Company profile:

Feilong Auto Components Co., Ltd. was established in 2001 and is a leading enterprise in the domestic automotive thermal management sector, maintaining strong growth momentum in both traditional and new energy tracks. In the field of traditional thermal management, the Company continues to consolidate its market advantage with three core products: mechanical water pumps, exhaust manifolds, and turbocharger housings (abbreviated as “turbo housings”). In the field of new energy system cooling, its main products include the electronic water pump series and thermostat valve series. Currently, the Company is implementing a dual-track penetration strategy of “automotive + general industrial”, developing a second growth curve in non-automotive sectors, focusing on intelligent liquid cooling solutions for 5G base stations, AI computing centres, new energy storage, hydrogen energy equipment, and high-end agricultural machinery, thereby enabling the cross-industry application of thermal management technology.

As of now, the Company has more than 200 major domestic and international customers (including over 130 customers in the new energy sector that are either supplied to or connected with), and serves over 300 global base factories. In the domestic market, the Company's supporting customers are mainly complete vehicle enterprises and OEMs, with key clients including Chery, Seres, Great Wall Motor, and Geely Auto. In the overseas market, key clients include BorgWarner, Cummins, and Daimler. Customers supplied to or contacted in the new energy thermal management components sector include GAC Aion, Li Auto, Leapmotor, NIO, Chery, Seres, Geely Auto, Xiaomi Auto, and XPeng.

Investment Summary

Stable Financial Performance

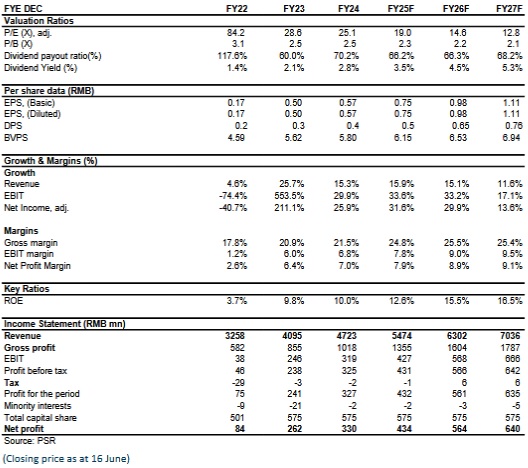

From 2007 to 2024, the Company achieved a compound growth rate of 13.7% in total operating revenue. In 2024, revenue reached RMB4723 million, up 15.34% yoy. By business segment, revenue from engine thermal management energy-saving and emission-reduction components grew by 19.4%, while revenue from new energy-related components increased by 40.44%, becoming the primary growth driver. Although revenue in the first quarter of 2025 declined by 10.55% yoy to RMB1.11 billion, net profit rose against the trend by 3.06% to RMB123 million. Gross margin improved by 4.84 ppts yoy to 25.33%, mainly due to optimised product mix and effective cost control.

Steady Growth in Traditional Core Business

Within the Company's traditional business, turbo housings benefited from increased penetration of hybrid models and export growth, maintaining steady development. In 2024, sales exceeded 5 million units, up 27.64% yoy, making it the Company's primary revenue source, accounting for over 45% of total revenue with a market share of 20%. The current casting capacity stands at 8 million units. In 2024, the Company's turbo housing was recognised as a “Single Champion Product in Manufacturing”. The mechanical water pump and exhaust manifold businesses remain relatively stable. The mechanical water pump, the Company's founding business, was recognised as a “Single Champion Product in Manufacturing” in 2020. The Company now holds a 25% market share in automotive water pumps, securing a leading market position.

New Energy Thermal Management Components Accelerating in Volume, Actively Expanding into Non-Automotive Sectors

n 2024, revenue from new energy and non-automotive sectors reached RMB526 million, up 40.44% yoy. The Company's flagship product is the electronic water pump, with power ratings ranging from 13W to 3500W and current production capacity of 5.6 million units. In 2024, the Company's market share exceeded 10%, ranking fourth in the market. Recently, the Company signed a supply agreement with BYD for 500 thousand sets of electronic oil pumps, marking recognition of its technical strength in the new energy thermal management sector by a leading automaker. This order is expected to contribute RMB160 million in sales revenue over its lifecycle. Although it will not impact 2025 results, it will significantly boost revenue in subsequent years. In terms of non-automotive business, the Company's operations mainly involve charging stations, server liquid cooling, 5G base stations, and energy storage. Currently, the annual capacity for civilian electronic pump series products stands at 1.2 million units. The Company is primarily entering the market through IDC liquid cooling and has made substantial progress, having established supply or cooperation relationships with over 30 clients including HP, Shenling Environment, and Envicool.

Capacity Expansion, Overseas Factory Nearing Production

The Company is showing strong momentum in capacity expansion within the new energy thermal management field. The commencement of phase II projects at its Zhengzhou and Wuhu plants has enabled large-scale production of thermal management integrated modules, which entered mass delivery in January 2025. The Company expects annual production capacity for new energy thermal management components to reach up to 8 million units, covering electronic water pumps and thermostat valve series, sufficient to support approximately 1.2 million new energy vehicles. Currently, its Thai subsidiary, Longtai Auto Parts (Thailand) Co., Ltd., is under orderly construction, with a total investment of approximately RMB500 million. Trial production is scheduled to begin by the end of June 2025, with full-scale production expected by year-end. Once fully operational, it is projected to achieve annual production capacities of 1.5 million turbo housings, 1 million exhaust manifolds, 500 thousand mechanical water pumps, and 1 million electronic water pumps. Upon reaching full capacity, the plant is expected to generate up to RMB1.5 billion in incremental revenue.

Investment Thesis

With the rising penetration of new energy vehicles and increasing demand for liquid-cooled servers, the Company's dual-track strategy of “automotive + general industrial” is expected to continue unlocking result potential. We remain optimistic about the Company's development prospects.

As for valuation, we expected diluted EPS of the Company to RMB 0.75/0.98/1.11 of 2025/2026/2027. And we accordingly gave the target price to RMB16.6, respectively 22/17/15x P/E for 2025/2026/2027. "Accumulate" rating. (Closing price as at 16 June)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

Click Here for PDF format...