Financial performance

In the first quarter of 2025, the company recorded total revenue of RMB 180 billion, representing a 12.9% year-on-year increase. In terms of profitability, non-IFRS operating profit reached RMB 57.6 billion, up 9.5% year-on-year, with the operating profit margin slightly decreasing to 32.0% from 33.0% in the same period last year. Non-IFRS net profit for the period amounted to RMB 49.7 billion, increasing by 16.6% year-on-year. By segment, value-added services revenue in 1Q25 grew robustly by 17.1% year-on-year to RMB 92.1 billion, primarily driven by contributions from the domestic games business against a low base effect in the prior year. Online advertising revenue rose 20.2% year-on-year to RMB 31.9 billion, benefiting from increased user engagement, continuous AI-powered upgrades to the advertising platform, and enhancements to the Weixin transaction ecosystem. FinTech and Business Services revenue increased by 5.0% year-on-year to RMB 54.9 billion, mainly due to growth in consumer loan services and wealth management services, as well as increased revenue from cloud services and merchant service fees.

Performance Summary

Gaming Business

In the first quarter of 2025, the company's gaming revenue increased by 23.7% year-on-year to RMB 59.5 billion, accounting for 51.0% of total revenue—up from 49.0% in the same period last year. International gaming revenue reached RMB 16.6 billion, up 22.1% year-on-year, primarily driven by strong performance of titles including PUBG MOBILE and Brawl Stars. Domestic gaming revenue rose 24.3% year-on-year to RMB 42.9 billion, benefiting from last year's low base effect and record-high revenue from evergreen titles like Honor of Kings. Additionally, the new game Delta Action achieved a peak DAU count exceeding 12 million, making it the highest-DAU new game launched in the industry in the past three years. According to management, both domestic and international gaming businesses retain long-term growth potential. AI technology enhances gaming experiences and user engagement, which is expected to partially mitigate the low base effect.

Social Networks Business

In 1Q25, Social Networks revenue grew 6.9% year-on-year to RMB 32.6 billion, mainly fueled by robust advertiser demand for ad inventory across Video Accounts, Mini Programs, and Weixin Search. Tencent Video and Tencent Music maintained market leadership, with paid subscriptions reaching 117 million and 123 million, respectively.

Marketing Services Business

Marketing Services revenue in 1Q25 increased 20.4% year-on-year to RMB 31.9 billion, primarily driven by strong advertiser demand for ad inventory in Video Accounts, Mini Programs, and Weixin Search. Management highlighted advancements in generative AI capabilities and upgrades to the advertising technology platform, including improved image generation and video editing tools to accelerate ad production, the rollout of digital human solutions to boost livestreaming activities, and deeper insights into user interests and products to enhance recommendation accuracy. AI-driven optimizations are currently quantified through higher ad CTR. Historically, CTR averaged around 0.1% for banner ads and 1.0% for in-feed ads. With AI enhancements, CTR for certain ad inventory has risen to 3.0%.

By leveraging organic traffic growth and increased user engagement to drive advertising revenue growth without relying on higher ad load, the company can reserve the release of new ad inventory for the future, thereby extending the growth cycle. By controlling ad load to directly enhance product experience and boost user stickiness, this creates a virtuous cycle: improved experience leads to higher user retention, which in turn elevates advertising value.

FinTech and Business Services Business

In 1Q25, FinTech and Business Services revenue reached RMB 54.9 billion, up 5.0% year-on-year. Growth in FinTech services was driven by increased revenue from consumer loan services and wealth management services. Business services revenue growth benefited from higher cloud services revenue and merchant service fees. Tencent Cloud's audio-video solutions ranked first in China by revenue for the seventh consecutive year. By integrating large language model capabilities, the solutions further enhanced content generation, media processing, and real-time interactive experiences.

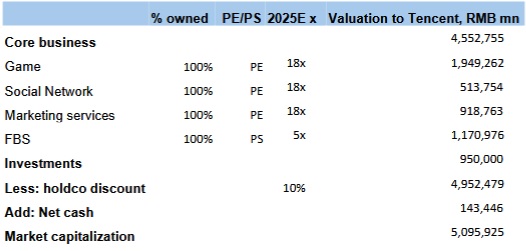

Company valuation

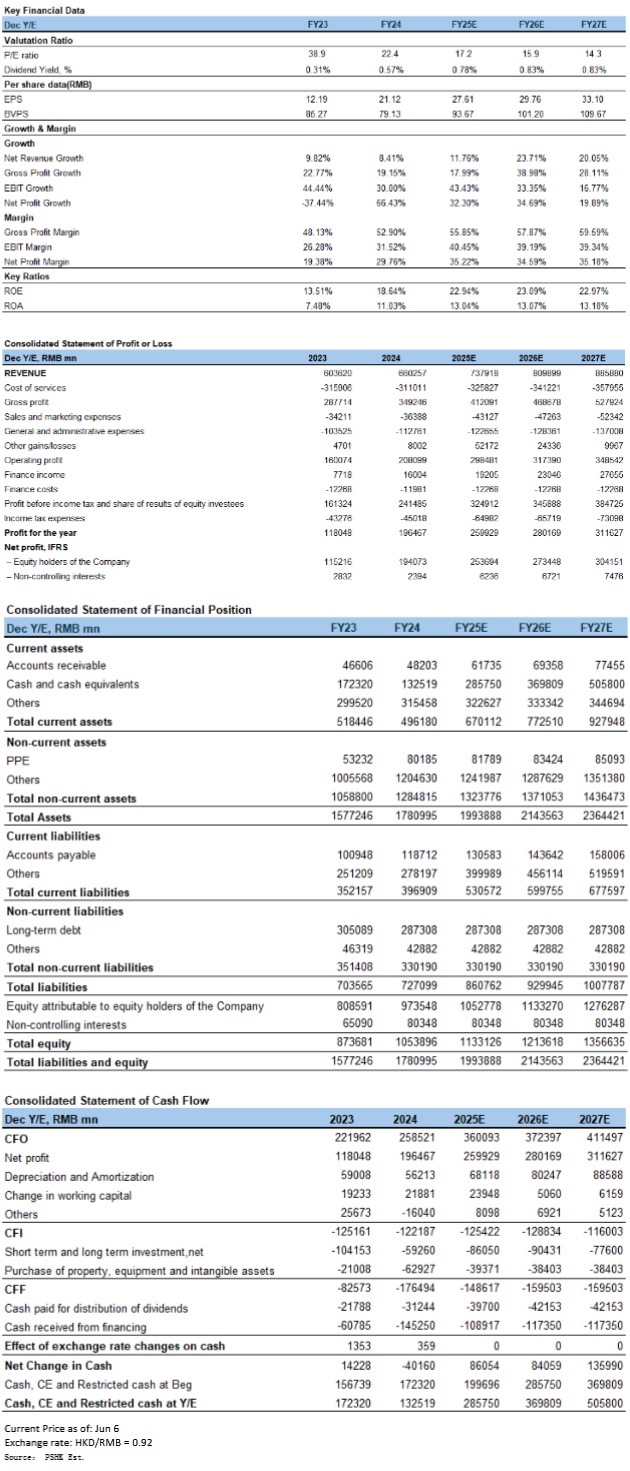

Overall, we remain optimistic about AI-driven medium-to-long-term growth. We raise our 2025-2027 revenue forecasts to RMB 737.9/809.9/885.9 billion and non-IFRS net profit estimates to RMB 295.0/315.3/346.7 billion, translating to EPS of RMB 28/30/33. The current share price implies a PE of 17/16/14x. Based on SOTP valuation—applying a 10% discount to the latest market values/valuations of subsidiaries and invested companies—we derive a 2025 target market cap of RMB 5.1 trillion for Tencent, equivalent to a target price of HKD 602. We upgrade our rating to "Accumulate".

Risk factors

1) Strict gaming regulations; 2) Weak macroeconomic environment; 3) Potential competitive threats from existing and emerging social platforms.

Financials

Click Here for PDF format...