Sectors:

Air & Automobiles (Zhang Jing),

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

Utilities, Commodity, Shipping (Margaret Li)

TMT, Semiconductors (Megan Tao)

Automobile & Air (Zhang Jing)

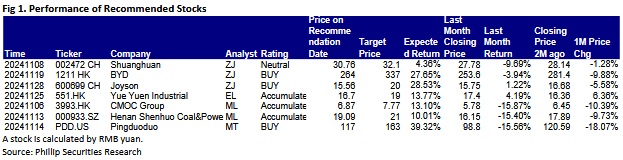

This month I released 1 initiation report of Shuanhuan Driveline (002472.CH), and updated reports of BYD (1211.HK) and Joyson Electronics (002472.CH).

Shuanghuan Driveline(002472.CH) is a pacesetter in the domestic automotive gear industry and robotic RV reducer industry. By leveraging its advantages in capacity, management, R&D and customer base, the Company has seized the opportunities for upgrading brought by gear outsourcing and high industry barriers as a result of the booming NEV industry.

The third quarter performance report for 2024 released by the Company shows that the revenue reached RMB 2.42 billion yuan (up 10.7% yoy), net profit attributable to shareholders arrive RMB 265 million yuan (up 20% yoy), and gross profit margin came to 23.96%,(up 2.26 ppts). The profitability continues to strengthen. In terms of gears for new energy vehicles, which enjoy high market attention, the Company reached a production capacity of five million units of transmission gear shafts for new energy vehicles at the end of 2023. The capacity utilization rate was high. Moreover, in 2023 the Company decided to establish a production base for gear transmission parts for new energy vehicles in Hungary. The construction will begin in 2024, and the Company will gradually release capacity based on existing orders and its production capacity in 2024 and 2025. In 2024H1, the Company recorded an overseas sales revenue of about RMB 0.62 billion, accounting for 14.3% (0.6ppts higher than 2023) of the total revenue, showing considerable room for improvement. As far as we are concerned, accelerated global capacity will lay cornerstone for the Company's global expansion.

Looking forward, Shuanhuan is expected to continuously benefit from the boom of new energy passenger vehicles, expansion of the industrial chains of automatic gearboxes of commercial vehicles, and rapid development of robotic reducers and gears for daily use. As for valuation, we expected diluted EPS of the Company to RMB1.22/1.53/1.89 of 2024/2025/2026. And we accordingly gave the target price to RMB32.1, respectively 26.3/21/17x P/E for 2024/2025/2026.

In May, BYD (1211.HK) launched its 5th-generation DM technology, featuring upgrades to the power architecture, thermal management system and electronic and electrical systems, allowing for a minimum charge-sustaining fuel consumption of 2.9L/100km and a total range of up to 2,100 km. Models equipped with this technology, including Qin L, Seal 06, Song L, Song PLUS, Han, Sealion 05, Song Pro and Tang DM-i Modified, have been launched successively since May, further driving up the competitiveness and pricing of the Company's products. From January to October 2024, the Company sold 3,250 thousand vehicles, up 36% yoy. Specifically, domestic sales reached 2,920 thousand vehicles, up 32.5% yoy, while overseas sales surged to 329 thousand vehicles, up 86.9 yoy. Overseas sales accounted for 10.2% of total sales, representing a yoy increase of 2.7 ppts. Sold high-end brand models totalled 144 thousand vehicles with yoy increase of 39%, accounting for 4.5% of total sales, representing a yoy increase of 0.1 ppts.

The upcoming launches of high-end models, such as Tengshi Z9 and Z9GT, Han L, Tang L, Fangchengbao 3, Fangchengbao 8 and Yangwang U7, and increase in overseas seals owing to the ramp-up of productivity abroad and positive expansion in Asian, African and Latin American markets (overseas sales are expected to surpass 450 thousand vehicles in 2024 and reach 800 thousand vehicles by 2025) will further contribute to the growth of Company's earnings..

For valuation, we revised the EPS forecast for 2024/2025 to 13.13/16.46 yuan, and introduce 2026E EPS to 19.31 yuan. Therefore, we given the target price of 337 HK$, corresponding to 2024/2025/2026 23.5/18.8/16x P/E.

Joyson Electronics (002472.CH) intensified efforts to increase its share in the Chinese market, focusing particularly on leading domestic self-owned brands and new forces of vehicle manufacturing. In the first three quarters of 2024, the Company gained new orders worldwide amounting to approximately RMB70.4 billion cumulatively, up 19.3% yoy. New orders for new energy models, amounting to approximately RMB37.6 billion, up 7.4% yoy, accounted for 53.4% of all new orders. From the business segment perspective, new orders in the automotive safety segment reached approximately RMB49.1 billion, a yoy increase of 44.4%, and new orders in the automotive electronics segment reached approximately RMB21.4 billion, a yoy decrease of 14.4%. From a regional perspective, the Company continued to strengthen its position in the Chinese market and its cooperation with self-owned brands and emerging vehicle manufacturers. New orders from China amounted to approximately RMB31 billion, up 24% yoy, accounting for around 44% of the Company's total orders from China, a yoy increase of 2 ppts. Notably, the proportion of orders from leading self-owned brands and emerging vehicle manufacturers saw consistent growth, demonstrated by the full coverage of top 10 new energy vehicle brands/manufacturers on the sales leaderboard in the automotive safety business segment.

The Company promptly seized the opportunities brought by the rapid development of intelligent electric vehicles, and deepened business layout and increased R&D input in intelligent electric vehicles, with enrichment of business categories. In the first three quarters, the Company explored emerging business, such as the UWB technology solution (consisting of the digital key and the in-cabin life detection radar), the ADAS L2 Smart Camera (front view all-in-one) solution and the vehicle-road-cloud integrated system, in the fields of intelligent driving, intelligent cockpit/network connection systems and body area intelligence. As the Company continues to increase R&D input and actively expands business categories, its competitiveness in emerging business is expected to enhance on an ongoing basis.

As a global leader in automotive safety and electronics, the Company has maintained sound development while actively capitalizing on the opportunities brought by rapid development in the intelligent electric vehicle sector. In this regard, its orders on hand will continue to grow, underscoring a promising outlook for its future growth.We expect Joyson's EPS for 2024/2025/2026 to be 0.94/1.11/1.5 yuan. We revised the target price of RMB 20 equivalent to 21.3/18/13.3x E P/E.

TMT, Semiconductors, Consumer, Healthcare (Eric Li)

This month I released reports of Yue Yuen Industrial (Holdings) Limited(551 HK).

For the nine months ending September 2024, Yue Yuen reported revenue of USD 6,075.3 million, reflecting a YoY increase of 1.5%. Gross profit surged to USD 1,472.3 million, up by 4.5%, with the gross margin expanding to 24.2%, an improvement of 0.7 percentage points compared to the same period last year.

Revenue attributed to footwear manufacturing activity (including athletic/outdoor shoes, casual shoes and sports sandals) reached USD 3,782.7 million, marking an 8.2% YoY growth. Footwear shipments volume increased by 16.2% YoY to 18.69 million pairs, while the average selling price per pair declined by 6.8% to USD 20.24. The gross margin for the manufacturing business rose by 1.6 percentage points to 19.6%, primarily driven by strong order demand, enhanced capacity utilization, and significant improvements in production efficiency.

The athletic/outdoor footwear segment accounted for 85.9% of footwear manufacturing revenue, whereas casual shoes and sports sandals comprised 14.1%. Athletic/outdoor shoes remain the primary revenue contributors, representing 53.5% of total revenue, followed by casual shoes and sports sandals at 8.8% of total revenue.

Selling and distribution expenses decreased by 8.3% to USD 624.2 million, administrative expenses declined by 1.2% to USD 416.1 million, and other expenses fell by 32.2%. These cost-containment measures have bolstered overall profitability and significantly enhanced operational efficiency.

The company recorded non-recurring profit of USD 26.4 million, primarily stemming from a one-off gain of US$24.1 million on the partial disposal of associates. Excluding non-recurring items, recurring profit attributable to shareholders stood at USD 305.2 million, reflecting a substantial YoY increase of 127.8%.

We maintain a cautiously optimistic outlook on Yue Yuen's future growth prospects. The company's leading position in the global footwear manufacturing market, coupled with its robust financial performance and flexible capacity management capabilities, positions it well to remain competitive amid market volatility.

Utilities, Commodity, Shipping (Margaret Li)

This month I released 2 initiation reports of CMOC Group Limited (3993.HK) & Henan Shenhuo Coal&Power Co.,Ltd. (000933.SZ).CMOC (3993.HK) engages in the non-ferrous metal industry, mainly the mining and processing business, which includes mining, beneficiation and smelting of base and rare metals, and mineral trading business. With its main business located over Asia, Africa, South America and Europe, the Company is a leading producer of copper, cobalt, molybdenum, tungsten and niobium in the world. It is also a leading producer of phosphate fertilizer in Brazil. In terms of trading business, the Company is one of the leading metal traders in the world. CMOC is one of the very few mining companies that has mastered a world-class metals trading platform.

The company's operating income in the third quarter of 2024 was 51.94 billion yuan (RMB, the same below), a yoy increase of 15.53%; the net profit attributable to shareholders of listed companies was 2.84 billion yuan, a yoy increase of 64.12%; EPS was 0.14 yuan. From January to September, operating income was 154.75 billion yuan, a yoy increase of 17.52%; net profit attributable to shareholders of listed companies was 8.27 billion yuan, a yoy increase of 238.62%; EPS was 0.39 yuan. The company's production and sales of copper and cobalt products had increased, the overall cost had decreased compared with the same period last year, and profits had increased yoy.

We predict that the company's revenue will be 204.8 billion yuan and 210.9 billion yuan respectively in 2024 and 2025, EPS will be 0.56/0.57 yuan per share, and the BVPS will be 2.84/2.75 yuan per share, P/B will be 2.21x/2.28x. The company has world-class mining resources. Congo (DRC) TFM is one of the world's largest copper and cobalt mines, KFM is the world's largest cobalt mine, Brazil's niobium mine is the world's second largest niobium mine, China's Sandaozhuang molybdenum and tungsten mine is one of the largest molybdenum mines in the world. The company's resources cover basic metals and special metals, which are closely related to the fields of energy transformation and industrial upgrading. At the same time, it is involved in agricultural applications through phosphorus. In the field of new energy metals, the company has important layouts in copper and cobalt, and is the world's leading new energy metal producer. It also has unique and scarce product portfolios such as molybdenum, tungsten, niobium, and phosphorus, all of which have leading industry positions. The cooperation agreement of the Nzilo II hydropower station in the Democratic Republic of the Congo (DRC) has been signed, and the power generation capacity of 200 MW will provide long-term and stable power guarantee for a new round of capacity leapfrogging. We believe that the company's in-depth development in the copper and cobalt industries will achieve more significant results in the future, giving the company a P/B of 2.5 times in 2024, a target price of HK$7.7, and an "Accumulate" rating.

Henan Shenhuo Coal&Power Co.,Ltd. (000933.SZ) is headquartered in Yongcheng, Henan Province, and its subsidiaries are mainly located in Henan, Xinjiang, Yunnan, Shanghai and other places. It is mainly engaged in coal mining and washing and processing, electric power production and distribution, alumina production and electrolytic aluminum smelting, aluminum sheets production, as well as the research and development and processing of new alloy materials and high-end energy storage materials. The annual production capacity of the main products is: 12 million tons of coal, 2000MW installed power generation capacity, 1.7 million tons of electrolytic aluminum, 1.2 million tons of alumina, processing for 420,000 tons of aluminum sheets and new material, with total annual output value of around 50 billion yuan (RMB, the same as below).

The company's Q3 revenue in 2024 was 10.09 billion yuan, with a yoy increase of 6.02% and a month-on-month increase of 0.96%; the net profit attributable to shareholders of listed companies was 1.25 billion yuan, with a yoy decrease of 8.00% and a month-on-month increase of 5.09%, which mainly due to the decline in coal price and increase in Alumina price; basic earnings per share was 0.56 yuan, with a yoy decrease of 8.39%; owners` equity attributable to shareholders of listed companies was 21.64 billion yuan.The company's mid-term profit distribution plan for 2024 is to distribute a cash dividend of 3.00 yuan (tax included) for every 10 shares, totaling 675 million yuan. No bonus shares will be issued, and no reserve fund will be converted into share capital. The plan aims to increase the frequency of dividends and investor returns.

In 2024, the company plans to produce 1.5 million tons of aluminum products, 6.9 million tons of raw coal, 535,000 tons of carbon products, 97,500 tons of aluminum foil, 165,000 tons of cold-rolled products, 50,000 tons of molded coke, and supply (sell) 11.97 billion kilowatt hours of electricity to achieve a balance between production and sales. In order to support the development of aluminum processing business, the company promoted the spin-off and listing of Henan Shenhuo Carbon New Materials Co., Ltd. We are optimistic about the growth of the company's aluminum and coal production, with the second phase of Shenhuo New Material's 60,000 tons annual battery foil project being put into production, the company's profit is expected to increase. We predict that the company's revenue will be 38.75 billion yuan and 40.692 billion yuan respectively in 2024 and 2025, earnings per share (EPS) are projected to be 2.16/2.52 yuan; and BVPS are projected to be 10.5 and 12.6, corresponding to a price-to-book ratio (P/B) of 1.8/1.5x. With a forecasted 2.0 times P/B in 2024 and a valuation of RMB 21, we recommend a "accumulate".

TMT, Semiconductors (Megan Tao)

In this month, I published a research report on Pingduoduo (PDD.US).

In the second quarter of 2024, the company achieved a total revenue of 97.1 billion yuan. Comparing to the same period last year, this represents an 85.7% increase. In terms of profitability, operating profit was 32.6 billion yuan, up by 156.0% year-on-year, and Non-GAAP net profit reached 34.4 billion yuan, a 125.5% increase year-on-year. Regarding segment revenues, online marketing revenue was 49.1 billion yuan, a 29.5% increase, primarily due to the improvement in the monetization rate of marketing products. Transaction service revenue was 47.9 billion yuan, showing a significant 234.2% increase driven by the growth in platform order volume and GMV. Management plans to waive 10 billion yuan in transaction fees over the next year, and it is anticipated that the growth rate of transaction service revenue will slow down. On the expense side, the company's total operating expenses for the quarter were 30.8 billion yuan, up by 47.5% year-on-year, mainly attributed to the increase in sales and marketing expenses. During the reporting period, sales and marketing expenses amounted to 26.0 billion yuan, a 48.5% increase year-on-year, primarily due to increased spending on promotional and advertising activities.

Considering the current macroeconomic environment in China, global geopolitical uncertainties, and the company's continued focus on high-quality development while providing significant transaction fee reductions, short-term profits may fluctuate. However, in the long term, this can help promote the formation of a positive platform ecosystem.We forecast the company's operating revenue for 2024 and 2025 to be 396.6 billion yuan and 504.1 billion yuan respectively, with Non-GAAP net profits of 96 billion yuan and 140.5 billion yuan, corresponding to EPS of 69 yuan and 101 yuan, and PEs of 17.2x and 14.8x.

According to the SOTP valuation method, the total target market value for Pinduoduo in 2024 is estimated at 225.8 billion USD, with a target price of 163 USD, corresponding to a Non-GAAP PE ratio of 17.2x for 2024 and a rating of "Buy." The segmented values are as follows:

Pinduoduo Main Platform: 124 USD, based on a Non-GAAP PE ratio of 13x for 2024, considering potential higher profit growth with a premium of around 30% compared to the current average valuation of comparable companies in the e-commerce industry.

Duo Duo Mai Cai: 6 USD, based on a Non-GAAP PE ratio of 15x for 2024, matching the valuation assigned to other companies with similar business models.

Temu: 12 USD, based on a Non-GAAP PE ratio of 15x for 2025, considering the support of its rapid revenue growth.Net Cash: 21 USD.

Click Here for PDF format...