Company Profile

Geely is one of the leading enterprises in China's self-brand passenger vehicles manufacturers. The Company's products include six major brands: Geely, Geometry, Lynk, Zeekr, Livan, and Galaxy, covering the A0 to C-class passenger vehicles market.

Investment Summary

New Models Showed a Significant Boost, with Sales Volume up 30% YoY and the Proportion of NEVs Rapidly Increasing

Geely reported a sales volume of 250 thousand units in November, up 27% yoy and 10.3% mom. The high yoy sales increase was mainly driven by new models such as Galaxy E5, Geely Xingyuan and ZEEKR 7X. On a closer look at brands, the high-end brand ZEEKR achieved a sales volume of 27 thousand units, up 106.1% yoy and down 13.1% mom. The mid-to-high-end brand LYNK&CO achieved a sales volume of 33 thousand units, up 8.7% yoy and 30.5% mom. The main brand Geely achieved a sales volume of 190 thousand units, up 23.8% yoy and 11.7% mom. Its sub-brand Galaxy achieved a sales volume of 75 thousand units, up 120.6% yoy and 18.5% mom. In terms of exports, 32.8 thousand units were exported in November, up 13% yoy.

In the first 11 months, the Company sold a total of 1,967 thousand units, up 30.9% yoy and extremely close to its annual target sales volume of 2 million units. The cumulative sales of Geely reached 1,512 thousand units, up 25.8% yoy (including that of the Galaxy series, which is 425 thousand units, up 73.5% yoy). That of ZEEKR reached 195 thousand units, up 85.3% yoy, and that of LYNK&CO reached 259 thousand units, up 33% yoy. In the first 11 months, 379 thousand units were exported, up 56% yoy.

In terms of new energy, the Company sold 122 thousand NEVs in November, up 93.9% yoy and 12.6% mom. NEVs accounted for 49% of the total sales volume, up 16.9 ppts yoy and 1 ppt mom. From January to November 2024, the cumulative sales of NEVs reached 777 thousand units, up 91.7% yoy, accounting for 39.5%, an increase of 12.5 ppts yoy. The Company's new energy transformation is accelerating.

Continuous Enhancement in Profitability in Q3

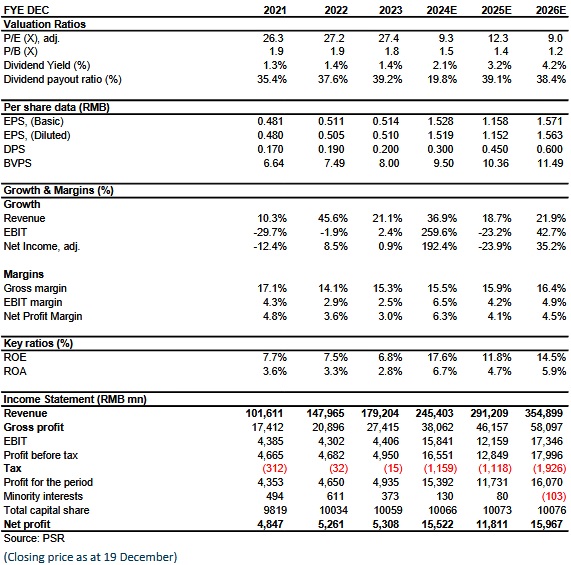

Thanks to its strong sales volume this year, Geely Auto has seen great growth in both revenue and profit. According to the Q3 report released by the Company, it reported a revenue of RMB60,378 million, up 20.5% yoy and 9.8% qoq, and a net profit attributable to the parent company of RMB2,455 million, up 92.4% yoy and down 72.8% qoq. The qoq decrease is mainly due to a one-time gain of approximately RMB RMB7.47 billion from the sale of the HORSE equity in the prior quarter. If this factor is excluded, up 56% qoq. Besides, if the one-time provision for LYNK&CO Europe in Q3 is excluded, the net profit attributable to the parent company excluding non-recurring items reaches RMB2.76 billion, up 116% yoy. In Q3, 534 thousand units were sold, representing a yoy increase of 18.7% and a qoq increase of 11.2%, respectively. Driven by the new models, the proportion of NEVs, especially high-end models, increased, boosting the ASP, which was up 4.1% yoy to RMB113 thousand.

A gross margin of 15.58% was recorded in Q3, up 0.14 ppts yoy and down 0.92 ppts qoq. The qoq decrease is mainly due to changes in accounting standards (the transfer of warranty deposits from expenses to costs). Particularly, the gross margin of ZEEKR vehicles was approximately 15.7% with a qoq increase of 1.5 ppts. ZEEKR achieved its first-ever quarterly turnaround from a loss to a profit( before any intercompany elimination), largely due to the scale effect coming into play. On the cost end, the sales and administration expense ratios were 4.47% and 5.82%, respectively, representing a yoy decrease of 1.73 ppts/0.54 ppts, indicating good cost control.

Shift towards Strengthening Strategic Integration to further Enhance Comprehensive Competitiveness

Changes in the auto industry are accelerating, and competition among NEVs is intensifying. To pursue long-term development, the Company issued the Taizhou Declaration in September 2024, clarifying strategic mergers and reorganisations as the development target for the next stage. In October, GEOME merged into Galaxy, and in November, LYNK&CO merged into ZEEKR. Upon completion, the Company will own 81% of LYNK&CO. LYNK&CO's results will be consolidated in the future. We believe that mergers and reorganisations can enhance strategic synergies and business integration across various sub-brands, eliminate horizontal competition, reduce duplicate investments, achieve complementary distribution networks, improve supply chain efficiency, and facilitate cost reduction and efficiency improvements. The brand positioning, technology planning, and product portfolio of the Company will be clearer. ZEEKR is positioned as a global luxury technology brand covering the high-end luxury market. LYNK&CO is positioned as a global mid-to-high-end brand in the new energy sector, covering the mid-to-high-end market. Geely Galaxy and China Star are positioned as mainstream brands, covering mainstream markets. Following the merger, ZEEKR and LYNK&CO plan to achieve a target sales volume of more than 1 million units by 2026. Two SUVs and two sedans of the Galaxy series will be launched next year, one per quarter. Distribution outlets will be expanded from the current 900 to 1,250 by the end of next year..

Investment Thesis

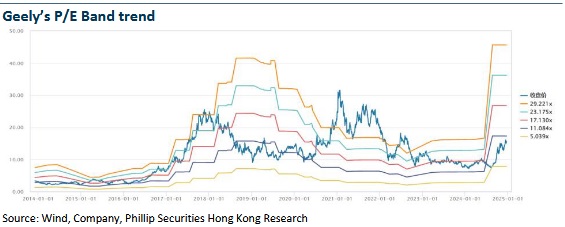

We revised our financial forecast and target price to HK$20.2, equivalent to 12.1/16/11.8x P/E ratio in2024/2025/2026, and we give the rating of Buy. (Closing price as at 19 December)

�Financials

Click Here for PDF format...