Company Profile:

Tuopu Group is an industry leader in the field of automotive NVH that is capable of synchronous design with the original equipment manufacturer. In recent years, on the basis of the original business of shock absorbers and interior functional parts, the Company has proactively arranged the module of the lightweight chassis system and the automotive electronics business as the future Ŗ+3" strategic development projects, in order to adapt to the trend of electrification, intellectualization and lightweight of vehicles.

Investment Summary

FY2024 Results Rose Nearly 40% Against the Market Trend; Short-Term Fluctuation Observed in Q1 2025

In 2024, Tuopu Group reported revenue of RMB26.60 billion (RMB, the same below), up 35.02% yoy; net profit attributable to the parent company was RMB3.001 billion, up 39.52% yoy; and net profit attributable to the parent company excluding non-recurring items was RMB2.73 billion, up 35.0% yoy. In Q4 alone, the Company recorded revenue of RMB7.248 billion, up 30.63% yoy, and net profit attributable to the parent company of RMB767 million, up 38.47% yoy. For the full year 2024, gross margin was 20.8% (down 2.2 ppts), and net profit margin was 11.3% (up 0.4 ppts yoy). Despite a decline in gross margin due to intensified competition among automakers, raw material price fluctuations, and capacity expansion, the Company's net profit margin improved against the trend, supported by strict cost control (period expense ratio dropped to 8.6%, down 0.9 ppts yoy) and increased government subsidies (RMB280 million, up RMB130 million yoy).

In Q1 2025, the Company recorded revenue of RMB5.77 billion, up 1.4% yoy, and net profit attributable to the parent company of RMB570 million, down 12.3% yoy. This was mainly due to increased expenses related to the development of new factories and businesses, as well as the impact of declining sales from downstream customers - Tesla and Seres saw their Q1 2025 sales drop by 13% and 47%, respectively.

Rapid Growth of New Energy Vehicles Drove Significant Result Growth, Automotive Electronics Experienced Explosive Growth

According to data from the China Association of Automobile Manufacturers, in 2024, China's automobile production and sales reached 31.282 million units and 31.436 million units, respectively, up 3.7% and 4.5% yoy. Among them, new energy vehicle production and sales were 12.888 million units and 12.866 million units, respectively, representing yoy increases of 34.4% and 35.5%, and accounting for 40.93% of China's total automobile sales. Benefiting from the rapid growth of new energy vehicles, the Company's interior, chassis, thermal management, and automotive electronics businesses in 2024 recorded yoy increases of 28.24%, 33.98%, 38.24%, and 907.63%, respectively, reaching segment revenues of RMB8.434 billion, RMB8.203 billion, RMB2.13 billion, and RMB1.82 billion. China's total automobile sales in 2025 are forecast to exceed 32 million units, with new energy vehicle sales expected to surpass 16 million units (including exports), continuing to maintain high growth. The production line adjustments of the Company's downstream customers are expected to conclude in Q2 2025, with limited impact anticipated for the full year.

Continued Increase in R&D Investment and Expansion of Product Lines

In 2024, the Company's R&D expenses reached RMB1.224 billion. Through continued investment in R&D, projects such as the air suspension system, smart cockpit, brake-by-wire (IBS), steer-by-wire (EPS), and electric drive systems have successively entered mass production, with the product portfolio continuing to expand. In the automotive chassis segment, the Company's independently developed forged aluminium ball joint control arm product contributed to the strong growth of the chassis business in 2024. In the automotive electronics segment, the Company became the first in China to achieve large-scale mass production and supply of closed-type electronic controlled air suspension systems (C-ECAS). Significant progress was also made in the intelligent braking system (IBS) segment, with multiple projects now in mass production.

Accelerated Capacity Expansion Domestically and Abroad, Rapid Advancement in Robotics Business

In 2025, the Company will continue to advance its capacity expansion plans. Domestically, it plans to complete the construction of Phase 9 and Phase 10 factories in the Qianwan New District. Overseas, planning has begun for Phase 2 of the Mexico project; the Phase 1 factory in Thailand, covering 185 mu, is scheduled to commence production in early 2026; and the Poland factory is being prepared for capacity expansion to further scale up production. Seizing the rapid development opportunities in the robotics industry, the Company established an independent electric drive division to focus on the robotics business. It began cooperation with customers on linear actuators and has since launched the development of rotary actuators and dexterous hand motors. Relevant products have been sampled to customers multiple times. The Company is also actively deploying products such as robotic body structural components, sensors, foot shock absorbers, and electronic flexible skin, aiming to establish a platform-based product layout for robotics. In 2025, the Company will launch a robotics industrial base project covering approximately 150 mu. Robot products are expected to undergo rapid iteration and enter mass production based on customer demand. The robotics business is set to create a new growth curve for the Company, laying a solid foundation for sustaining rapid development.

Investment Thesis

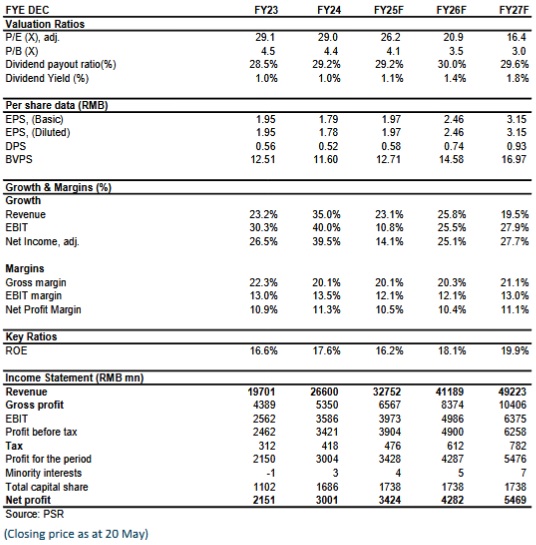

Tuopu Group is deeply integrated with new energy vehicle manufacturers through its Tier 0.5 collaboration model. On one hand, it continues to expand its product lines through sustained R&D investment; on the other hand, it benefits from the high-growth dividends of the new energy vehicle sector. Additionally, the Company is developing electric drive actuators and other products for the robotics segment—an emerging track with trillion-level future potential—offering vast development prospects. Overall, we believe the Company possesses sustainable growth capability. We expect the EPS for 2025/2026/2027 to be 1.97/2.46/3.15. So, we revise the Company's target price to RMB 59.1 yuan, respectively 30/24/19x P/E for 2025/2026/2027, a "Accumulate" rating. (Closing price as at 20 May)

Risk

Price war among peers

Raw material price increase

New business risk

Financials

Click Here for PDF format...