Financial summary

In the first quarter of 2025, the company achieved total revenue of 111.3 billion yuan (RMB, same below), representing a 47.4% year-on-year increase; in terms of profitability, operating profit reached 13.1 billion yuan, up 256.4% year-on-year, while adjusted net profit hit 10.7 billion yuan, reaching a historic high with a 64.5% year-on-year growth. For segment revenue, 1Q25 smartphone × AIoT revenue amounted to 92.7 billion yuan, growing 22.8% year-on-year, primarily driven by increased smartphone shipments; innovative businesses including smart electric vehicles generated revenue of 18.6 billion yuan, with a gross margin of 23.2%.

Financial performance

Smartphone × AIoT

In the first quarter of 2025, smartphone revenue reached RMB 50.6 billion, up 8.9% year-on-year, primarily driven by increased shipments of higher ASP models, pushing the overall ASP to a historic high. According to Canalys data, global smartphone shipments reached 42 million units in Q1 2025, growing 3.0% year-on-year, ranking among the top three globally with a market share of 14.1% (up 0.3 percentage points year-on-year) for the 19th consecutive quarter. Regionally, the company reclaimed the top position in smartphone shipments in the Chinese mainland, with market share rising 4.7 percentage points year-on-year to 18.8%. In May 2025, the company launched its flagship Xiaomi 15S Pro, equipped with its first self-developed flagship processor, the Xuanjie O1.

In Q1 2025, IoT and lifestyle products revenue reached RMB 32.3 billion, surging 58.7% year-on-year, with gross margin hitting 25.2%, both setting new historical highs. This growth was primarily fueled by enhanced industrial capabilities, elevated brand influence, expanded retail channels, and government subsidies in the Chinese mainland. Meanwhile, the user ecosystem continued to expand. As of March 31, 2025, the number of connected IoT devices (excluding smartphones, tablets, and laptops) on the AIoT platform grew to 944 million, up 20.1% year-on-year.

Internet services revenue reached RMB 9.1 billion in Q1 2025, rising 12.8% year-on-year, mainly driven by increased advertising revenue, with gross margin reaching 76.9% (up 2.7 percentage points year-on-year). The internet user base continued to grow, with global monthly active users reaching 719 million in March 2025, a 9.2% year-on-year increase, setting another historic high.

Innovation Businesses (Smart Electric Vehicles, AI, etc.)

In Q1 2025, total revenue from innovation businesses including smart electric vehicles and AI reached RMB 18.6 billion, comprising smart electric vehicle revenue of RMB 18.1 billion and other related business revenue of RMB 500 million. The segment gross margin was 23.2%, with a segment operating loss of RMB 500 million. During Q1 2025, Xiaomi SU7 series deliveries reached 75,869 units.

Company valuation

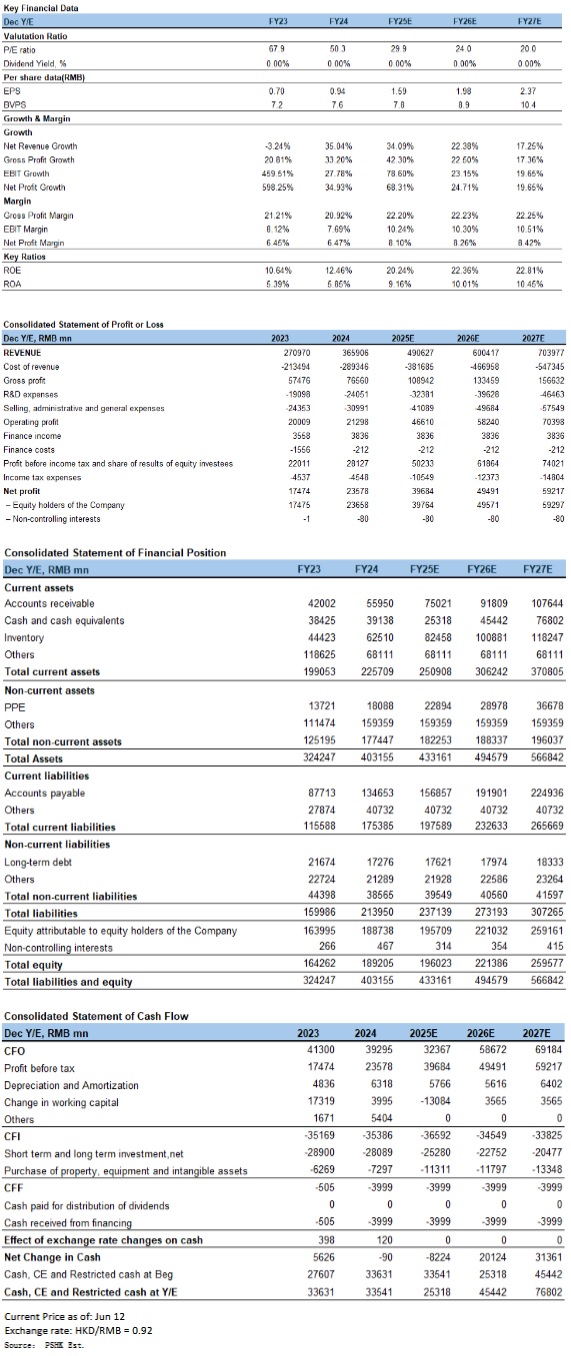

For non-automotive businesses, the smartphone market uptrend will continue into 2025, while China's stimulus policies are expected to drive consumption recovery. The company will benefit from its premiumization strategy, progressively upgrading product AI capabilities. For automotive business, the company's revenue is poised to maintain rapid growth alongside steady gross margin improvement. Overall, we remain positive about the company's medium-to-long-term growth prospects, valuing it at 35x 2025 PE with a target price of HK$60 per share. We forecast 2025-2027 revenue at RMB490.6/600.4/704.0 billion and net profit at RMB39.7/49.5/59.2 billion, translating to EPS of RMB1.59/1.98/2.37. Current share price implies 30/24/20x PE from 2025 to 2027. Consequently, we upgrade our rating to "Accumulate".

Risk factors

1) Demand for smartphones and other personal electronic products is below expectations; 2) Component costs are increasing; 3) Demand in the new energy vehicle market is lower than expected.

Financials

Click Here for PDF format...