Company Profile

Hengan founded in 1985, is a famous manufacturer of household paper and maternal & child hygiene products. The market shares of the three leading products, namely women's sanitary napkins, baby diapers, and household tissues, is among the best in the domestic market.

FY2023 still records solid growth

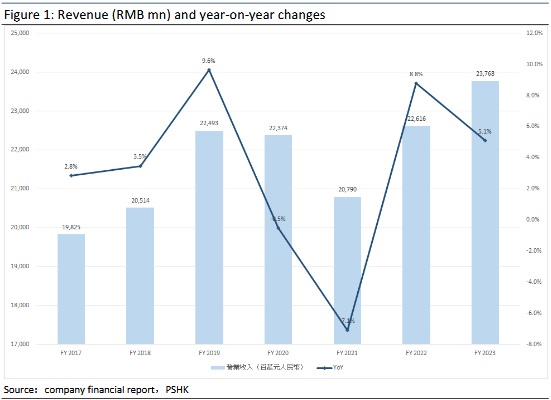

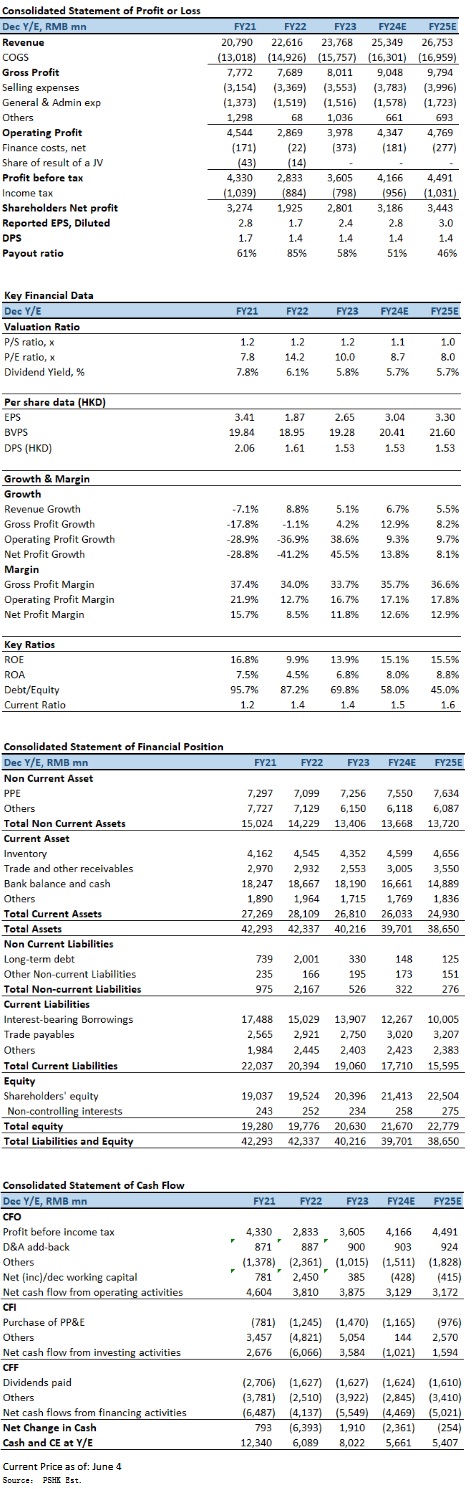

For the year ended 31 December 2023 (FY2023), Hengan's revenue increased by 5.1% to RMB23,768mn, above market expectation. During the year, operating profit increased significantly by 38.6% to RMB3,978mn (FY2022: RMB2,869mn). Although the depreciation of the Renminbi against the US dollar and the HK dollar during the year resulted in an operating foreign exchange loss after tax of RMB150mn, the loss was significantly reduced by about 83.6% compared with the operating FX loss before tax of RMB901mn in 2022. Therefore, profit attributable to shareholders of the Company was RMB2,801mn (FY2022: RMB1,925mn), representing a significant yoy increase of 45.5%. Excluding the operating FX loss after tax, profit attributable to shareholders of the Company increased by 4.3% yoy, mainly reflecting the improvement in the company's gross profit margin as a result of the decline in the cost of wood pulp and upgrades of products. Basic EPS was RMB2.415 (FY2022: RMB1.657), with full-year dividend RMB1.40 per share, unchanged yoy.

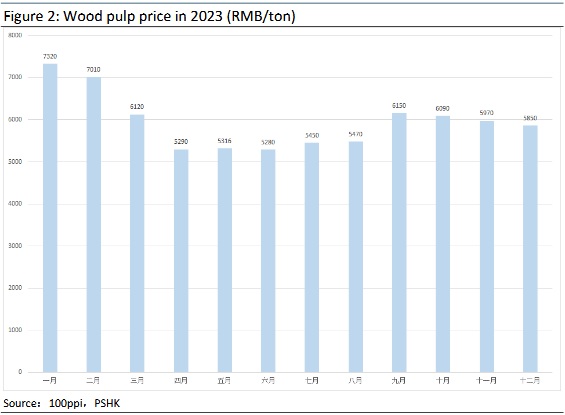

During the year under review, raw material prices dropped in the second half of the year, leading to intensified market promotions and price competition. The decline in the price of wood pulp, the main raw material for tissue paper, in the second half of the year compared to the first half of the year, coupled with the robust growth in the company's upgraded products and premium product series resulted in a significant improvement in the gross profit of the tissue paper business. FY2023, the company's overall gross profit increased by 4.2% to RMB8,011mn (FY2022:RMB7,689mn). Although the gross profit margin was under pressure in the 1HFY2023, the overall gross profit margin for the full year still recorded at 33.7% (FY2022: 34.0%), almost consistent with last year. Gross profit the 2HFY2023 even significantly improved to 36.5% (2HFY2022: 32.8%). It is expected that in 2024, premium high margin products will continue to experience significant growth, leading to a continuous improvement in the gross profit margin.

By business segment, despite fierce market competition and aggressive pricing and promotional strategies of other brands, the revenue of the company's sanitary napkin business increased by 0.4% to RMB6,178mn (FY2022: RMB6,156mn), accounting for 26.0% (FY2022: 27.2%) of the Group's overall revenue, outperforming the sales performance in the overall sanitary napkin industry. Benefiting from brand premiumisation and the steady increase in the proportion of upgraded products, as well as the decline in the price of petrochemical raw materials, the main raw material for sanitary napkins in the second half of the year compared with the first half of the year, the gross profit margin of the sanitary napkin business stood at 66.0% in the 2HFY2023, representing an improvement from 61.8% in the 1HFY2023, while the overall gross profit margin in FY2023 was 63.8%, decrease 3 percentage points yoy.

For the company's tissue paper business, the revenue increased remarkably by 12.2% to RMB13,748mn (FY2022: RMB12,248mn), outperforming the industry's average growth rate and maintaining a leading market share. The sales of the tissue paper business accounted for 57.8% of the company's overall revenue (FY2022:54.2%). Although the company moderately increased promotions in the 2HFY2023, resulting in higher promotional expenses, it benefited from product upgrades and the increased proportion of high-margin products, as well as a drop in wood pulp costs. As a result, the gross profit margin for the 2HFY2023 improved significantly from 17.7% in the 1HFY2023 to 26.1% (2HFY2022: 18.5%), while the gross profit margin for 2023 increased to 21.7%, (FY2022: 20.7%). The company's upgraded and premium tissue paper products achieved outstanding sales. Among them, the sales of the “Cloudy Soft Skin” series recorded sales of more than RMB1.30 billion, increased by around 26.6% and accounting for 12.0% of the overall tissue paper sales. In terms of the company's wet wipes business, the sales for the year were RMB931mn (FY2022:RMB842mn), recording a sales growth of nearly 10.5%, accounting for 6.8% of the overall sales of the tissue paper business (FY2022: 6.9%).

The sales of the company's disposable diaper business increased by 4.3% to RMB1,254mn (FY2022: RMB1,202mn), accounting for 5.3% (FY2022: 5.3%) of the company's overall revenue. In terms of gross profit margin, the price decrease in petrochemical raw materials for disposable diapers in the second half of the year led to an decrease in costs of sales, coupled with the increase in the proportion of sales of the higher-margin “Q.MO” products and premium adult disposable diapers helped increase the gross profit margin to more than 40.0% in the 2HFY2023, which is a significant improvement from 36.0% in the 1HFY2023. The gross profit margin of the diaper business in 2023 rose to 38.1% (FY2022: 36.9%).

Regarding other income and household products, the company's revenue for the year, which mainly includes revenues from raw material trading business, household products business, and Wang-Zheng Group in Malaysia, decreased by 14.0% yoy to RMB2,587mn (FY2022: RMB3,009mn). The decline was mainly due to the company's preference to reserve raw materials for the manufacturing of products and ensure reasonable profits from its raw material trading business. As a result, revenue from raw material trading business dropped significantly by 13.6% to RMB1.4 billion (FY2022: RMB1.6 billion).

E-commerce channels maintained strong momentum

The company's e-commerce and new retail channels (including Retail Integrated and New Channel) sales for the year soared over 17.7% to RMB7.16 billion (2022: RMB6.1 billion), bringing the proportion of e-commerce sales up to 30.1% (2022: 26.9%) of the company's overall sales. During the year, the tissue paper business in e-commerce and new retail channels (including Retail Integrated, community group-buying, etc.), with a sales growth of 26.1%, accounting for nearly 35.3% of the overall sales of tissue paper; new retail channels contributed 26.5% and 52.8% of contribution to the sales of sanitary napkin business and disposable diaper business respectively.

Investment Thesis

Despite a challenging operating environment, Hengan leverages its strong comprehensive competitive advantages and effective profit-focused sales strategies to continue expanding its market share and further solidify its robust business resilience. The company's three core business segments—tissue paper, sanitary napkins, and diapers—have maintained steady growth in revenue over the past two years. The decline in raw material prices in the second half of last year intensified industry marketing and price competition. However, the company prudently allocated promotional resources and continued to record significant growth in high-end, high-margin products. Gross profit margins are expected to remain stable. Hengan maintains a healthy financial condition with a significant improvement in its debt ratio to 69.8%, placing it in a net cash position. We expect FY2024E-FY2025E EPS to be RMB2.77 and RMB3.01 respectively, with PT of HKD35.18, implies a FY2024E P/E of 11.6x (~5-yrs historical average). Our investment rating is “Buy”.

Risk factors

1) The price of raw materials continues to rise; 2) market competition intensifies; 3) channel development is not as expected; and 4) Sharp fluctuations in FX.

Financial

Click Here for PDF format...