Investment Summary

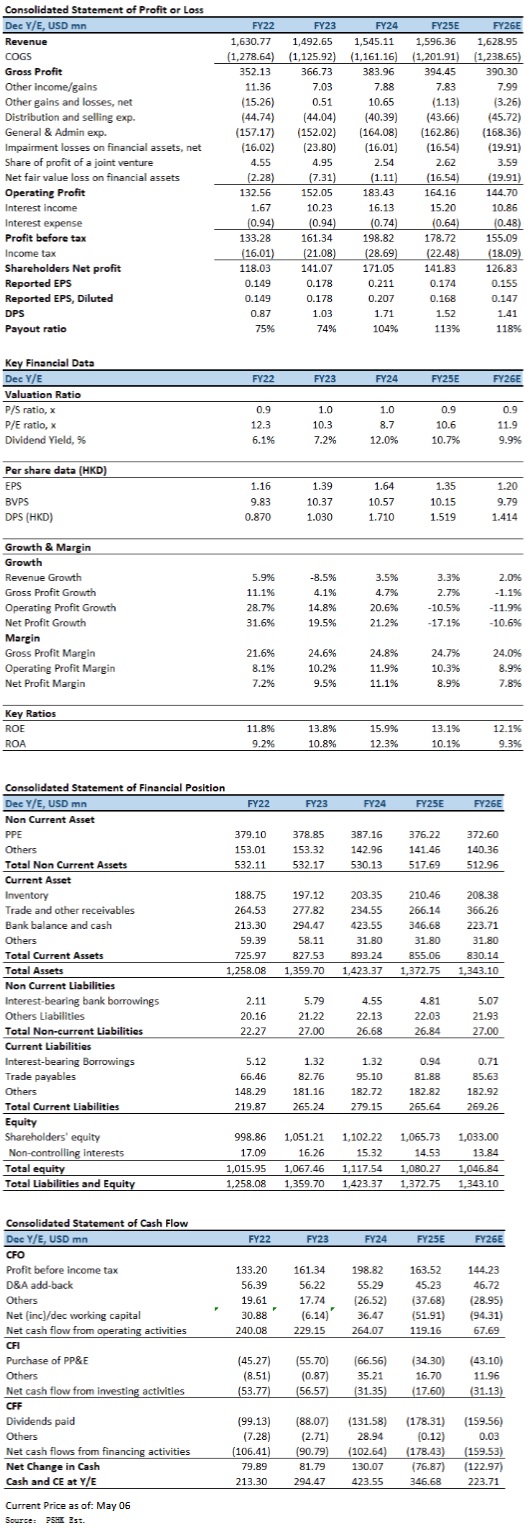

Stella International (1836 HK) reported FY2024 results that again exceeded market expectations, underscoring management's strong execution under its 2023–2025 Three-Year Strategic Plan. Total revenue rose 3.5% YoY to USD 1.545 billion, with shipment volume increasing by 8.2% to 53 million pairs, despite a 4.4% decrease in average selling price (ASP) to USD 28.4 due to product mix shifts and raw material cost normalization. Gross profit grew 4.7% to USD 384 million, with gross margin expanding to 24.9%. Operating profit rose 15.7% to USD 185 million, and the operating margin widened from 10.7% to 11.9%. Net profit reached USD 170 million, up 21.2% YoY, translating to a net margin of 11.0%. The company maintained prudent capital management, with net cash rising to USD 424 million. A final dividend of HKD 0.50 and a special dividend of HKD 0.56 were proposed, bringing the full-year distribution to HKD 1.71 per share, sustaining a ~70% payout ratio with additional shareholder returns on top.

Revenue and Shipment Analysis

In FY2024, revenue reached USD 1.545 billion, up 3.5% YoY. While the ASP declined due to a higher proportion of athletic footwear and lower input costs, the 8.2% increase in shipment volume to 53 million pairs offset pricing pressure. By region, North America recorded the strongest growth, with revenue up 7.7% YoY to USD 733 million, accounting for 47.4% of total revenue. Europe saw a modest decline of 2.8% to USD 362 million, while China remained stable at USD 260 million. Asia ex-China and other markets contributed USD 142 million and USD 49 million, respectively.

In 1QFY2025, unaudited group revenue declined slightly by 2.2% YoY to USD 331 million, largely due to a high base effect. Manufacturing shipment volume rose 3.4% to 12.1 million pairs, driven by robust demand for athletic footwear. ASP fell 5.0% YoY to USD 26.4 per pair, reflecting the increased mix of sports products. The continued growth in shipment volume despite ASP pressure highlights the resilience of underlying demand.

Gross profit for FY2024 rose 4.7% YoY to USD 384 million, with gross margin improving from 24.6% to 24.9%. The margin expansion was driven by a more favorable product mix, increased contribution from higher-margin sports and premium fashion footwear, better capacity utilization, and improved manufacturing efficiency. Despite a challenging macro environment, Stella maintained gross margin expansion, reflecting strong cost control and operational resilience.

Operating profit rose 15.7% to USD 185 million, with operating margin increasing 120bps to 11.9%, exceeding the company's 2025 target ahead of schedule. Net profit rose 21.2% to USD 170 million, and net margin improved to 11.0%. Adjusted net profit excluding a USD 11 million fair value loss related to its investment in Lanvin Group reached USD 171 million. Basic and diluted EPS came in at HKD 1.6490 (USD 0.2113) and HKD 1.6146 (USD 0.2069), respectively, both recording double-digit growth.

The manufacturing segment remained the core revenue contributor, generating USD 1.543 billion in revenue and USD 200 million in segment profit, up 13.9% YoY. The retail and wholesale segment, undergoing strategic downsizing, reported revenue of only USD 26 million and a segment loss of USD 9.5 million. The company has made clear its focus on the more profitable manufacturing business to enhance capital returns.

Operationally, the new factory in Surakarta, Indonesia further ramped up in 2024, contributing to improved plant efficiency. Meanwhile, the new factory in Bangladesh was completed by year-end, setting the stage for increased capacity to support future high-end orders.

As of end-2024, cash and cash equivalents increased to USD 424 million, up 43.8% YoY. Operating cash flow for the year reached USD 264 million, up 15.2% YoY, reflecting solid profit-to-cash conversion. Capital expenditure remained stable at USD 67 million, mainly allocated to capacity expansion in Indonesia and Bangladesh. Net investment outflow was USD 31.4 million, aligning with the capital deployment plan under the three-year strategy. Net cash improved significantly to USD 418 million, and net gearing dropped to -37.4%, underscoring a healthier capital structure.

Execution of 2023–2025 Three-Year Plan

By the end of 2024, Stella had essentially achieved the core financial targets set in its 2023–2025 plan. Operating margin surpassed the 10% target ahead of schedule, and net profit CAGR exceeded the original low-teens guidance. Capacity expansion is on track, and the client base continues to diversify, with several new boutique athletic and premium fashion brands added during the year. The company remains focused on enhancing ROIC through disciplined investment and operating efficiency.

In line with its shareholder return policy, the company proposed a final dividend of HKD 0.50 and a special dividend of HKD 0.56 per share, bringing the full-year payout to HKD 1.71, or approximately USD 113 million, maintaining a ~70% payout ratio. Under its capital return program announced in August 2024, Stella also reaffirmed its commitment to return up to an additional USD 60 million annually to shareholders during 2024–2026.

Investment Thesis and Valuation

Despite impressive execution, Stella faces mounting uncertainty amid macroeconomic headwinds and rising geopolitical risks. In particular, high U.S. tariffs and potential order volatility in premium fashion and sports segments pose challenges. While the company continues to focus on product quality, client mix optimization, and production efficiency to sustain a 10% operating margin and low double-digit net profit CAGR, delivering these targets may prove increasingly difficult.

To diversify revenue streams, Stella has begun expanding into the handbag and accessories segment, which could become a new growth engine over the medium term. The company's strong execution, prudent financial management, and clear long-term vision continue to underpin its leadership in the global premium footwear manufacturing space. However, given the external uncertainties, we forecast the company's earnings per share (EPS) for FY2025 and FY2026 to $0.174 and $0.155, respectively. We assign a target price of HKD 12.08, based on 9.0x FY2025E P/E, equivalent to +1 standard deviation above the past two-year average. Our investment rating is “Reduce”, reflecting a more cautious stance.

Risk factors

1) Weaker-than-expected end-consumer demand; 2) Inventory overhang at major sportswear clients; and 3) Escalating geopolitical tensions or trade restrictions.

Financial

Click Here for PDF format...