Financial performance

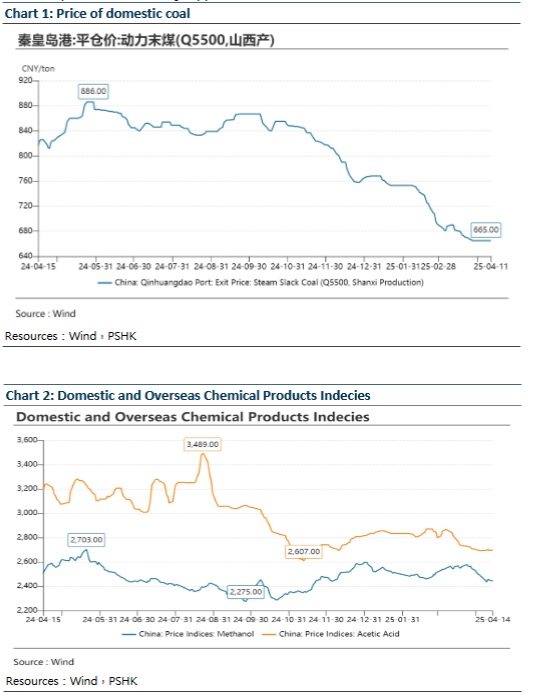

Due to the decline in coal price, the company's sales revenue in 2024 was 124.53 billion yuan (RMB, the same below) with a year-on-year decrease of 6.2%, of which the coal business revenue was 91.62 billion yuan with a year-on-year decrease of 10.2%, and the output of commercial coal reached 142 million tons with a year-on-year increase of 10.39 million tons. Among them, the output of Shaanxi-Inner Mongolia base increased by 6.66 million tons year-on-year, becoming the largest core growth pole which contributed the most. The output of Australian base increased by 3.43 million tons year-on-year, firmly ranking as Australia's largest dedicated coal producer; coal chemical business revenue was 25.22 billion yuan with a year-on-year decrease of 4.5%, and chemical product output reached 8.70 million tons with a year-on-year increase of 1.15 million tons; power generation business revenue was 2.54 billion yuan with a year-on-year decrease of 2.0%; other business revenue was 5.15 billion yuan with a year-on-year increase of 196.5%. Gross profit was 41.83 billion yuan with a year-on-year decrease of 17.3%. The net profit attributable to the parent company was 14.06 billion yuan with a year-on-year decrease of 26.9%. EPS was 1.42 yuan with a year-on-year decrease of 27.9%. The annual total dividend was 0.77 yuan per share, indicating that the company attached importance to shareholders` returns.

Good results in cost control, continued efforts to reduce costs and increase efficiency in 2025

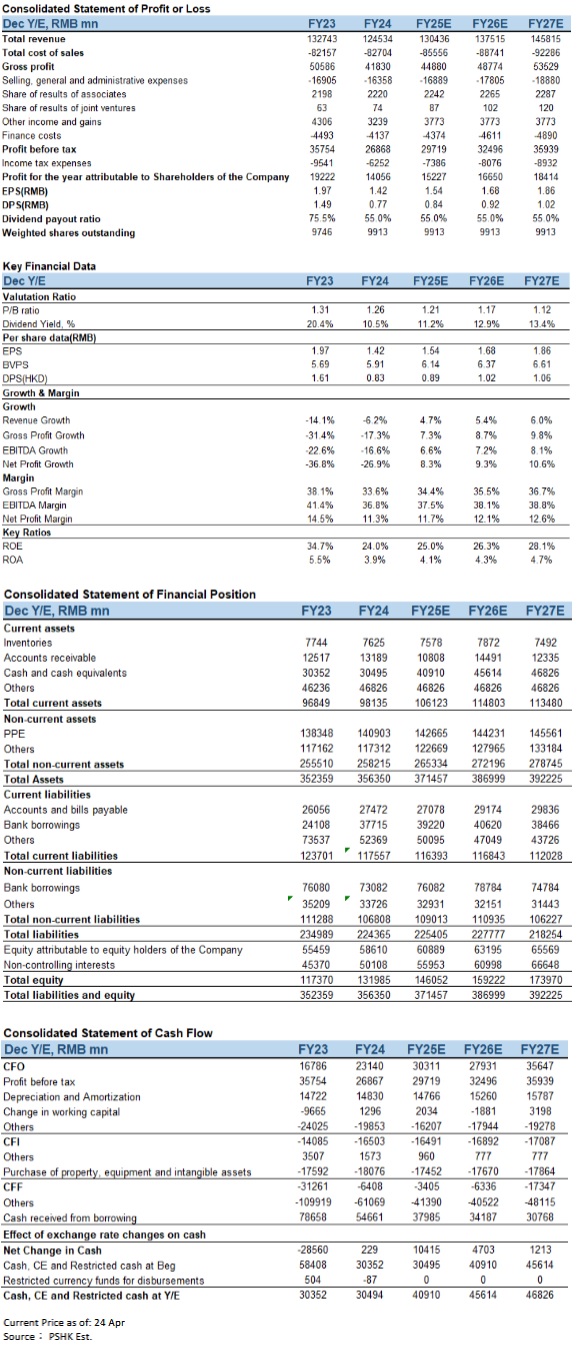

The company strictly controlled production costs and period expenses with remarkable results. In 2024, the sales cost of self-produced coal per ton was 345.4 yuan with a year-on-year decrease of 5.4%; the unit sales cost of methanol was 1,454 yuan/ton with a year-on-year decrease of 14.6%; the unit sales cost of acetic acid was 2,147 yuan/ton with a year-on-year decrease of 6.8%. The company actively optimized its debt structure, reduced financial expenses, and further reduced its debt-to-asset ratio. In 2024, the company's average financing rate was 2.98%, falling to the lowest level in history; it implemented H-share issuance and raised 4.5 billion yuan; effectively saved 830 million yuan in financial expenses; and reduced its debt-to-asset ratio to 63%. In 2025, the company will continue to promote the strategy of reducing costs and increasing efficiency and try to reduce the sales cost per ton of coal by 3%; the sales cost of methanol will decline by 60 yuan/ton; and the sales cost of acetic acid will not increase. The comprehensive financing cost will decline by 6%, financial expenses will decline by 300 million yuan, and the debt-to-asset ratio is expected to be below 60%.

Spending more than RMB 10 billion to acquire Xibei Mining, coal production capacity is expected to be released faster

Recently, the company issued an announcement that it plans to spend 14.07 billion yuan to acquire 51% equity of Xibei Mining, a subsidiary of its controlling shareholder(Shandong Energy Group Company Limited). Currently, Xibei Mining has 12 coal enterprises under its jurisdiction, holds 14 mining rights, has a total approved production capacity of 61.05 million tons/year and owns 10 production mines with an approved production capacity of 36.05 million tons/year. As of the end of November 2024, Xibei Mining assessed that the amount of resources utilized was 6.35 billion tons and the reserves were 3.65 billion tons, and the coal resource reserves were quite rich. This transaction will help increase Yankuang Energy's revenue and net profit, increase the company's coal resource reserves and the company's coal production capacity is expected to be released faster.

Company valuation

The company released guidance on its operating targets for 2025, with commercial coal production set to reach 155-160 million tons, trying to increase by more than 13 million tons year-on-year, chemical product production to reach 8.6-9 million tons, and CAPEX will be 19.5 billion yuan, with the main sources of money from self-owned funds, bank loans and bond issuance. The China Coal Industry Association released the Coal Industry Development Annual Report” which shows that this year's coal production and consumption are expected to maintain a growth trend, and coal imports will remain at a high level. In addition, the current level of coal reserves in society is relatively high. The supply and demand in the coal market throughout the year will be in a relatively balanced situation and then shift towards situation with more supply and less demand. Therefore, we believe that coal prices will continue to fluctuate downward in 2025, but there is certain support on the demand side, so the downward space is small and the company's coal business revenue is expected to improve. In terms of chemical business, the company expects that the growth rate of methanol and acetic acid industry production capacity will slow down in 2025, and the loose supply and demand pattern will continue. The prices of polyoxymethylene and caprolactam are expected to remain at a medium-to-high level. The price center of the company's chemical products is generally stable, and the price of high-end chemical products has strong support.

As a large-scale energy enterprise, Yankuang Energy has strong competitive advantages and growth potential in the industry. We raise our forecast for the company's revenue in 2025. We predict that the company's revenue will be 130.4 billion yuan, 137.5 billion yuan and 145.8 billion yuan respectively in 2025-2027. EPS will be 1.54/1.68/1.86 yuan. BVPS will be 6.14/6.37/6.61, corresponding to the P/B of 1.21x/1.17x/1.12x. The company's profit is expected to grow. The company is given a P/B of 1.3 times in 2025, with a target price of HK$8.48, and we maintain investment rating as " Accumulate ". (Current price as of Apr 24)

Risk factors

Energy policy impact, geopolitics, electricity demand, and production safety accidents.

Financial

Click Here for PDF format...