Company Profile

Geely is one of the leading enterprises in China's self-brand passenger vehicles manufacturers. The Company's products include six major brands: Geely, Geometry, Lynk, Zeekr, Livan, and Galaxy, covering the A0 to C-class passenger vehicles market.

Investment Summary

Strong Sales Momentum Continued in June, and the Sales Target Was Revised Upwards

Geely Auto's total sales in June reached 236 thousand units, up 42% yoy and 0.4% mom; of which, new energy vehicle sales amounted to 122 thousand units, up 86% yoy and down 11.2% mom, accounting for 51.8% of the total; exports reached 40 thousand units, up 12% yoy and 33.3% mom. The strong sales growth is mainly due to the powerful momentum of the new vehicle cycle, with new energy models such as the Galaxy E5, Geely Xingyuan, and Zeekr 7X, along with fuel vehicles like the Xingrui, Xingyue L, and Binyue, being well-received in the market, maintaining strong sales.

By brand segmentation: Geely brand sales in June were 193 thousand units, up 58.8% yoy and 2.1% mom; Lynk & Co. sales were 26 thousand units, up 7.7% yoy and down 7.1% mom; Zeekr brand sales were 17 thousand units, down 16.9% yoy and 10.5% mom. Among these, Geely's China Star sub-brand sales totaled 103 thousand units, up 6% yoy and 18% mom; the Galaxy sub-brand sold 90 thousand units, up 202% yoy and down 11.8% mom.

We note that the Company's strategy of creating blockbuster models is beginning to show results. The Geely Xingyuan achieved sales of 200 thousand units in H1, becoming the top-selling model across all categories; the Lynk & Co. 900 remained in the top three of the large SUV market for eight consecutive weeks, and the Zeekr 7X stayed as the top-selling pure electric SUV for Chinese brands priced over RMB200 thousand.

Looking at the cumulative data for H1, the Company achieved total sales of 1,409 thousand units, up 47.4% yoy, and has completed 52% of its annual sales target of 2.71 million units. Among them, new energy vehicles reached 725 thousand units, up 126.5% yoy, accounting for 51.5%. Geely brand's cumulative sales totaled 1164 thousand units, up 56.99% yoy (of which the Galaxy series sold 548 thousand units, up 232% yoy); Zeekr's cumulative sales were 91 thousand units, up 3.3% yoy; Lynk & Co. sales were 154 thousand units, up 22.3% yoy. Exports for the first six months totaled 184 thousand units, down 7.7% yoy. Given the strong sales performance, the Company has revised its annual sales target to 3 million units, with the corresponding growth rate revised upwards from 25% to 38%.

Impressive Result in the First Quarter

Thanks to the strong sales performance, Geely Auto achieved robust growth in both revenue and profits. According to the Q1 report, the Company achieved revenue of RMB72,495 million (RMB, the same below) in Q1 2025, up 24.5% yoy and flat mom; net profit attributable to the parent company was RMB5,672 million, up 263.4% yoy and 58.5% mom. According to the Company's announcement, due to rapid growth in export business, the depreciation of the RMB against the ruble, and other factors, exchange rate fluctuations positively impacted after-tax profit by approximately RMB2-2.3 billion. Excluding foreign exchange gains, core net profit was about RMB3.48 billion, achieving an 84.3% yoy increase.

In the first quarter, the Company sold 704 thousand vehicles, up 47.9% yoy and 2.5% mom, with growth higher than revenue, mainly due to the increased share of lower-priced models, which led to a 15.8% decrease in average selling price yoy.

However, driven by positive economies of scale and the return to the "One Geely" integration strategy, gross margin increased by 0.2 ppts to 15.8%, and sales, administration, and R&D expense ratio decreased by 2.6 ppts to 11.6%.

Additionally, Zeekr's vehicle gross margin was about 18.8%, up 1.8 ppts yoy, turning a loss (-RMB540 million) into a profit (RMB510 million).

Privatization of Zeekr, Speeding up Strategic Integration

On 15 July, the Company announced that it had signed a privatization merger agreement with Zeekr to acquire all the remaining non-controlling shares and American Depositary Shares of Zeekr, and delist Zeekr from the New York Stock Exchange. Subsequently, Zeekr will become a wholly-owned subsidiary. Zeekr's original shareholders can choose either USD2.687 or 1.23 newly issued Geely Auto shares for each Zeekr share (USD26.87 or 12.3 new Geely Auto shares for each Zeekr American Depositary Share). The Company will pay a maximum of USD2.399 billion or 1,089 million Geely Auto shares, accounting for 11% of the current equity.

This privatization is an important step in Geely's return to the "One Geely" strategy, validating that Geely is accelerating its shift from multi-brand expansion to a more consolidated approach. Mergers and acquisitions can enhance strategic coordination and business integration between sub-brands, eliminate competition within the same industry, reduce duplication of investment, complement sales networks, improve supply chain efficiency, and drive cost reduction and efficiency improvement. In the future, the Company will accelerate technology integration and cost optimization. For example, Zeekr's SEA architecture will be implemented in the high-end Galaxy L9 model, and channels for Zeekr and Lynk & Co. will be further integrated, saving 8-20% in supply chain, R&D, and other costs.

In terms of new models, the Company plans to release 10 new models in 2025, with Galaxy, Zeekr, and Lynk & Co. brands releasing 5, 3, and 2 models respectively. The already launched StarShine 8, Lynk & Co. 900, and Zeekr 007GT have received a positive market response, and their potential to become blockbuster models is increasingly evident. Noteworthy new models in H2 include the launch of the Galaxy A7/M9, Zeekr 9X/8X, and Lynk & Co. 10EM-P, as well as the gradual ramp-up of overseas markets with the introduction of new products.

Investment Thesis

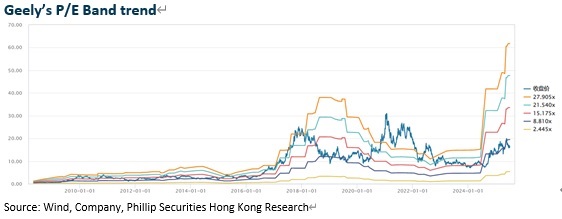

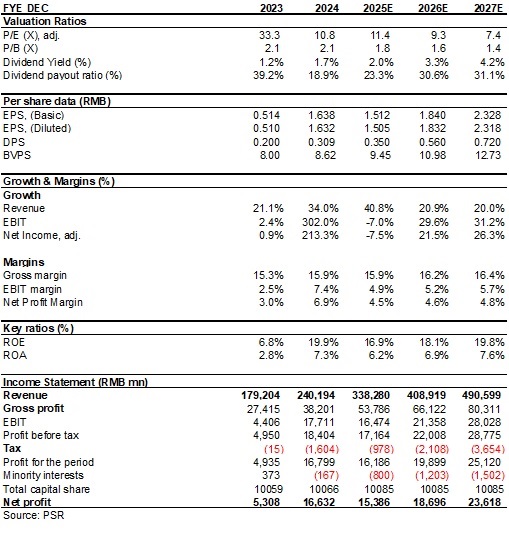

We revised our financial forecast and target price to HK$24.1, equivalent to 14.6/12/9.5x P/E ratio in 2025/2026/2027, and we give the rating of Buy. (Closing price as at 22 July)

Financials

(Closing price as at 22 July)

Click here to download PDF version...