|

CARDIOFLOW-B(2160)

Analysis:

MicroPort CardioFlow Medtech (2160) primarily focuses on the R&D, manufacturing, and sales of medical devices for treating heart valve diseases. Its Transcatheter Aortic Valve Implantation (TAVI) products have made significant progress in global commercialization. In China, the company covers over 630 hospitals and maintains steady growth in top-tier hospitals. Overseas, VitaFlow Liberty received CE certification in April 2024, becoming the first “Made in China” TAVI system to enter the European market, laying a strong foundation for rapid growth in the group’s overseas revenue. As of December 31, 2024, the group’s TAVI products have been adopted in nearly 100 hospitals across countries including Argentina, Colombia, Thailand, Russia, Italy, Spain, Chile, and Switzerland.Last year, the group acquired a 51% stake in MP CardioAdvent, officially expanding its business into the high-growth segment of stroke prevention for non-valvular atrial fibrillation patients within the structural heart disease market, further diversifying its revenue streams. MP CardioAdvent’s independently developed AnchorMan Left Atrial Appendage (LAA) Closure System received approval from China’s NMPA in January 2024 and CE marking in February 2025, making it the only semi-closed LAA closure product approved by the NMPA to date and the only LAA closure system with both CE and NMPA certifications in China. The accompanying AnchorMan LAA Delivery System also received NMPA and CE approvals. As of December 31, 2024, the AnchorMan LAA Closure System and its delivery system have been used in over 350 commercial procedures across more than 50 centers in 15 Chinese provinces, achieving a 100% surgical success rate with no serious complications.The group’s global registration efforts are progressing steadily. The third-generation TAVI product, VitaFlow Liberty Flex, equipped with a newly upgraded coaxial steerable delivery system, received NMPA approval in December 2024, becoming the world’s only “true” coaxial steerable self-expanding transcatheter aortic valve delivery system. As of December 31, 2024, in addition to the CE markings for VitaFlow Liberty and the AnchorMan LAA Closure and Delivery Systems, VitaFlow Liberty has secured regulatory approvals in 18 countries/regions. Registration efforts for VitaFlow Liberty and Alwide Plus in emerging markets such as Brazil, Australia, and Mexico have also reached milestone progress, with registration preparations for the AnchorMan LAA Closure and Delivery Systems in emerging markets underway.As its products continue to gain registrations in overseas markets, the group will leverage MicroPort’s global brand recognition and existing sales network to further expand its business footprint and accelerate global business development. While accelerating commercialization, the group is also steadily advancing mid- to long-term projects, achieving R&D milestones. The fourth-generation TAVI product, VitaFlow IV, is currently undergoing a rigorous engineering design process, while the independently developed Transcatheter Mitral Valve Replacement (TMVR) product has completed multiple human applications and successfully concluded follow-ups for up to two years post-surgery. (I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $1.05, Target Price: $1.20, Cut Loss Price: $0.99

|

HENGRUI PHARMA(1276)

Analysis:

The Company is an innovative international pharmaceutical enterprise dedicated to the research, development, production, and promotion of high-quality medicines. It focuses on novel drug R&D in areas including oncology, metabolic and cardiovascular diseases, immunology and respiratory disorders, and neuroscience, standing as one of China's most innovative leading pharmaceutical companies. On the news front, on July 15, the Company and U.S.-based Kailera Therapeutics jointly announced positive topline results from the Phase III clinical trial (HRS9531-301) of GLP-1/GIP dual receptor agonist HRS9531 injection for treating obesity or overweight in Chinese subjects. The partnership structure on this product also signals the Company's global ambitions. In May 2024, Hengrui Pharmaceuticals granted Kailera Therapeutics exclusive rights to develop, manufacture, and commercialize HRS9531 worldwide excluding Greater China. The deal includes upfront and milestone payments potentially totaling up to $6 billion, with Hengrui acquiring a 19.9% equity stake in Kailera.

Strategy:

買入價$70.25,目標價$77.20,止蝕價$64.00

|

|

Kuaishou (1024.HK) - AI-driven end-to-end efficiency improvement

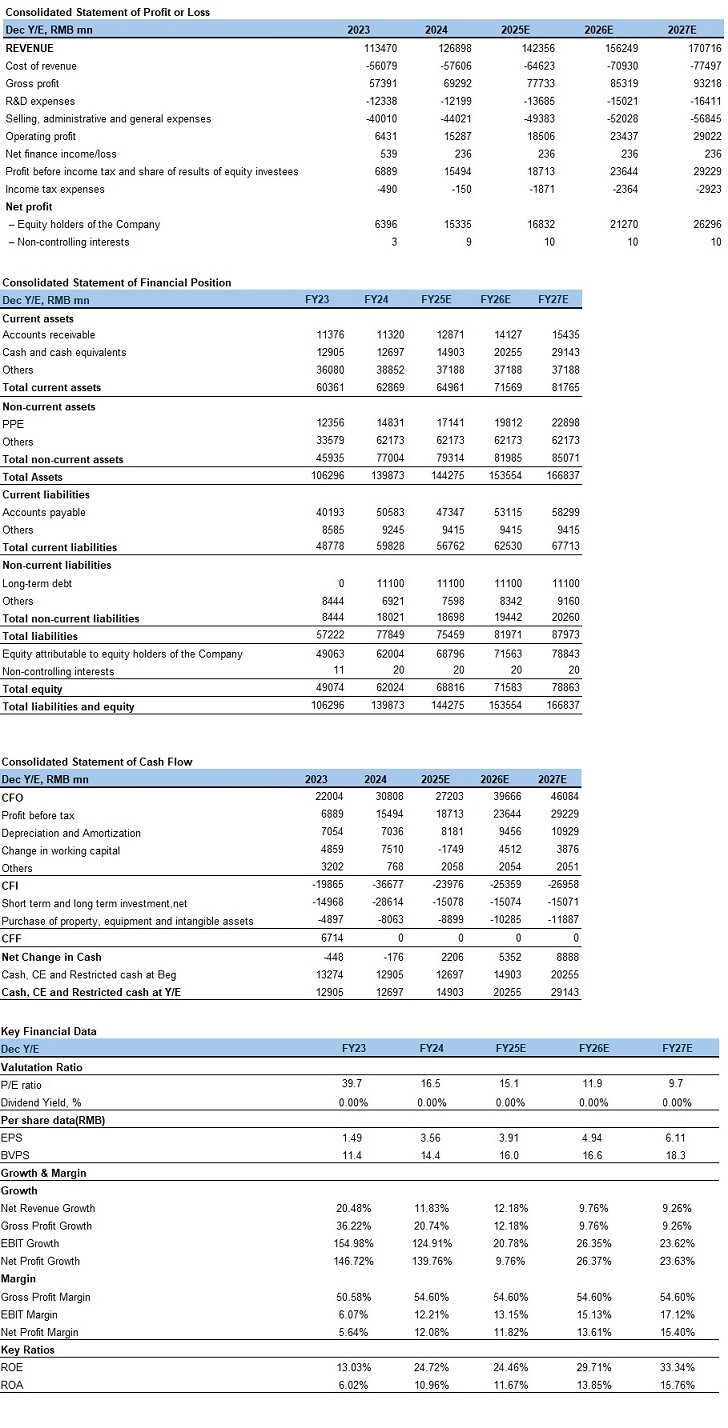

Financial summaryKuaishou is a leading content community and social platform in China and globally. As a technology company powered by and built upon artificial intelligence, Kuaishou is dedicated to continuously enriching its services and application scenarios through ongoing technological innovation and product upgrades, thereby creating value for its customers. On Kuaishou, users record and share their lives through short videos and live streaming, discover what they need, and showcase their talents. By closely collaborating with content creators and businesses, Kuaishou provides technologies, products, and services that meet users' diverse needs, including entertainment, online marketing services, e-commerce, local lifestyle services, gaming, and more. Financial performanceIn the first quarter of 2025, the company achieved total revenue of RMB 32.6 billion (Chinese yuan, same below), representing a year-over-year increase of 10.9%. In terms of profitability, operating profit reached RMB 4.3 billion, up 6.6% YoY, while adjusted net profit was RMB 4.6 billion, a 4.4% YoY increase. By segment, 1Q25 online marketing services revenue grew 8.0% YoY to RMB 18.0 billion, primarily driven by increased ad spending from marketing clients due to the adoption of AI-powered ad placement solutions. Live streaming revenue rose 14.4% YoY to RMB 9.8 billion, attributed to refined operations and diversified content. Other services revenue increased 15.2% YoY to RMB 4.8 billion, mainly fueled by e-commerce business growth. In terms of expenses, the company’s sales and marketing expenses as a percentage of total revenue decreased to 30.4% in Q1 2025 from 31.9% in the same period last year, primarily due to improved operational efficiency. In Q1 2025, Kuaishou’s average daily active users (DAUs) and monthly active users (MAUs) reached 408 million and 712 million, respectively, up 3.6% and 2.1% YoY. The app’s DAUs hit a record high and surpassed 400 million for the third consecutive quarter. Through refined user growth strategies, the average customer acquisition cost (CAC) for new users decreased. Meanwhile, enhanced content consumption experiences—driven by high-quality content, iterative traffic distribution mechanisms, and diverse community engagement features—further improved new user retention rates. Online Marketing Services: External-loop business as the core growth engine, AI-driven end-to-end efficiency improvementIn the first quarter of 2025, external-loop marketing services served as the primary growth driver, with AI technology deeply enhancing end-to-end operational efficiency. Within the content consumption sector, marketing expenditure for short dramas achieved rapid year-over-year growth. Marketing clients leveraged native pathways to elevate content value and strengthen user engagement, deepening the platform’s understanding of user preferences. In the local lifestyle sector, solutions such as native direct messaging and lead form collection boosted conversion rates, driving marketing expenditure growth of over 50.0% YoY. Meanwhile, AI technology empowered the entire workflow of online marketing service solutions, delivering efficient brand marketing and performance-driven conversions. According to management, Q2 online marketing service revenue is expected to return to double-digit YoY growth, with accelerated ad expenditure growth in the generalized shelf-based advertising space. E-commerce: Tripartite Operating Model Drives Continuous Optimization Across Multiple DomainsThe company continued to enhance consumers' shopping experience. In Q1 2025, e-commerce GMV grew by 15.4% YoY to RMB 332.3 billion, while the monthly active buyer count reached 135 million, up 7.1% YoY. By continuously developing growth resources and widely applying large-scale models, the company provided merchants with a full suite of AI-powered livestreaming tools, leading to a YoY increase of over 30.0% in new merchants joining Kuaishou during Q1 2025. Through the establishment of a tripartite operating model integrating "livestreaming + mall + short videos," the company drove continuous optimization across multiple domains. In Q1 2025, generalized shelf-based e-commerce contributed approximately 30.0% of total GMV, with the number of daily active merchants growing over 40.0% YoY, while short video-based e-commerce GMV surged by over 40.0% YoY. Livestreaming: YoY Growth Returns to Positive TerritoryThe company further refined its operations in key categories such as multi-host livestreaming and group livestreaming. By the end of Q1 2025, the number of signed agencies increased by over 25.0% YoY, while the number of signed streamers grew by over 40.0% YoY. Company valuationIn April 2025, the company launched Keling AI 2.0, introducing the innovative concept of multimodal vision-language and rolling out multimodal editing features, which have now been widely adopted across various industries including advertising marketing, short dramas, and smart devices. Leveraging AI technology, the company has empowered the entire process of online marketing service solutions, encompassing AIGC marketing material production, intelligent marketing placement agents, and large-scale marketing acompañrecommendation models, thereby enhancing clients' marketing conversion efficiency. In Q1 2025, the daily average ad spending on AIGC marketing materials reached approximately RMB 30 million. Overall, we are optimistic about the company's medium-to-long-term growth prospects and believe its fair valuation should be 17 times the projected 2025 PE, corresponding to a target price of HK$73 per share. We forecast the company's 2025-2027 operating revenues at RMB 142.4/156.2/170.7 billion, with net profits of RMB 16.8/21.3/26.3 billion, translating to EPS of RMB 3.91/4.94/6.11. The current share price implies PE multiples of 15/12/10x for 2025-2027. In conclusion, we initiate coverage with an "Accumulate" rating. Risk factors1) Slower-than-exhibitspected progress in AI applications;

2) User growth slowdown;

3) Regulatory risks in the internet industry. Financials

Current Price as of: Jul 14 2025

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est. Download PDF version...

| Recommendation on 17-7-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 65.000 | | Suggested purchase price | N/A | | Target Price | $ 73.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|