Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

Utilities, Commodity, Shipping (Margaret Li)

Automobile & Air (Zhang Jing)

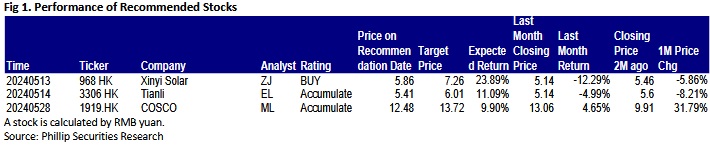

This month I released 1 initiation report of Xinyi Solar (968.HK).

Xinyi Solar, established in 2006, is the world's largest photovoltaic (PV) glass manufacturer and one of the two oligopolies in the industry. The Company's revenue mainly comes from two core business, namely the sales of PV glass and the operations of solar farms. They contributed to 88.5% and 11.2% of the total revenue, respectively, (according to the 2023 annual report) and 71% and 29% of the gross profit, respectively.

From the listing in 2013 to 2023, Xinyi Photovoltaic quickly raised its revenue and net profit, thanks to the rapid growth of the PV industry. Meanwhile, its ten-year compound annual growth rates of the total revenue and the net profit were 29.8% and 30%, respectively. As of the end of 2023, its daily melting capacity of PV glass amounted to 25,800 tons, nearly 13 times the 2,000 tons at the end of 2013. At the end of 2023, the Company's cumulative grid-connected installed capacity reached 5,944MW, wherein 3,695MW was indirectly held through Xinyi Energy.

Over the past eight years, the gross profit margin maintained between 26% and 54%. Specifically, the fluctuations in the gross profit margin of solar farm operations business were relatively small and between 68% and 77%. Because of the greater impacts of the industry cycle, the fluctuations of PV glass business were between 21% and 50%. Especially, driven by short supply in 2020, the gross profit margin of PV glass used to reach 49%, and the diluted ROE was between 18% and 42%. However, the figures have fallen in recent years. Besides the impact of the industry cycle, the Company reduced financial leverage, and the asset-liability ratio declined from 55.8% in 2016 to 37.4% in 2023.

The FY2023 result report revealed that, the Company's annual revenue stood at HKD26.63 billion, up by 29.6%yoy, and the annual net profit attributable to the parent company was HKD4.19 billion, rising by 9.6%yoy, exceeding the previous market expectations. In the second half of the year, the revenue reached HKD12.94 billion with yoy and hoh increases ratio of 29% and 16%. The net profit attributable to the parent company amounted to HKD2.51 billion. Different from the year-on-year decrease of 27% in the first half of the year, the figures in the second half sharply grew by 41% and 96%yoy and hoh.

The main reason for the lower and then higher results is that the PV glass business in the first half of the year was affected by the increased raw material and energy costs and the decreased average selling price (ASP). Yet, the sharp fall in the prices of polysilicon and PV components from the second quarter triggered the accelerated downstream demand for installed capacity in the second half of the year. Coupled with a slowdown in the growth of PV glass capacity, the supply and demand in the PV glass market was improved. Due to the declined ASP, higher raw material prices, and unfavorable exchange rate direction, the overall gross margin dropped by 3.4 percentage points to 26.6% from 30% in 2022.

With respect to future planning, the Company will continue to maintain an aggressive pace of capacity expansion. A total of six production lines with a capacity of 6,400 tons are planned to be launched in 2024, including four in Anhui Province and two in Malaysia. Moreover, the Company intends to build new production lines in Yunnan and Jiangxi Provinces as well as Indonesia after 2025. In regard to solar farms, Xinyi Solar has decided to set up more prudent objectives for installed capacity, and planned to add 300MW of grid-connected capacity in 2024. As a result, the Company's overall capital expenditure for 2024 is planned to be HKD7 billion, significantly declining from HKD9.9 billion in 2023, and a higher weight is given to PV glass business.

After two consecutive years of unprecedented growth, it is expected that the global PV installed capacity will continue to grow in 2024, but the growth rate will be slower or not as high as that in the past two years but still higher than the long-term historical average. However, PV glass is expected to grow faster than the PV installed capacity. For capacity expansion, Xinyi Solar adopts a positive attitude. It is expected that the cost advantage will be reinforced, and the leading position will be consolidated. Moreover, the Company's overseas capacity is expected to double this year, and its overseas products enjoy a high premium. If expanded smoothly, overseas products will become another growth point for the Company.

We are optimistic about the Company's future in consideration of the alleviated pressure in PV glass inventory, the stabilized selling price, and the weak prices of sodium carbonate and natural gas in the medium term. We estimate that the Company's earnings per share (EPS) in 2024 and 2025 will be HKD0.60 and HKD0.76. Taking into account the Company's leading advantage and new capacity to build, P/E ratios in 2024 and 2025 are expected to be 12x and 9.6x, with Target Price of 7.26 HKD, BUY rating.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released reports of Tianli International (01773.HK).

Established in 2002, Tianli International (01773.HK) is a comprehensive education service operator in Western region of the PRC, providing with comprehensive education management and diversified services. With a presence in Sichuan province where Tianli International is based in, its school spans across 36 cities in Inner Mongolia, Shandong, Henan, Guizhou, Jiangxi, Zhejiang, Yunnan, Gansu, Anhui, Guangxi, Guangdong, Shaanxi, Shanghai, Chongqing and Hubei. As of 29 February 2024, it principally provided students with comprehensive education services in 50 schools. For the same period, the number of full-time teachers employed by Tianli self-owned schools was 2,060 (as of 28 February 2023: 1,654). There were 36,708 high school students in the Company's school network as at the beginning of the 2023 fall semester, representing an increase of 43.8%, among which the enrollment number of new high school students was 19,071, representing an increase of 41% as compared with the enrollment number of new high school students as at the beginning of the 2022 fall semester.

For the year ended 31 August 2023 (FY2023), revenue increased by 160.3% to RMB2302 million, primarily driven by increase of revenue from comprehensive educational services and sales of products. Adjusted profit for the year was RMB366 million, an increase of 276.4% YoY. During the period, basic EPS were RMB15.90 cents, the full-year dividend was RMB4.77 cents per share, and the dividend payout ratio was 30%.

The gross profit was RMB779 million, representing an increase of 165.3%, primarily due to the increase in the number of high school students enrolled and the revenue from the provision of comprehensive quality services and product sales. The gross profit margin was 33.8%, representing a slight increase of 0.6 percentage points.

For the six months ended 29 February 2024 (1HFY2024), revenue increased by 73.8% to RMB1645 million. Among which, revenue from comprehensive educational services increased by 64.4% to RMB851 million, which is primarily due to the increase in high school students enrollment; the end of the pandemic, which led to a significant growth in the study tour business. Sales revenue increased by 1.8 times to RMB474. The revenue from canteen operations increased by 19.9% to RMB294 million, primarily due to the increase in the number of students served by the company. The revenue from management and franchise fees increased by 34.9% to RMB26.056 million, primarily because of the addition of three schools to the company's entrusted school network. The gross profit margin 35.4%, representing a slight decrease of 3.8 percentage points. Adjusted profit was RMB319 million, a year-on-year increase of 70.0%.

As the policy further defines and clarifies the boundaries of off-campus training, and with the industry's regulatory policies becoming more transparent, with a focus of for-profit high schools, providing students with comprehensive operational services, including but not limited to a series of other value-added services such as online campus store, logistical integrated services, study guidance for arts and sports oriented schools, international education, overseas studies consulting and study tours, Tianli is expected to benefit from sustainable development.

Utilities, Commodity, Shipping (Margaret Li)

This month I released reports of COSCO SHIPPING Holdings Co., Ltd (1919).

The company's Q1 revenue in 2024 was 48.27 billion yuan (RMB, the same as below), an increase of 1.94% YoY; the net profit attributable to shareholders of listed companies was 6.76 billion yuan, a decrease of 5.23% YoY; EPS was 0.42 yuan, a decrease of 4.55 % YoY. The decrease in profits was mainly due to the fact that the container shipping industry was facing many challenges such as weakening transportation and demand, rising capacity supply, and geopolitical tensions. The market freight level has dropped significantly compared with 2022. Since the growth in demand is far less than the growth in shipping capacity, the container shipping market shifted from a weak balance between supply and demand to oversupply from 2023. At the end of 2023, tensions in the Red Sea continued to escalate, and the supply and demand relationship had been improved in the short term, but it did not change the situation of wide supply and weak demand in the container shipping market.

COSCO SHIPPING Holdings is assisting the Silk Road Sea and ASEAN routes have been upgraded. At the end of 2023, two new Southeast Asia routes operated by NEW GOLDEN SEA SHIPPING PTE.LTD, a subsidiary of COSCO SHIPPING Holdings, departed from Tianjin and Shanghai. In January 2024, NEW GOLDEN SEA SHIPPING PTE.LTD launched two new South Asia route services. Against the background of increasingly close economic and trade exchanges between Northeast China and India, COSCO SHIPPING Holdings continues to optimize the layout of the South Asia route service network and increase the coverage of the foreign trade route network in Northeast China. On January 11, 2024, the first foreign trade container directly to India line (the route "Dalian-India" Express (CIX3) was officially opened for operation at the CSP Dalian Container Terminal under COSCO SHIPPING Holdings. It fills the gap in direct shipping services from Dalian Port to India, opens up the maritime logistics channel from Northeast China to South Asia, and realizes the first shipping with full goods. In February, 2024, COSCO Shipping Lines (Morocco) was officially launched and started operations in Casablanca, which means that COSCO Shipping Lines has embarked on a new journey in its business development in Northwest Africa. In March, 2024, the Ocean Alliance, where the company's dual brands are located, released DAY8 route products. The products maintain the stability and consistency of services. A total of approximately 355 ships, approximately 4.82 million TEU transport capacity, and more than 480 sets of direct port-to-port services have been invested.

Click Here for PDF format...