|

YUM CHINA(9987)

Analysis:

Yum China delivered robust performance in the first quarter of this year despite a market environment filled with uncertainties, demonstrating its business resilience and the effectiveness of its dual-driven strategy focused on efficiency and innovation. KFC's coffee brand, K-Yum Coffee, reached a milestone of 1,000 stores, leveraging a breakthrough business model that utilizes KFC's store space, resources, and membership system to attract more customer traffic. For Pizza Hut, building on the success of converting older stores to the WOW format, the group opened new WOW stores in lower-tier cities, with capital expenditure as low as half that of standard Pizza Hut stores.In the first quarter, total revenue grew 1% year-on-year to $3 billion, with system sales increasing by 2%, primarily driven by a 4% contribution from net new store openings. The group added a net total of 247 new stores, including 62 franchise stores, accounting for 25% of the additions. As of March 31, 2025, the total store count reached 16,642, with KFC operating 11,943 stores and Pizza Hut 3,769 stores. Delivery sales grew 13%, maintaining double-digit annual growth for the past 11 years, contributing approximately 42% of KFC and Pizza Hut restaurant revenue. Digital order revenue reached $2.6 billion, accounting for about 93% of the group's restaurant revenue.First-quarter same-store transaction volume rose 6% year-on-year, marking nine consecutive quarters of growth. Same-store sales reached 100% of the previous year's level for the first time since Q1 2024. Operating profit was $399 million, up 7%, with core operating profit increasing 8%. The operating profit margin improved to 13.4%, up 80 basis points, driven by higher restaurant margins and reduced administrative expenses. The restaurant margin was 18.6%, up 100 basis points, mainly due to lower costs for food, packaging, property rent, and other operating expenses. Diluted earnings per share rose 8% to $0.77, a new first-quarter high. The group returned $262 million to shareholders in Q1, including $172 million in share repurchases and $90 million in cash dividends.Yum China is actively exploring innovative technologies such as robotics and generative AI to enhance operational efficiency. Amid the current dynamic market environment, the group remains steadfast in pursuing its full-year 2025 targets, including a net addition of 1,600–1,800 stores, while continuing to create long-term, sustainable value for shareholders. (I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $366.00, Target Price: $398.00, Cut Loss Price: $350

|

ANJOYFOOD(603345.SH)

Analysis:

The company is a leading player in the frozen food industry in China, with its main products including frozen prepared foods, frozen noodle and rice products, and frozen dish products. Its sales models include distribution, supermarket, special direct sales, e-commerce, and new retail. In recent years, the company has expanded from frozen hot pot ingredients and frozen rice noodles to pre packaged food business, mainly through self-produced, OEM, and external mergers and acquisitions, with the goal of "creating a new Anjing" for pre packaged food. In 2024, due to increased promotion, the company achieved a total operating revenue of 15.127 billion yuan (+7.70% year-on-year) and a net profit attributable to the parent company of 1.485 billion yuan (+0.46%). In 2025, the company will launch new products including: 1) live fish freshly killed tender fish balls, 2) 6 creative packaging options, 3) C-end products for grilled sausages, and 4) Lock Fresh 6.0 series. The company recently acquired Dingwei Taiche to enter the Western style baking market, further enriching its product matrix.

Strategy:

Buy-in Price: RMB75.70, Target Price: RMB90.10, Cut Loss Price: RMB68.00

|

|

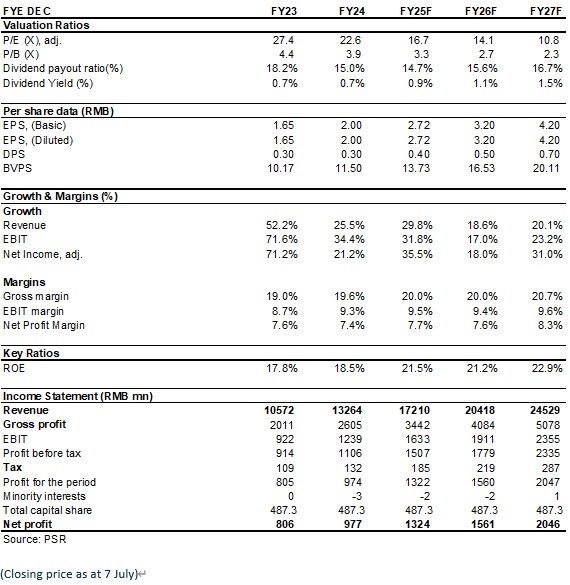

Xinquan(603179.CH) - Accelerating globalization

Company ProfileXinquan Co., Ltd., founded in 2001, offers a full range of interior and exterior trim assembly products for both commercial vehicles and passenger vehicles. With industry-leading process competence, cost control capability and technical strength, the Company is capable of simultaneous development with OEMs. In 2024, the Company reported revenue of RMB13,264 million (RMB, the same below), up 25.5% yoy; and net profit attributable to the parent company of RMB977 million, up 21.2% yoy. In Q1 2025, the Company reported total revenue of RMB3.52 billion, up 15.5% yoy; and net profit attributable to the parent company of RMB210 million, up 4.4% yoy. Investment SummaryStable growth in results

In 2024, the Company reported revenue of RMB13,264 million, up 25.5% yoy, mainly driven by the ramp-up from key downstream customers. Net profit attributable to the parent company was RMB977 million, up 21.24% yoy. Sales to the top five customers amounted to RMB9,889 million, up 38.16% yoy. In Q1 2025, the Company recorded revenue of RMB3,519 million, up 15.5% yoy. Among key downstream customers, the global production volumes of Chery, Geely, Li Auto and Tesla in Q1 2025 increased by 17%, 48%, and 16%, and decreased by 13% yoy, respectively. Net profit attributable to the parent company was RMB213 million, up 4.4% yoy. The gross margin was 19.5%, up 2.0 ppts yoy, showing stable performance, while the net profit margin fluctuated in the short term mainly due to: 1) Overseas business being in the capacity ramp-up phase, resulting in a mismatch between personnel expenses and per capita output; 2) An increase in employee welfare expenses during the period. Continuous expansion of product portfolio and enhancement of per-vehicle value

While focusing on interior and exterior trim products such as automotive instrument panel assemblies and bumper assemblies, the Company is actively developing its automotive seat business, continuously enriching and expanding its product portfolio to meet existing customers’ demand for integrated interior and exterior system solutions. In 2024, the interior business achieved steady growth, with revenue from instrument panel assemblies, door panel assemblies, and interior accessories reaching RMB8,348 million, RMB2,167 million, and RMB416 million, up 19.6%, 23.9%, and 12.4% yoy, respectively. The exterior business saw rapid volume growth, with bumper assemblies and exterior accessories generating revenue of RMB474 million and RMB229 million, up 415.0% and 29.0% yoy, respectively. The Company is currently accelerating capacity deployment for its seat business, with planned seat back panel capacities of 400 thousand sets in Mexico and 500 thousand sets in Slovakia. Additionally, the Company recently acquired a 70% equity interest in Anhui Ruiqi to accelerate seat business expansion with Chery Automobile. The new business is expected to further enhance the per-vehicle value contribution and lay a solid foundation for the Company’s long-term development. Accelerated globalization with strong contribution from the North American market

The Company has invested in and established production bases in Malaysia, Mexico, and Slovakia, and set up subsidiaries in the United States and Germany to cultivate the Southeast Asian, North American, and European markets, thereby promoting global expansion. In 2024, the overseas markets made rapid progress, with revenue in Southeast Asia, North America, and Europe all achieving high yoy growth. Among them, the North American market was the standout performer, with revenue reaching RMB700 million, up 89.14% yoy, and a gross margin of 26.37%, up 2.1 ppts yoy. This was mainly driven by the Company’s channel expansion and acquisition of new customers in North America, including a significant increase in orders from internationally renowned electric vehicle brands. Looking ahead to 2025, the production base in Slovakia is expected to commence operations, which will further expand the Company’s channels and customer base in the European market. Investment ThesisXinquan is a promising domestic automotive interior and exterior decoration enterprise. With the continuous expansion of the clients base and production capacity, it is expected to maintain sustained growth. We are optimistic about the long-term development of the Company and expect EPS to be 2.72/3.20/4.20 yuan respectively for 2025/2026/2027, a yoy increase of 35.5%/18.0%/31.0%. We offer a target price of 54.37 yuan, respectively 20/17/12.9 P/E for 2025/2026/2027, and an "Buy" rating. (Closing price as at 7 July)

Risk Factors1) Progress of new production line is below expectations

2) Electric vehicle sales fall short of expectations

3) Macroeconomic downturn affects product demand

4) Sharply rising raw material prices or sharply falling product prices Financial Data

Download PDF version... For more information on related options strategies, please click here.

| Recommendation on 10-7-2025 | | Recommendation | BUY (Upgrade) | | Price on Recommendation Date | $ 45.270 | | Suggested purchase price | N/A | | Target Price | $ 54.370 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|