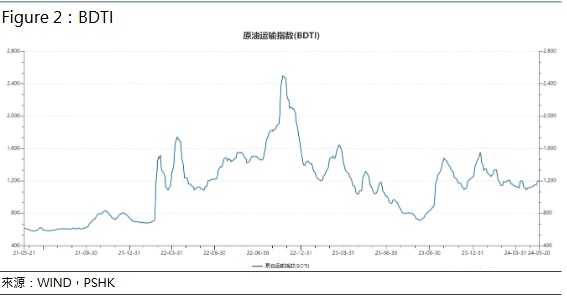

The Baltic Dry Bulk Index (BDI) index measures the transportation costs of iron ore, coal, grain, etc. It is a leading indicator of the global economy. It is calculated by the weight of 40% BCI, 30% BPI, and 30% BSI. It is the economic indicator of the shipping industry. Indicator, including changes in dry bulk trading volumes in the shipping industry. The BDTI index mainly measures oil transportation situations.

The Red Sea incident caused a large number of containers to bypass the Cape of Good Hope, but the supply chain disruption caused by it has not yet fully realized. As the situation continues to fail to cool down, it may have long-term effects. As can be seen from Figure 1, the BDI index has also continued to rise, hitting a multi-month high position, and the freight rate center is expected to grow further. As shown in Figure 2, the BDTI index is also at a high level.

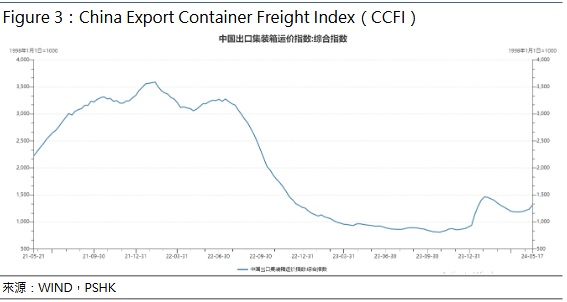

The China Export Container Freight Index (CCFI) selects 12 routes as representatives among the numerous export container shipping routes, and calculates the freight index based on the freight rates and container volumes of these routes. The data reflects real-time price trends of container shipping exported from China ports. As can be seen from Figure 3, the CCFI composite index has increased significantly compared with last year.

Company Business

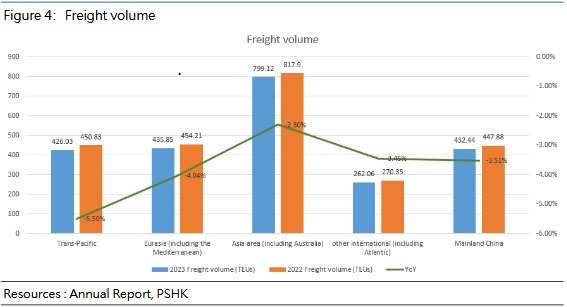

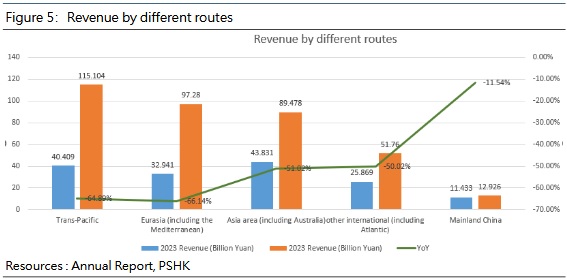

In 2023, the cargo volume of the group's container shipping business was 24.41 million TEUs, a decrease of 3.51% compared with the same period last year. As of the end of March 2024, the group's operating fleet includes 510 container ships, with a shipping capacity of 3.11 million TEUs. The group's cargo volumes (TEU) in 2023 by route were as below: Trans-Pacific 4.26 million, a decrease of 5.5% YoY; Eurasia (including the Mediterranean) 4.36 million, a decrease of 4.04% YoY; Asia area (including Australia) 7.80 million, a decrease of 2.3% YoY; other international (including Atlantic) 2.62 million, a decrease of 3.07% YoY; Mainland China 4.32 million, a decrease of 3.45% YoY, totaling 23.56 million, a decrease of 3.51% YoY.

In 2023, the group's route revenue by route was as below: Trans-Pacific 40.41 billion yuan, a decrease of 64.89% YoY; Eurasia (including the Mediterranean) 32.94 billion yuan, a decrease of 66.14% YoY; Asia area (including Australia) 43.83 billion yuan, a decrease of 51.02% YoY; other international (including Atlantic) 25.87 billion yuan, a decrease of 50.02% YoY; mainland China 11.43 billion yuan, a decrease of 11.54% YoY.

Valuation and recommendation

COSCO SHIPPING Holdings is assisting the Silk Road Sea and ASEAN routes have been upgraded. At the end of 2023, two new Southeast Asia routes operated by NEW GOLDEN SEA SHIPPING PTE.LTD, a subsidiary of COSCO SHIPPING Holdings, departed from Tianjin and Shanghai. In January 2024, NEW GOLDEN SEA SHIPPING PTE.LTD launched two new South Asia route services. Against the background of increasingly close economic and trade exchanges between Northeast China and India, COSCO SHIPPING Holdings continues to optimize the layout of the South Asia route service network and increase the coverage of the foreign trade route network in Northeast China. On January 11, 2024, the first foreign trade container directly to India line (the route "Dalian-India" Express (CIX3) was officially opened for operation at the CSP Dalian Container Terminal under COSCO SHIPPING Holdings. It fills the gap in direct shipping services from Dalian Port to India, opens up the maritime logistics channel from Northeast China to South Asia, and realizes the first shipping with full goods. In February, 2024, COSCO Shipping Lines (Morocco) was officially launched and started operations in Casablanca, which means that COSCO Shipping Lines has embarked on a new journey in its business development in Northwest Africa. In March, 2024, the Ocean Alliance, where the company's dual brands are located, released DAY8 route products. The products maintain the stability and consistency of services. A total of approximately 355 ships, approximately 4.82 million TEU transport capacity, and more than 480 sets of direct port-to-port services have been invested.

Looking forward to 2024, with the interest rate hike cycle in Europe and the United States coming to an end, inventory replenishment in Europe and the United States restarting, the "One Belt and One Road" deepening cooperation, and the rise of emerging markets, global commodity trade is expected to restart and recover, which may drive the growth of global container shipping market demand. From the industry perspective, the EU will cancel the antitrust exemption for the liner industry this year, coupled with changes and adjustments in the global container shipping alliance, market competition may become more intense.

The Red Sea incident has had a greater impact on the entire shipping industry, mainly because this area is the most economical and convenient shipping channel connecting Europe and Asia. The current detour will undoubtedly significantly increase transportation time and transportation costs. The resolution of the Red Sea crisis depends on when the conflict between Hamas and Israel ends. In view of the current situation and the fact that many impacts have not yet been fully realized, freight rates are still expected to rise in the second quarter.

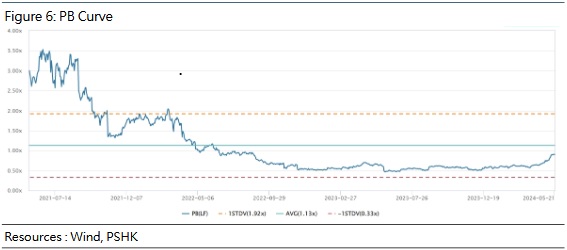

We predict that the company's revenue will be 236.86 billion yuan and 248.70 billion yuan respectively in 2024 and 2025, with EPS of 1.59/1.66 yuan; BVPS of 13.4 and 14.4, corresponding to P/B of 0.83/0.77x. The company's average P/B in the past three years is about 1.13. The current situation in the Red Sea is still volatile. The company is given a 0.95x P/B in 2024 and an "Accumulate" rating of 13.72. (Current price as of May 23)

Risk factors

Macro-environmental risks, geopolitical risks, lower-than-expected freight rates, and deteriorating competitive situation risks.

* The analyst has a financial interest in the listed corporation covered in this report.

Financial

Click Here for PDF format...