Company Profile

Spring Airlines (hereinafter referred to as the "Company") is the leader of low-cost airlines in China, founded in 2004 and based in Shanghai. It adopts a single aircraft model (i.e., the Airbus A320 family) and only offers the economy class. The Company raises its passenger load factor (P L/F) mainly by attracting travellers through its parent company, Shanghai Spring International Travel Service Ltd. (Shanghai Spring Tour), offering charter flights through its subsidiaries, and providing special fares. Meanwhile, it enhances the aircraft utilisation rate to obtain a remarkable cost advantage by optimising the route structure, prolonging flight time, and accelerating turnover.

Investment Summary

Pre-tax Profit Remains Robust

In 2024, Spring Airlines achieved operating revenue of RMB20 billion (RMB, the same below), up 11% yoy. Net profit attributable to the parent company reached RMB2.27 billion, up 0.7% yoy, while non-recurring net profit attributable to the parent company amounted to RMB2.25 billion, up 1.1% yoy. The Company distributed a cash dividend of RMB0.82 per share, with a payout ratio of approximately 35%.

In Q1 2025, the Company's operating revenue was RMB5.32 billion, up 2.9% yoy. Net profit attributable to the parent company was RMB680 million, down 16.4% yoy, while non-recurring net profit attributable to the parent company was RMB670 million, down 16.8% yoy. The decline in net profit was mainly due to the reduction of income tax expenses in the same period of previous years, as the tax shield was not utilised in 2024. However, the pre-tax profits for 2024 and Q1 2025 were RMB2.65 billion and RMB890 million, respectively, up 0.43% and 0.52% yoy, showing steady performance.

Solid Growth in Capacity and Strong International Route Performance

In 2024, the Company achieved a yoy growth of 18.8% in Revenue Passenger Kilometers (RPK), reaching 127% of 2019 levels. Domestic and international RPK grew by 9.8% and 95.4%, respectively, achieving 158% and 72.8% of 2019 levels. Available Seat Kilometers (ASK) grew by 16.1% yoy, reaching 126% of 2019 levels, with domestic and international ASK growing by 7.7% and 81.3%, respectively. The international route performance was particularly strong, with its share gradually recovering.

In Q1 2025, the Company's overall, domestic, and international RPK grew by 6.2%, -2.9%, and 61.6%, respectively. ASK grew by 6.9%, -3.3%, and 66.1%, respectively. The strong growth in international routes continued, while domestic routes were impacted by the repair of Leap-1A engines.

High Load Factor Maintained, but Yield Under Pressure

In 2024, the Company's average load factor was 91.5%, up 2.1 percentage points yoy. In Q1 2025, the load factor slightly declined by 0.6 percentage points to 90.6%, mainly due to the impact of a public opinion event in Thailand.

In 2024, the Company's revenue per available seat kilometer (RASK) decreased to RMB0.385, down 6.5% yoy, in line with the industry's downward trend. However, it remained above the industry average decline of 13%, and was up 6.4% compared to 2019. Domestic RASK was RMB0.373, down 6.35% yoy, while international RASK was RMB0.437, down 14.77% yoy, but grew by about 20% compared to 2019. In Q1 2025, the continued decline in industry ticket prices also led to a 3.14% yoy drop in Spring Airlines` RASK.

In 2024, the company's aircraft utilisation per day increased to 9.30 hours, up 9.41% yoy, partially offsetting the pressure from falling ticket prices. Additionally, the company's efforts in digital cost management began to show results, with unit ASK cost decreasing by 3.3% yoy, and unit ASK cost excluding fuel dropping by 1.7%. However, in Q1 2025, engine repairs limited aircraft utilisation, causing a 2.2% yoy increase in unit ASK cost excluding fuel. Despite this, the continued decline in oil prices benefited the company, reducing unit ASK cost by 2.3% yoy.

Fleet Expansion Continues

As of the end of 2024, the company's fleet consisted of 129 aircraft, with a net addition of 8 aircraft. It is expected that the fleet will reach 134, 146, and 160 aircraft in 2025, 2026, and 2027, respectively, with net additions of 5, 12, and 14 aircraft. In Q1 2025, the company's market share of capacity at Shanghai Pudong International Airport and Shanghai Hongqiao International Airport increased from 8.06% and 9.46% in the same period last year to 8.21% and 9.63%, respectively. We expect that the fleet expansion, continued recovery of international routes, higher aircraft utilisation, and cost improvements will contribute to sustained performance growth.In the long term, the low-cost airline business model is expected to continue penetrating the mass-market aviation travel sector. The company has a significant competitive advantage in both leisure and low-cost business travel segments. The company's growth momentum remains strong. However, due to factors such as ticket price declines and US-China tariffs, we are adjusting the company's EPS forecast.

Investment Thesis

Looking ahead, through the business model of low-cost aviation, the Company is expected to keep developing the mass aviation market and boasts its prominent competitiveness in sightseeing and low-cost business trips. There is still adequate momentum for future growth.

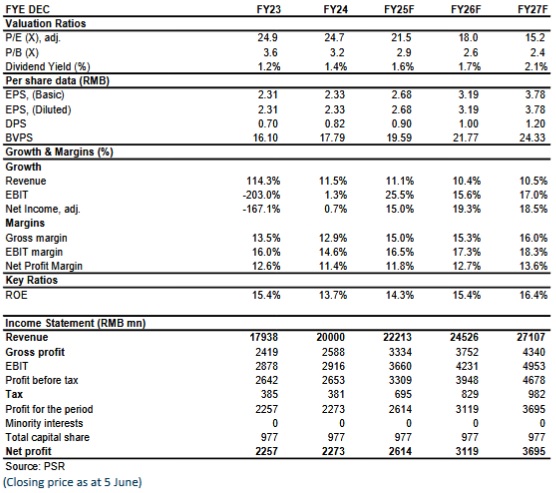

We revised the estimate for EPS for 2025/2026/2027 to be 2.68/3.19/3.78 yuan, respectively. We revised the Company's target price to RMB 65.5, respectively 24.5/20.5/17.3 x P/E, for 2025/2026/2027, a "Accumulate" rating. (Closing price as at 5 June)

Risk

Business cycle risk

Risk of jet fuel price fluctuation

Public health outbreak risk

Exchange rate fluctuation risk

Financials

Click Here for PDF format...