Investment Summary

Yue Yuen Industrial (Holdings) Limited ("Yue Yuen") remains a global leader in footwear manufacturing. For the nine months ended September 30, 2024, Yue Yuen reported a net profit attributable to owners of USD 331.7 million, representing a YoY growth of 140.9%. The robust performance of its footwear manufacturing business offset the challenges in its China retail operations, while effective cost control measures supported overall profitability growth.

Despite macroeconomic uncertainties, including fluctuations in consumer confidence and geopolitical risks, Yue Yuen has demonstrated strong operational resilience. With flexible capacity management, ongoing cost control efforts, and stable cash flow Based on the company's resilient business model and promising outlook. Our investment rating is “Buy”, with PT of HKD35.00.

Financial Performance Highlight

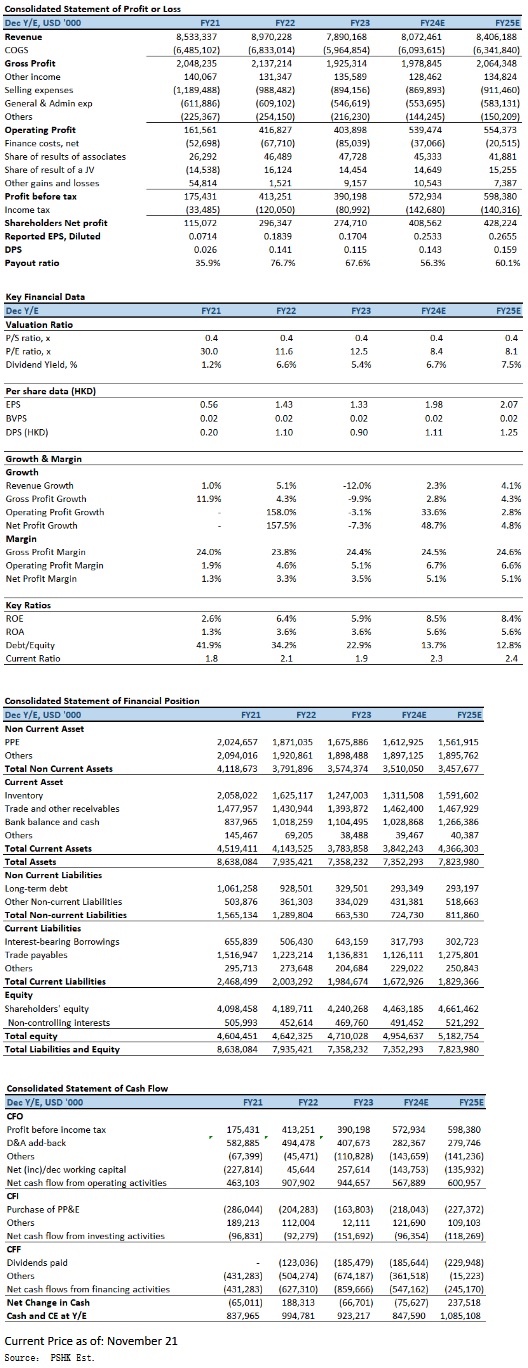

For the nine months ending September 2024, Yue Yuen reported revenue of USD 6,075.3 million, reflecting a YoY increase of 1.5%. Gross profit surged to USD 1,472.3 million, up by 4.5%, with the gross margin expanding to 24.2%, an improvement of 0.7 percentage points compared to the same period last year.

Revenue attributed to footwear manufacturing activity (including athletic/outdoor shoes, casual shoes and sports sandals) reached USD 3,782.7 million, marking an 8.2% YoY growth. Footwear shipments volume increased by 16.2% YoY to 18.69 million pairs, while the average selling price per pair declined by 6.8% to USD 20.24. The gross margin for the manufacturing business rose by 1.6 percentage points to 19.6%, primarily driven by strong order demand, enhanced capacity utilization, and significant improvements in production efficiency.

The athletic/outdoor footwear segment accounted for 85.9% of footwear manufacturing revenue, whereas casual shoes and sports sandals comprised 14.1%. Athletic/outdoor shoes remain the primary revenue contributors, representing 53.5% of total revenue, followed by casual shoes and sports sandals at 8.8% of total revenue.

Selling and distribution expenses decreased by 8.3% to USD 624.2 million, administrative expenses declined by 1.2% to USD 416.1 million, and other expenses fell by 32.2%. These cost-containment measures have bolstered overall profitability and significantly enhanced operational efficiency.

The company recorded non-recurring profit of USD 26.4 million, primarily stemming from a one-off gain of US$24.1 million on the partial disposal of associates. Excluding non-recurring items, recurring profit attributable to shareholders stood at USD 305.2 million, reflecting a substantial YoY increase of 127.8%.

Robust Footwear Demand

As the global footwear market continues to normalize, Yue Yuen Group is poised to sustain robust growth in order demand, driving further improvements in overall capacity utilization and production efficiency. Operationally, the third quarter of the year was uncharacteristically solid and not a low season for the Group's manufacturing business. Demand for its production capacity continued to outstrip supply, with footwear shipment volumes growing strongly and the decline in average selling price narrowing quarter-on-quarter.

Despite the mixed consumption landscape in mainland China, where retail operations have been impacted by diminished foot traffic across multiple locations, resulting in subdued sales momentum, Pou Sheng continuously improved sales conversion rates within its retail stores while optimizing store-level productivity and efficiency. At the same time, its omni-channel sales remained relatively resilient as it continued to push ahead with its digital transformation strategy and maintain a high degree of agility and flexibility in its decision-making processes.

Looking ahead, Yue Yuen Group remains committed to its mid-to-long-term capacity expansion strategy, targeting Indonesia and India to leverage labor supply and infrastructure developments that support sustainable growth. This strategic diversification of manufacturing capacity is expected to bolster the company's operational resilience. The company will continue to focus on enhancing manufacturing efficiency and sustaining solid profitability growth through stringent cost and expense management measures. Additionally, Yue Yuen International will persist in its dynamic expansion of both physical and omni-channel retail operations, further enhancing operational efficiency through inventory management and digital transformation initiatives.

Investment Thesis

We maintain a cautiously optimistic outlook on Yue Yuen's future growth prospects. The company's leading position in the global footwear manufacturing market, coupled with its robust financial performance and flexible capacity management capabilities, positions it well to remain competitive amid market volatility. We expect the company's earnings per share (EPS) to reach USD 0.25 in FY2024 and USD 0.27 in FY2025, with PT of HKD19.00, implies a FY2024E forecast P/E of 9.6x (aligning with ~5-yrs historical average). Our investment rating is “Accumulate”.

Risk factors

1) Adverse global economic conditions or waning consumer confidence could negatively impact demand within the footwear market; 2Increases in the costs of raw materials or labor may erode the company's gross margins; 3Potential disruptions to global supply chains resulting from geopolitical tensions could adversely affect operations; and 4) Continued subdued consumer spending in mainland China's retail sector may further dampen retail business performance.

Financial

Click Here for PDF format...