|

CRYSTAL INTL(2232)

Analysis:

Crystal International primarily engages in the development and manufacturing of apparel products, including casual wear, denim, intimate apparel, sweaters, sportswear, and outerwear. The group has strengthened partnerships with leading clients and sportswear brands by increasing market share in existing product lines and successfully developing new categories, driving stable revenue growth. Additionally, Crystal has secured certifications for various upstream fabrics from brand clients, leveraging vertical integration to meet broader production needs and solidify long-term client relationships.For the year ending December 31, 2024, the group achieved revenue of US$2.47 billion, up 13% from 2023, and a net profit of US$201 million, up 22%. This was driven by continued investment in automation and effective management addressing initial inefficiencies from onboarding numerous new employees, optimizing production efficiency and boosting the gross margin by 0.5 percentage points to 19.7%. The net profit margin rose to 8.1%, up 0.6 points from 2023. Total dividends for 2024 were HK$0.383 per share (including a special dividend of HK$0.055 to mark the group's 55th anniversary), a 113% increase from 2023. Excluding the special dividend, the current dividend yield is 6%. The group indicated that, based on projected cash flows, there is room for further dividend increases.By the end of 2024, most core brand clients had optimized inventory levels, eliminating the need for further destocking. Rising consumer demand for trendy and innovative products prompted additional orders from brand clients, further boosting apparel production demand. Looking to 2025, Crystal will focus on sportswear, casual wear, and intimate apparel, deepening ties with key clients. Mid-2024 capacity expansion added 10,000 employees, bringing the total to 75,000, ensuring sufficient capacity for growing orders. The group's key production facilities in Vietnam, including a new self-built fabric plant in northern Vietnam that began construction in late 2024, will benefit from the recent U.S.-Vietnam tariff agreement (20% tariffs on Vietnamese exports to the U.S.). (I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $5.35, Target Price: $5.85, Cut Loss Price: $5.10

|

PRINX CHENGSHAN(1809)

Analysis:

The Company is one of the leading tire manufacturers in China, mainly producing all steel radial tires (all steel tires), semi steel radial tires (half steel tires), and diagonal tires (diagonal tires). It has four major brands, namely Prinx, Chengshan, Auston, and Fortune. The Company has two major production bases in China and Thailand, and three sales centers in China, North America, and Europe, forming a global development layout. In 2024H1, the Company`s revenue reach RMB 10.97 billion (a yoy increase of 9.9%), and its net profit reached RMB 1.312 billion (a yoy increase of 27%). In 2025, the company plans to establish a second overseas tire production base in Malaysia, with a production capacity of 6 million semi steel tires per year and 600000 all steel tires per year, further promoting its global layout.

Strategy:

Buy-in Price: $7.39, Target Price: $8.27, Cut Loss Price: $6.90

|

|

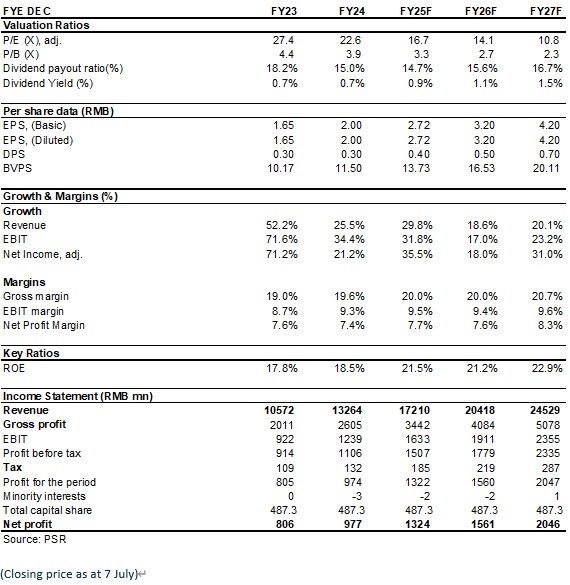

Xinquan(603179.CH) - Accelerating globalization

Company ProfileXinquan Co., Ltd., founded in 2001, offers a full range of interior and exterior trim assembly products for both commercial vehicles and passenger vehicles. With industry-leading process competence, cost control capability and technical strength, the Company is capable of simultaneous development with OEMs. In 2024, the Company reported revenue of RMB13,264 million (RMB, the same below), up 25.5% yoy; and net profit attributable to the parent company of RMB977 million, up 21.2% yoy. In Q1 2025, the Company reported total revenue of RMB3.52 billion, up 15.5% yoy; and net profit attributable to the parent company of RMB210 million, up 4.4% yoy. Investment SummaryStable growth in results

In 2024, the Company reported revenue of RMB13,264 million, up 25.5% yoy, mainly driven by the ramp-up from key downstream customers. Net profit attributable to the parent company was RMB977 million, up 21.24% yoy. Sales to the top five customers amounted to RMB9,889 million, up 38.16% yoy. In Q1 2025, the Company recorded revenue of RMB3,519 million, up 15.5% yoy. Among key downstream customers, the global production volumes of Chery, Geely, Li Auto and Tesla in Q1 2025 increased by 17%, 48%, and 16%, and decreased by 13% yoy, respectively. Net profit attributable to the parent company was RMB213 million, up 4.4% yoy. The gross margin was 19.5%, up 2.0 ppts yoy, showing stable performance, while the net profit margin fluctuated in the short term mainly due to: 1) Overseas business being in the capacity ramp-up phase, resulting in a mismatch between personnel expenses and per capita output; 2) An increase in employee welfare expenses during the period. Continuous expansion of product portfolio and enhancement of per-vehicle value

While focusing on interior and exterior trim products such as automotive instrument panel assemblies and bumper assemblies, the Company is actively developing its automotive seat business, continuously enriching and expanding its product portfolio to meet existing customers’ demand for integrated interior and exterior system solutions. In 2024, the interior business achieved steady growth, with revenue from instrument panel assemblies, door panel assemblies, and interior accessories reaching RMB8,348 million, RMB2,167 million, and RMB416 million, up 19.6%, 23.9%, and 12.4% yoy, respectively. The exterior business saw rapid volume growth, with bumper assemblies and exterior accessories generating revenue of RMB474 million and RMB229 million, up 415.0% and 29.0% yoy, respectively. The Company is currently accelerating capacity deployment for its seat business, with planned seat back panel capacities of 400 thousand sets in Mexico and 500 thousand sets in Slovakia. Additionally, the Company recently acquired a 70% equity interest in Anhui Ruiqi to accelerate seat business expansion with Chery Automobile. The new business is expected to further enhance the per-vehicle value contribution and lay a solid foundation for the Company’s long-term development. Accelerated globalization with strong contribution from the North American market

The Company has invested in and established production bases in Malaysia, Mexico, and Slovakia, and set up subsidiaries in the United States and Germany to cultivate the Southeast Asian, North American, and European markets, thereby promoting global expansion. In 2024, the overseas markets made rapid progress, with revenue in Southeast Asia, North America, and Europe all achieving high yoy growth. Among them, the North American market was the standout performer, with revenue reaching RMB700 million, up 89.14% yoy, and a gross margin of 26.37%, up 2.1 ppts yoy. This was mainly driven by the Company’s channel expansion and acquisition of new customers in North America, including a significant increase in orders from internationally renowned electric vehicle brands. Looking ahead to 2025, the production base in Slovakia is expected to commence operations, which will further expand the Company’s channels and customer base in the European market. Investment ThesisXinquan is a promising domestic automotive interior and exterior decoration enterprise. With the continuous expansion of the clients base and production capacity, it is expected to maintain sustained growth. We are optimistic about the long-term development of the Company and expect EPS to be 2.72/3.20/4.20 yuan respectively for 2025/2026/2027, a yoy increase of 35.5%/18.0%/31.0%. We offer a target price of 54.37 yuan, respectively 20/17/12.9 P/E for 2025/2026/2027, and an "Buy" rating. (Closing price as at 7 July)

Risk Factors1) Progress of new production line is below expectations

2) Electric vehicle sales fall short of expectations

3) Macroeconomic downturn affects product demand

4) Sharply rising raw material prices or sharply falling product prices Financial Data

Download PDF version... For more information on related options strategies, please click here.

| Recommendation on 11-7-2025 | | Recommendation | BUY (Upgrade) | | Price on Recommendation Date | $ 45.270 | | Suggested purchase price | N/A | | Target Price | $ 54.370 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|