Company profile:

Zoomlion is a leading enterprise in the comprehensive engineering machinery industry, both domestically and globally, and is a frontrunner in the crane sector. Its main products cover 18 categories, 105 product series, and 636 model types. The company's traditional products primarily include cranes and concrete machinery, while emerging businesses mainly include excavators, high machines, agricultural machinery, mining machinery, and more. The company holds an industry-leading position in cranes, concrete machinery, and high machines, ranking third among global crane manufacturers and first among tower crane manufacturers.

Investment Summary

Stable Profitability

The Company released its 2024 annual report on March 24, 2025. The total revenue for the year was 45.478 billion (RMB, the same below), down 3.39% yoy. The net profit attributable to the parent company was RMB 3.52 billion, up 0.41% yoy, while the net profit after excluding non-recurring items was RMB 2.554 billion, down 2.7% yoy. If the company's share-based payment expense of RMB 866 million in 2024 (compared to RMB 279 million last year) is excluded, the net profit increased by 15.89%. Despite the decline in revenue, profitability remained stable, primarily due to the increase in gross profit margin (up 0.62 ppts) and cost control (sales expense ratio down 0.71 ppts). The gross profit margin rose to 28.17%, mainly driven by the decline in raw material prices and the increase in the proportion of high-margin overseas business.

Strong Growth in Overseas Business Compensates for Domestic Demand Shortfall

In 2024, the company's domestic revenue was RMB 22.098 billion (down 24.2% yoy), while its foreign revenue was RMB 23.38 billion (up 30.58% yoy). The decline in domestic revenue was mainly due to sluggish real estate investment (down 5.2% yoy in 2024), which dampened demand for construction machinery. At the same time, the overseas gross profit margin was 32.5%, significantly higher than the domestic gross profit margin of 24.06%, which strongly supported the stability of profits. The company continues to improve its “end-to-end, digital, localized” overseas business system, with its overseas layout continuing to expand. Additionally, by localizing production, the company reduces logistics and tariff costs. With 400 global sales outlets, the company provides “end-to-end” services, and its direct sales overseas account for more than 70%, with profit margins higher than those of the agency model. The company has established 11 overseas production bases in eight countries, including Italy, Germany, India, Mexico, Belarus, Brazil, Turkey, and the United States, forming a production system covering eight categories and 32 series. The company's overseas business continues to grow strongly, with significant results from its localized development strategy in key countries.

Dual-Engine Drive of Traditional and Emerging Businesses, Enhanced Anti-Cycle Capability

In 2024, the Company's main traditional segments, concrete machinery and crane machinery, generated revenues of RMB 8.01 billion and RMB 14.79 billion, respectively, with year-on-year declines of 6.8% and 23.35%, primarily due to the weakness in domestic real estate investment. In contrast, emerging segments such as earthmoving machinery, high-altitude machinery, and agricultural machinery generated revenues of RMB 6.67 billion, RMB 6.83 billion, and RMB 4.65 billion, respectively, with year-on-year growth of 0.34%, 19.74%, and 122.29%. In 2024, the company experienced a significant decline in crane machinery, while high machines and agricultural machinery saw rapid growth, leading to an increase in the proportion of emerging segments such as earthmoving, high machines, and agricultural machinery, which rose to 39.92%. Among these, agricultural machinery: the company ranked first in the dryer market share, second in wheat machinery, and saw new opportunities for growth in corn and rice machines. High-altitude machinery: the company has become a domestic leader, with significant technological advantages (the most complete range of domestic models).

Investment Thesis

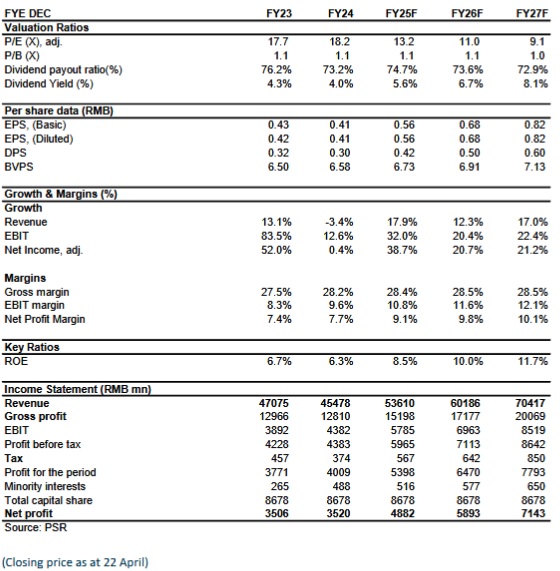

Zoomlion's 2024 performance reflects a pattern of "pressure on traditional segments, rise of emerging sectors," with overseas expansion and product mix optimization supporting earnings resilience. We believe the company's emerging businesses and international markets will continue to grow and expect EPS to be 0.56/0.68/0.82 yuan respectively for 2025/2026/2027. We offer a target price of 9 yuan, respectively 16/13.3/10.9x P/E for 2024/2025/2026, and an "BUY" rating. (Closing price as at 22 April)

Risk

Progress of new production line is below expectations

Downstream industries fall short of expectations

Sharply rising raw material prices or sharply falling product prices

Overseas market risk

Financials

Click Here for PDF format...