Xtep International principally engages in the design, development, manufacturing, sales, marketing and brand management of sports products covering footwear, apparel and accessories for adults and children. With a diverse brand portfolio encompassing the core Xtep brand, Saucony and Merrell to strategically target the mass market, athleisure and professional sports segments, has an extensive global distribution network and more than 8,600 stores in Asia-Pacific, North America and EMEA.

Net Profit increased by 13.0% in 1H, and gross profit margin improved

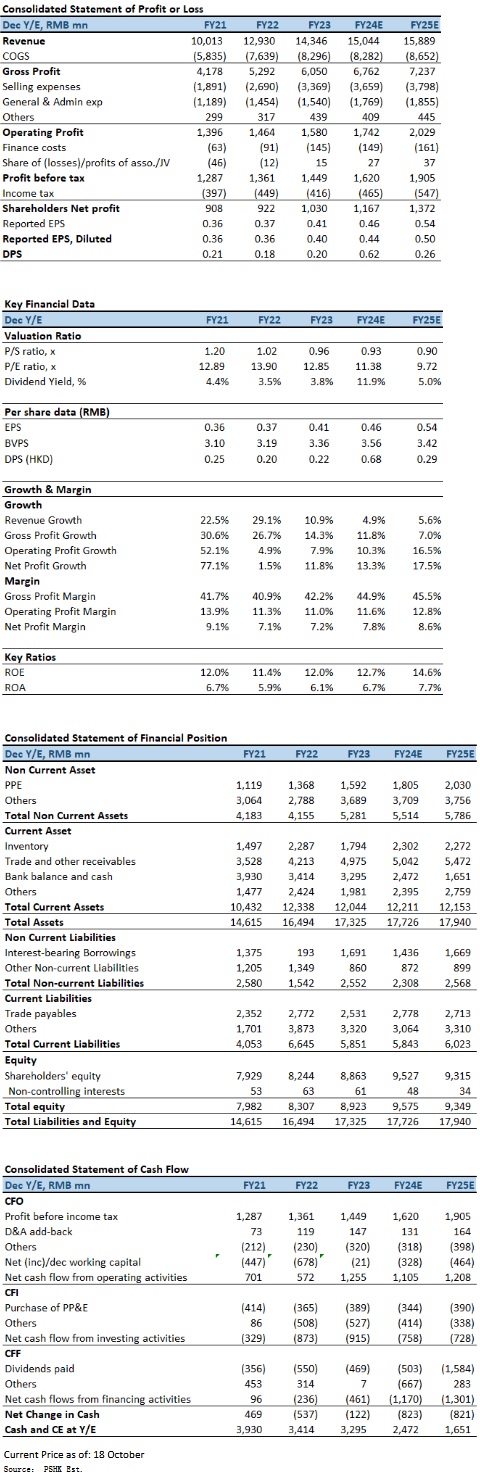

1H2024FY, Xtep’s revenue increased by 10.4% to RMB7203 million, meet market expectations, and ahead of peers. Profit attributable to ordinary equity holders grew 13.0% to RMB752 million. Basic EPS was RMB29.7 cents (1H2023FY:RMB26.4 cents). The interim dividend is HK15.6 cents (1H2023FY: HK13.7 cents, the additional special dividend is HK44.7 cents per share. If the interim dividend is taken into account, the total dividend per share will be HK60.3 cents.

Overall gross profit margin increased to 3.1 percentage points to 46.0%. This improvement was mainly driven by the higher contribution from the direct-to-consumer (DTC) model, which carries higher gross margins. Notably, there was an increased contribution from e-commerce in the Mass Market segment and a higher revenue contribution from the Athleisure and Professional Sports segments, both of which have a higher proportion of DTC operations. Selling and distribution expenses amounted to RMB1692 million, representing 23.5% of the total revenue (1H2023FY: RMB1510 million, representing 23.2% of the total revenue). The increase was mainly attributed to higher advertising and promotional costs. General and administrative expenses amounted to RMB802 million, representing 11.1% of the total revenue (1H2023FY: RMB636 million, representing 9.8% of the total revenue). Operating profit increased by 10.9% to RMB1094 million, operating profit margin improved slightly to 15.2% from 15.1%.

For the six months ended 30 June 2024, inventories turnover days decreased by 7 days to 100 days (1H2023FY: 107 days). Trade receivables turnover days increased by 8 days to 100 days (1H2023FY: 92 days). Trade payables turnover days decreased by 1 day to 110 days (1H2023FY: 111 days). The overall working capital turnover days remained stable at 90 days (1H2023FY: 88 days).

Professional sports brands maintain rapid growth

By brand nature, revenue from the mass market segment increased by 6.6% to RMB5789 million, accounting for 80.4% of the total revenue, and the segment operating profit increased by 7.6% to RMB1190 million; Revenue in the athleisure segment grew by 9.7% to RMB822 million, accounting for 11.4% of the total revenue, and the segment operating losses RMB99.2 million, compared to a loss of RMB66.3 million in RMB66.3 million in 1H2023FY; The professional sports segment saw significant growth of 72.2%, with revenue rising to RMB593 million, segment operating rising by 75.5% to RMB23.3 million.

Eliminate the losses, focus on running

On January 1 2024, Xtep completed the acquisition of Wolverine Group's interests in certain joint venture entities associated with the Merrell and Saucony brands and their subsidiaries. all Merrell and Saucony operating entities in Greater China are now wholly-owned by Xtep. Additionally, Xtep sold KP Global, which held the American sports brands K-Swiss and Palladium, to the major shareholder, the Ding family, for $151 million. The sale was accompanied by a special dividend distribution of the same amount to shareholders, equivalent to HK$0.447 per share. Since 2019, the two brands have continuously incurred losses, totaling over US$100 million. In the first three months of this year, they recorded an additional loss of approximately US$9 million, and the annual loss is expected to be similar to last year’s. This restructuring is expected to eliminate the losses KP Global brought to Xtep, improving its profitability over the next two years and beyond. The business structure will be streamlined, with a focus on running.

Company valuation

Macroeconomic challenges are making Chinese consumers more price-conscious. Xtep's main brand offers high-value professional running products, giving it strong core competitiveness as a mass-market brand. Notably, China plans to introduce new fiscal stimulus measures, including issuing approximately 2 trillion in special government bonds to address deflationary pressures and slow economic growth. The Ministry of Finance intends to issue a trillion in special bonds, primarily to stimulate consumption. Moreover, with increasing public participation in sports and national policies promoting sports development, consumer enthusiasm for sports is expected to grow. We maintain a cautiously optimistic outlook for the medium-term prospects of China's sports goods industry. We expect FY2024E-FY2025E EPS to be RMB0.46 and RMB0.54 respectively, with PT of HKD8.20, implies a FY2024E P/E of 16.3x (~2-yrs historical average + 1 standard deviation). Our investment rating is “Buy”.

Risk factors

1) Consumer demand recovery is slower than expected; 2) Slowdown in domestic sports apparel consumption expenditure; 3) Intensified competition in the industry; and 4) Slower-than-expected in new brands development.

Financial

Click Here for PDF format...