Company profile:

Tuopu Group is an industry leader in the field of automotive NVH that is capable of synchronous design with the original equipment manufacturer. In recent years, on the basis of the original business of shock absorbers and interior functional parts, the Company has proactively arranged the module of the lightweight chassis system and the automotive electronics business as the future Ŗ+3" strategic development projects, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles.

Investment Summary

Revenue Rose by 27% in 2023, and Performance Leaped by Over 40% in Q1 2024

In 2023, the Group recorded a revenue of RMB19.7 billion, up 23.2% yoy, net profit of RMB2,151 million attributable to the parent company, up 26.5% yoy, and net profit of RMB2,021 million attributable to the parent company excluding non-recurring items, up 22% yoy and about 10% lower than our mid-year projection. By quarter, the net profit attributable to the parent company was up 16.7% to RMB450 million, up 100% to RMB644 million, up 0.43% to RMB503 million, and up 12.6% to RMB554 million, respectively, in Q1, Q2, Q3 and Q4 2023. We reckon that the sales increase of downstream customers, product line expansion of the Group, and commissioning of new electronic products for various car models, such as pneumatic suspension, brake-by-wire and electronic adjustable steering column, drove the Group's performance to grow. A forward-looking layout has been made in new energy vehicles (NEVs). Especially, the Group's lightweight chassis and electronic business started to enter the harvesting period and contribute to business performance.

The year 2023 witnessed the global delivery of 1,810 thousand units of NEVs by the Group's largest customer, Tesla, with a yoy increase of 38%. Among Chinese vehicle manufacturers, the yoy growth rate of the sales volume of Geely Auto was 18%, higher than the industry average of 11%, and the annual sales of NIO, AITO, Li Auto and BYD rose by 31%, 26%, 182% and 62% yoy, respectively. The sales growth of both new and existing customers drove the Group's revenue and profit to increase.

In FY2024Q1 the momentum for the Group's performance growth sustained, and the Group recorded a revenue of RMB5.69 billion, up 27.3% yoy and 2.5% qoq, in Q1 2024, as well as a net profit of RMB670 million attributable to the parent company, up 43.3% yoy and 17.3% qoq, and a net profit of RMB600 million attributable to the parent company excluding non-recurring items, up 41.9% yoy and 14.6% qoq. In Q1 2024 Q1, Chinese vehicle manufacturers Li Auto and AITO recorded a sales volume of 80.4 thousand and 85.8 thousand vehicles, respectively, up 52.9% and 636.27% yoy, and Geely Auto recorded a sales volume of 476 thousand vehicles, up 49% yoy.

According to the latest positive profit alert, the total revenue for FY2024H1 was 12.227 billion yuan, up 33.47% yoy; The net profit attributable to the parent company was 1.452 billion yuan, up 32.69% yoy; Correspondingly revenue for 24Q2 was 6.538 billion yuan, up 39.3% yoy and 14.9% qoq; The net profit attributable to the parent company was 806 million yuan, up 25.2% yoy and 24.9% qoq. Shipments and result continue to beat consensus growth.

Profitability Soundly Improved

Thanks to the continuous practice of the Tier 0.5 business model, the Group's matching amount of single vehicles increased constantly to RMB30 thousand approximately. In terms of profitability, the net profit margin for the full year 2023 grew by 0.29 percentage points, from 10.62% in the same period of the previous year to 10.91%. By quarter, the net profit margin was 10.16% (down -0.51 ppts yoy), 13.75% (up 3.35 ppts yoy), 10.1% (down 1.5 ppts yoy) and 9.85% (down 0.2 ppts yoy), respectively, in Q1, Q2, Q3 and Q4 2023. In Q1 2024, the gross margin was 22.43%, up 0.58 ppts yoy, and the net profit margin was 11.39%, up 1.23 ppts yoy.Profitability may continue to improve as the scale effect will dilute R&D costs and capital expenditures because of mass production and sales growth of products in the coming days, and independent parts brands will produce more and more products for middle- and high-end new energy vehicles.

The Group Highlighted Core Customers and Continued to Promote the Tier 0.5 Cooperation Model

Deepening strategic cooperation with customers with the Tier 0.5 model was more acceptable to the market with the continuous advancement of the platformisation strategy of products. Sustained rapid growth of new orders was a guarantee for the Group's high-speed sustainable development in the future.

In the domestic market, the Company's cooperation with Huawei-Seres, Li Auto, NIO, XPeng, BYD, Geely New Energy and other new energy vehicle manufacturers deepened rapidly, with a constantly rising matching amount of single vehicles. In the global market, the Group conducted all-around cooperation in the new energy vehicle sector with innovative American vehicle manufacturers A, RIVIAN and LUCID, as well as traditional American vehicle manufacturers such as FORD, GM and FCA. FAW, Geely, Huawei-Seres, Li Auto, BYD, Xiaomi Auto, Hycan, HiPhi and SAIC selected the Group as the permanent suppliers of IBS, EPS, pneumatic suspension, thermal management and smart cabin projects. Amid intensive cooperation with leading vehicle manufacturers, sales to core customers and the matching amount of single vehicles are expected to grow, and the Group may be the first to benefit from it.

Robot Actuators may be the Star Product that Boosts the Group's Growth

With the software, electrical control, motor and machinery technologies accumulated in the IBS project, the Group initiated robot actuator business. Samples of robot linear actuators and rotary actuators developed by the Group were sent to customers many times, and won recognition and praise from customers. The project calls for mass production to ramp up from the first quarter of 2024, with an initial order of 100 units per week. In January 2024, the Group announced its intent to build a production base of robot electric actuators with an investment of about RMB5 billion. The Group's production line with an annual capacity of 300 thousand sets of electric actuators was officially put into operation on January 8, the capacity of which will be improved to 100 million sets in the future. For the great potential for development of the robot industry, robot actuators may be the star product that boosts the Group's growth in the long run.

Investment Thesis

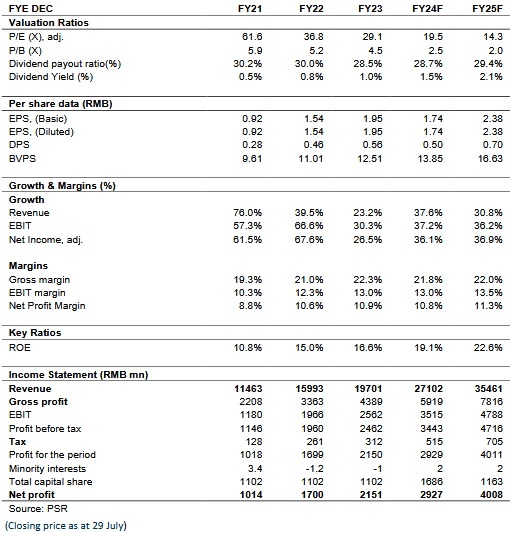

The market is concerned that Tesla's slowing growth will have a negative impact on the Group's performance, and we believe that the updates on the Group's overseas factories will help the Group earn orders from other overseas customers. The sales volume of supporting products for domestic core new energy customers such as Huawei, Xiaomi, NIO, Li Auto and BYD is expected to grow rapidly. Constant implementations of new business orders, growing single-vehicle value, rapid capacity expansion, and increasing scale effects will secure the mid- and long-term development of the Group. Taking into account the dilution of conversion of follow-on offerings, we lower the EPS estimate for 2024 to RMB1.74 from RMB1.94. So, we revise the Company's target price to RMB 51.69 yuan, respectively 30/22 x P/E for 2024/2025, a "Buy" rating. (Closing price as at 29 July)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...