Overview

China Oilfield (2883.HK) is mainly engaged in drilling work, providing oil and gas well technology, offshore work vessel services and transportation. China Oilfield Services Limited is the Asia's largest comprehensive oilfield service provider. Its services span all stages of offshore oil and gas exploration, exploitation and production. Its business is divided into four major categories: geophysical acquisition and surveying services, drilling services, well services and marine support services.

Company Performance review

The company's revenue in the first quarter of 2024 was 10.15 billion yuan (RMB, the same as below), a year-on-year increase of 20.0%; the net profit attributable to shareholders of listed companies was 636 million yuan, a year-on-year increase of 57.3%, which mainly due to the fact that the company proactively deployed global regional markets in the upswing phase of the industry, continued to strengthen core competitiveness, and leveraged the advantages of a complete industrial chain to promote a year-on-year increase in the main workload and revenue of each segment during the period. EPS was 0.13 yuan/share, a year-on-year increase of 62.5%; weighted average net assets earnings ratio was 1.5%, a year-on-year increase of 0.5 percentage points.

Main business analysis

Drilling services

The company is the largest offshore drilling contractor in China and one of the internationally well-known drilling contractors. It mainly provides relevant drilling and well completion services such as jack-up drilling rigs, semi-submersible drilling rigs and land drilling rigs. At the end of 2023, the Company operated and managed a total of 60 drilling rigs (of which 46 are jack-up drilling rigs, and 14 are semi-submersible drilling rigs), etc. In 2023, revenue from drilling services amounted to 12,051.2 million yuan, a year-on-year increase of 16.6%. The “NH4” rig successfully installed the first shallow-water underwater wellhead water injection tree in China, realizing the industrial application of the shallow-water underwater wellhead water injection system; the “HYSY943” rig successfully completed the operation of “new, excellent and fast” project, the first unmanned rig of CNOOC, speeding up 22.15%; the “KAI XUAN YI HAO” rig successfully completed the operation of a certain well section in the Bohai Sea, shattering a new record for the longest open-hole section in the Bohai Sea; the “HYSY982” rig successfully completed the drilling of the first deepwater high-pressure development well of CNOOC; the “China Merchants Hailong 7” rig completed the operation of a high-value well in the Americas with high standards.

As of 31 March 2024, affected by the off-lease drilling rig, the operating days of drilling rigs of the company amounted to 4,388 days, representing a decrease of 77 days or 1.7% as compared with the same period last year, among which the operating days of jack-up drilling rigs amounted to 3,420 days, representing a decrease of 2.6% as compared with the same period last year, and the operating days of semi-submersible drilling rigs amounted to 968 days, representing an increase of 1.6% as compared with the same period last year. The calendar day utilization rate of drilling rigs remained stable as compared with the same period last year, among which the calendar day utilization rate of jack-up drilling rigs was 80.2% and the calendar day utilization rate of semi-submersible drilling rigs was 76.0%.

Well services

The company is the main provider of China offshore well services together with the provision of onshore well services. The company provides professional well services, including but not limited to logging, drilling & completion fluids, directional drilling, cementing, well completion, well workover, stimulation, etc. In 2023, revenue from well services amounted to 25,717.5 million yuan, a year-on-year increase of 31.4%.

The company has achieved leaping development of self-developed” Xuanji” high-end drilling technical equipment, and further realized the large-scale marine application, achieving more than 1,700 well times and accumulated footage of over 1.6 million meters, and the good run ratio was improved to 95.11%.

Marine support services

The company operates and manages the largest offshore operation fleet with the most comprehensive functions in China. The company can provide comprehensive support and services, including anchor handling for different water level, towing of drilling rigs/engineering barges, offshore transportation, oil/gas field standby, firefighting, rescue, oil spill assisting, for offshore oil and gas exploration, development, construction and oil/gas field production, etc. In 2023, revenue from marine support services amounted to 3,938.8 million yuan, a year-on-year increase of 5.9%.

As of 31 March 2024, the operation and management of vessels under the marine support services of the Company amounted to 172 vessels in total and the operating days in current period amounted to 14,227 days, representing an increase of 532 days or 3.9% as compared with the same period last year. Among which, 12 LNG powered vessels operate in Bohai Sea and South China Sea and the operating days in the first quarter amounted to 1,014 days. It is expected to reduce 12,000 tons of carbon emissions every year. The calendar day utilization rate of self-owned vessels increased by 1.0 percentage points as compared with the same period last year.

Geophysical acquisition and surveying services

The Company is a major supplier for China offshore geophysical acquisition and surveying services and a solid competitor and a provider of effective and high quality service in the global geophysical exploration. At the end of 2023, the Company owns 5 towing streamer vessels, 4 submarine seismic vessels, 4 integrated marine surveying vessels and 2 support vessels for operation in deep water. Services for clients include but not limited to providing services of wide azimuth, broadband, high density seismic acquisition services, ocean bottom cable and ocean bottom node multi-component seismic acquisition services, as well as integrated offshore surveying services.

As of 31 March 2024, with the impact of time schedule of operating, the 2D acquisition operation volume was 4,043 kilometers, representing a decrease of 7,960 kilometers as compared with the same period last year; the 3D acquisition operation volume was 6,696 square kilometers, representing an increase of 5,585 square kilometers as compared with the same period last year, which was mainly due to the increase in overseas operations. The ocean bottom operation volume was 241 square kilometers, representing an increase of 15.3% as compared with the same period last year.

Valuation and recommendation

Crude oil prices had been at volatile highs in the past year. OPEC+ agreed in June to cancel voluntary production cuts gradually after the third quarter while retaining other restrictive measures. According to the STEO in July, EIA now expects the average brent crude oil spot price will be US$86.37 and US$88.38 per barrel in 2024 and 2025 respectively, US$87.97 per barrel in the third quarter of 2024, and US$89.64 per barrel in the fourth quarter of 2024. In July, the International Energy Agency (IEA) forecasts the oil demand growth of 2024 will be 970,000 barrels/day, almost the same as last month. And the oil demand growth of 2025 is expected to be 980,000 barrels/day, decreasing 50,000 barrels/day from the previous forecast.

According to S&P Global's "Global Upstream Capital Expenditure Research Report", global upstream exploration and development capital expenditures was US$565.2 billion in 2023, a year-on-year increase of 10.75%. Among them, offshore oilfield capital expenditure was US$163.8 billion, a year-on-year increase of 13.43%. China Oilfield expects capital expenditures in 2024 will be approximately RMB 7.4 billion, which will be mainly used for equipment investment and upgrading, technical equipment upgrading, technology research and development investment and base construction.

According to Spears & Associates` "Oilfield Services Market Report", the global oilfield services industry market value was US$306.3 billion in 2023, a year-on-year increase of 12.40%. It is expected that the global oilfield services industry market value will continue to grow in 2024. Domestically, according to the "Guiding Opinions on Energy Work in 2024" issued by the National Energy Administration, the oil and gas industry will conduct in-depth research on implementation of the medium- and long-term oil and gas development strategy of increasing reserves and production, increase efforts of oil and gas exploration and development, promote stable production of old oil fields, accelerate the construction of new areas and strengthen the construction of oil and gas production capacity in the key areas of "two deep areas, unconventional and stable production of mature oil fields ", it is predicted that the domestic oilfield service market will continue to maintain a continuous upward trend. Generally speaking, it is conducive to the development of China Oilfield businesses.

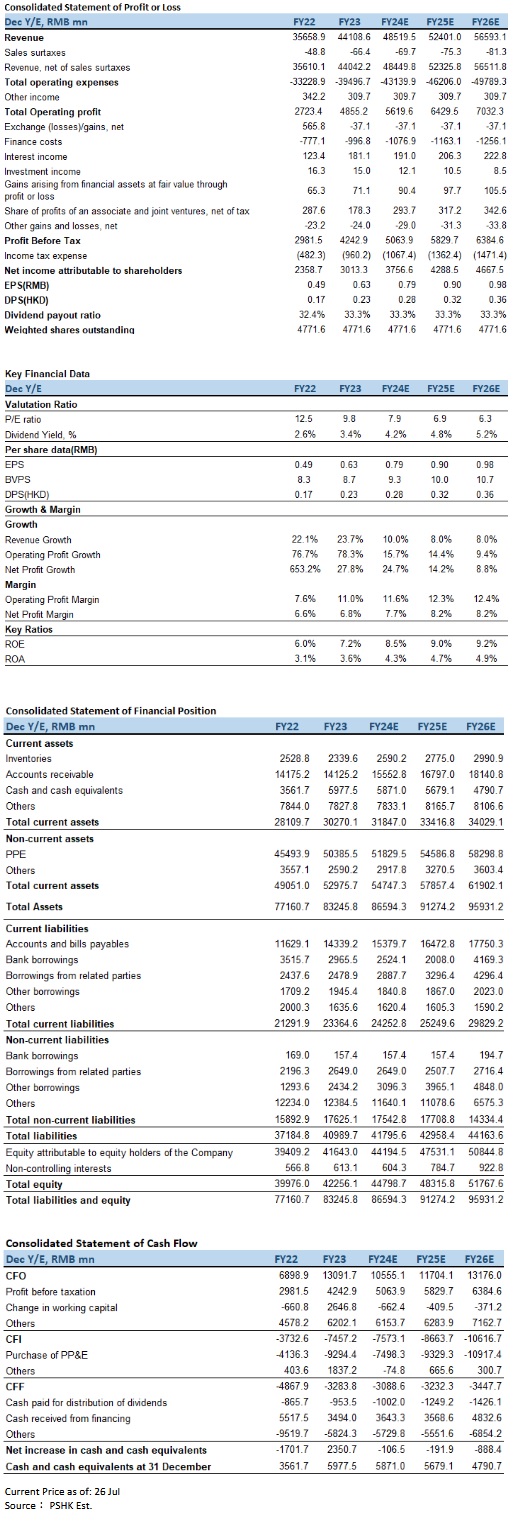

We predict that the company's revenue will be 48.52 billion yuan, 52.40 billion yuan, and 56.59 billion yuan in 2024-2026 respectively, with a compound annual growth rate of 8.7%, earnings per share EPS of 0.79/0.90/0.98 yuan, and BVPS of 9.3 yuan and 10.0 yuan and 10.7 yuan, corresponding to P/B of 0.67x/0.62x/0.58x. The impact of the off-lease drilling rig is a short-term factor, and the impact will decrease gradually in the future. The company's net profit attributable to shareholders increased by 57% year-on-year, and its profitability has increased. We are optimistic about the company's development in 2024 and give the company a P/B of 0.75 times in 2024, with a target price of HK$7.51 and an "Accumulate" rating. (Current price as of July 26)

Risk factors

Crude oil price fluctuations, geopolitical conflicts, and corporate capital expenditures exceeded expectations.

* The analyst has a financial interest in the listed corporation covered in this report.

�Financial

Click Here for PDF format...