China Unicom (00762.HK) demonstrated robust financial performance and a continuously optimizing business structure in 2024. Its annual results not only slightly exceeded market expectations but also underscored the strategic effectiveness of the company's two core businesses: Connectivity and Communications (CC) and Computing and Digital Smart Applications (CDSA). Final dividend of RMB0.1562 per share (pre-tax), which, together with the interim dividend, brings the full-year dividend to RMB0.4043 per share (pre-tax). This represents a year-on-year increase of 20.1%, significantly higher than the earnings growth. The dividend payout ratio reached 60% in 2024, an increase of 5 percentage points yoy, clearly reflecting the company's strong commitment to shareholder returns and confidence in its future.

2024 Annual and 2025 First Quarter Performance Review

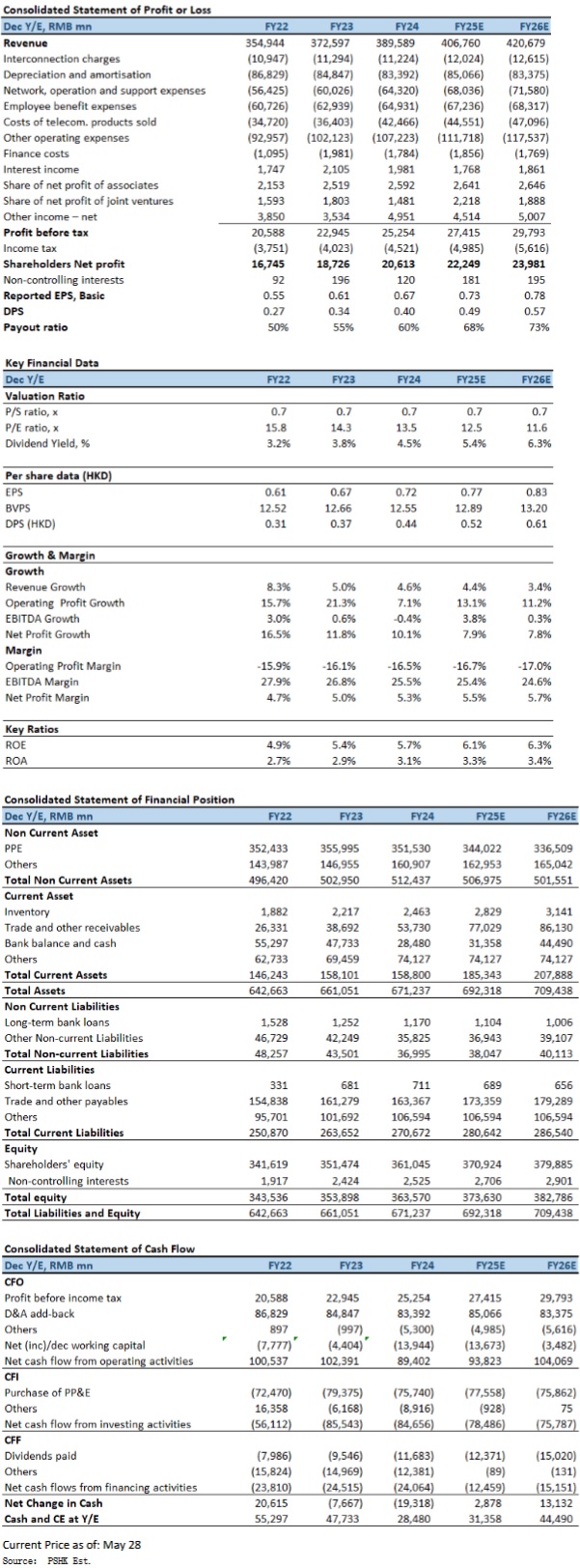

For the full year 2024, China Unicom's operating revenue reached RMB389.6 billion, a steady yoy increase of 4.6%, leading the industry in growth rate. Service revenue amounted to RMB345.98 billion, up 3.2% yoy, with a continuous optimization of the revenue mix. Profit attributable to equity shareholders of the Company reached RMB20.6 billion, a substantial 10.1% yoy increase, and return on equity (ROE) rose to 5.8%. The growth in these key financial indicators primarily stemmed from the company's effective implementation of cost control and operational efficiency enhancements. Notably, gross profit on sales of telecommunications products was RMB1.14 billion. Although accounts receivable increased from RMB38.69 billion in 2023 to RMB53.73 billion in 2024, an increase of 38.9%, the company emphasized that due to its large customer base, there is no significant concentration of credit risk regarding customer receivables.

Entering the first quarter of 2025, China Unicom maintained its steady growth trajectory. Operating revenue reached RMB103.35 billion, a yoy increase of 3.9%. Profit before income tax was RMB7.60 billion, and profit attributable to equity shareholders of the Company reached RMB5.93 billion, growing 5.6% yoy. First quarter service revenue was RMB90.88 billion, an increase of 2.1% compared to RMB89.04 billion in the first quarter of 2024. Sales of telecommunications products revenue also rose from RMB10.45 billion to RMB12.47 billion, an increase of 19.3%. These figures indicate that the company has maintained strong operational momentum into the new fiscal year.

Analyzing the performance of its business segments, China Unicom's two core businesses—Connectivity and Communications (CC) and Computing and Digital Smart Applications (CDSA)—both achieved steady growth and structural optimization. The CC business, serving as the company's "steady support", generated revenue of RMB261.33 billion in 2024, a 1.5% yoy increase, accounting for 76.0% of service revenue. The subscriber base reached a new record high, with mobile subscribers totaling 340 million, a net addition of 10.68 million; fixed-line broadband subscribers exceeded 120 million, with a net addition of 8.84 million, with both mobile and broadband subscriber bases reaching historical highs. The average monthly ARPU for integrated package subscribers remained above RMB100. The number of Internet of Things (IoT) connections surpassed 620 million, with a net addition of 130 million, and 5G IoT business scale led the industry. The number of Internet of Vehicles (IoV) connections reached 76 million, maintaining the leading position in the industry. Furthermore, the Gewu Industrial Internet platform managed over 12 million devices, accounting for one-eighth of the total number of devices nationwide. TV connectivity and information services also achieved innovative breakthroughs, with subscriber bases for key products such as Unicom UHD, Unicom Cloud Drive, and Unicom Housekeeper continuously expanding, leading to significant revenue growth. In the first quarter of 2025, the CC business continued its steady performance, with mobile subscribers reaching 349 million, a net addition of 4.78 million; fixed-line broadband subscribers at 124 million, a net addition of 1.92 million; and IoT connections reaching 663 million, a net addition of 38.4 million.

The CDSA business generated revenue of RMB82.49 billion in 2024, a substantial yoy increase of 9.6%, accounting for 24.0% of service revenue. Unicom Cloud revenue reached RMB68.6 billion, up 17.1% yoy. Data center revenue was RMB25.9 billion, a 7.4% yoy increase. Intelligent computing business showed strong growth, with newly signed contract value exceeding RMB26 billion last year. The company cumulatively implemented over 29,000 industrial Internet projects and established over 7,100 5G factories, achieving leadership in service capability and market position. In digital government services, intelligence services revenue reached RMB7.1 billion, up 26.5% yoy; data services revenue reached RMB6.4 billion, up 20.8% yoy, indicating the company's continued deep cultivation and breakthroughs in areas such as digital government and intelligent urban governance. International business also accelerated its growth, with revenue reaching RMB12.5 billion, a 15.2% yoy increase. It also expanded its branch network globally to enhance globalized operations, particularly in the IoV sector, serving the overseas expansion of leading Chinese automotive enterprises and facilitating the development of the intelligent connected new energy vehicle industry. In the first quarter of 2025, the CDSA business achieved a breakthrough in scale, with Unicom Cloud revenue reaching RMB19.72 billion. Data center revenue was RMB7.22 billion, a yoy increase of 8.8%. Intelligence services revenue reached RMB2.10 billion, up 14.0% yoy, and data services revenue was RMB1.84 billion, up 11.3% yoy. The company cumulatively implemented 30,000 řG+Industrial Internet" projects and established over 7,500 5G factories, further solidifying its leading position in industry applications.

Regarding operating costs, the total operating costs in 2024 amounted to RMB373.56 billion, a 4.5% yoy increase, with its percentage of operating revenue slightly decreasing to 95.9%. Depreciation and amortization charges were RMB83.39 billion, down 1.7% yoy, with its percentage of operating revenue decreasing from 22.8% to 21.4%. This primarily benefited from the company's precise investment, network "co-build co-share," and optimization efforts in recent years. However, due to factors such as the expanding scale of the network, network, operation, and support expenses increased by 7.2% to RMB64.32 billion, with its percentage of operating revenue increasing from 16.1% to 16.5%. Employee benefit expenses increased by 3.2% yoy to RMB64.93 billion, but its percentage of operating revenue slightly decreased to 16.7%, reflecting the company's efforts to optimize human resource efficiency. General and administrative expenses decreased by 7.4% yoy to RMB5.12 billion, while selling and marketing expenses increased by 3.2% yoy to RMB36.98 billion, with both their percentages of operating revenue decreasing, indicating the company's achievements in enhancing quality and efficiency and improving resource allocation efficiency. Other operating expenses increased by 7.2% to RMB65.13 billion, primarily due to the continuous growth of the CDSA business, leading to an increase in associated project costs. In the first quarter of 2025, depreciation and amortization expenses were RMB20.20 billion, a decrease of 4.6% compared to RMB21.18 billion in the first quarter of 2024, confirming the ongoing benefits of precise investment and network optimization.

Regarding capital expenditure, the company's capital expenditure in 2024 was RMB61.37 billion, a 17% yoy decrease, while computing power investment increased by 19% year-on-year. This reflects the company's precise investment strategy, optimizing its investment structure by allocating more resources to high-growth potential computing power areas to solidify the foundation for high-quality development. The company anticipates capital expenditure of RMB55.0 billion in 2025, with computing power investment expected to increase by 28% yoy. Special budget allocations have also been made for key AI infrastructure and major projects, further underscoring its strategic focus. In 2024, the company's net cash flow from operating activities was RMB89.40 billion, and free cash flow after deducting capital expenditure for the year was RMB28.03 billion. Although the company's current liabilities exceeded current assets by RMB111.9 billion, management emphasized that its continuous net cash inflows from operating activities, sufficient revolving banking facilities of RMB229.1 billion (of which RMB220.9 billion was unutilized as at 31 December 2024), and good credit history will ensure the company has ample funds to meet its working capital commitments, expected capital expenditure, and debt obligations.

Investment Thesis

China Unicom's robust performance in its Connectivity and Communications (CC) business provides a solid foundation. Its large subscriber base and stable ARPU ensure core revenue streams. More critically, the company's Computing and Digital Smart Applications (CDSA) segment demonstrates strong growth momentum and significant development potential. As the digital economy flourishes and AI technology is deeply integrated, the demand for computing power, data centers, and vertical industry solutions is expected to continue its upward trajectory. China Unicom, through a precise capital expenditure strategy, is gradually shifting its investment focus towards high-value, high-growth computing power infrastructure, while vigorously developing cloud services and intelligent applications. This effectively optimizes its business structure and enhances profitability. Furthermore, the company's consistently optimized dividend policy, with dividend growth outpacing profit growth, underscores its commitment to shareholder returns and confidence in future cash flows. We expect FY2025E-FY2026E EPS to be RMB 0.73 and RMB 0.78 respectively, with PT of HK$9.19, implies a FY2025E P/E of 11.9x (~3-months historical average plus 1 standard deviation). Our investment rating is “Neutral”.

Risk factors

1) Business growth may be lower than expected; 2) Macroeconomic downward pressure continues, and corporate customers` spending on digital transformation and ICT solutions may slow down; 3) Policy risks of the government pushing for more price cuts.

�Financial

Click Here for PDF format...