|

ASMPT(522)

Analysis:

ASMPT announced its second-quarter results for 2025. Sales revenue reached HK$3.4 billion (US$436 million), up 1.8% year-on-year and 8.9% quarter-on-quarter. New order bookings totaled HK$3.75 billion, exceeding expectations, with a significant 20.2% year-on-year increase and 11.9% quarter-on-quarter growth. Operating profit was HK$169 million, up 25.4% year-on-year and 5.9% quarter-on-quarter. Net profit was HK$134 million, down 1.7% year-on-year but up 62.6% quarter-on-quarter. Basic earnings per share were HK$0.32, down 3% year-on-year but up 60% quarter-on-quarter.In the first half of 2025, driven by the strong artificial intelligence (AI) wave, the Group’s advanced packaging business continued to grow, contributing significantly to total sales revenue, accounting for approximately 39% of total sales, primarily driven by sustained demand for Thermal Compression Bonding (TCB) tools. The Group secured follow-on orders for TCB tools in memory and logic applications, maintaining the largest installed base of TCB tools globally, exceeding 500 units. Additionally, new order bookings for power management solutions reflected growing demand from mainstream businesses in AI data centers, while orders from China saw significant growth, fueled by electric vehicles and consumer end markets.Regarding next-generation tools, the Group expects Hybrid Bonding (HB) to coexist with other packaging technologies, with adoption progressing gradually. Progress continued with first- and second-generation HB tools, with customers actively engaged in setup, certification, and delivery stages. Notably, second-generation HB tools offer competitive advantages in alignment and bonding accuracy, footprint, and output per hour. The Group expects to deliver these second-generation tools to a high-bandwidth memory (HBM) customer in Q3 2025.The rapid growth of AI continues to drive data center bandwidth demand, boosting the need for optical transceivers and Co-Packaged Optics (CPO) applications. The Group’s photonics tools enable the packaging of higher-bandwidth transceivers, particularly 800G and above. Due to its significant market leadership, the Group expects sustained order momentum from global transceiver manufacturers serving major AI companies. Although the CPO market is still in its early stages, the Group has actively collaborated with leading global CPO companies and secured a significant order from a leading integrated equipment manufacturer in the first half of 2025, positioning it favorably to increase market share.The Group forecasts Q3 2025 sales revenue to range between US$445 million and US$505 million, with the midpoint indicating a 10.8% year-on-year increase and 8.9% quarter-on-quarter growth, surpassing market expectations. The Group reiterated its projection that the total addressable market for TCB will reach US$1 billion by 2027 and will continue to focus on strengthening its leadership in the TCB market for memory and logic applications.

Strategy:

Buy-in Price: HK$62. Target price: HK$69. Cut-loss Price: HK$59

|

WellCell Holdings(2477)

Analysis:

On the evening of July 21, Jingwei TianDi announced via the Hong Kong Stock Exchange its official entry into the cryptocurrency payment sector. Concurrently, it launched the stablecoin payment platform "Fopay" on the same day. According to the announcement, Fopay is developed based on the stablecoin crypto payment concept, offering an all-in-one payment solution. Currently, it provides stablecoin custody and prepaid card payment functionality through several licensed partners. The Board believes that launching Fopay and establishing this new business segment will enable the company to explore more commercial opportunities and benefit shareholders overall. In fact, Jingwei TianDi's move into crypto payments was not abrupt. In late May this year, the group had disclosed its exploration of new business segments, including payment services (encompassing global payment services utilizing blockchain technology) and fintech operations.

Strategy:

Buy-in Price: $9.12. Target Price: $10.04. Cut-loss price: $8.22

|

|

TME (1698.HK)-ARPPU as the primary growth driver

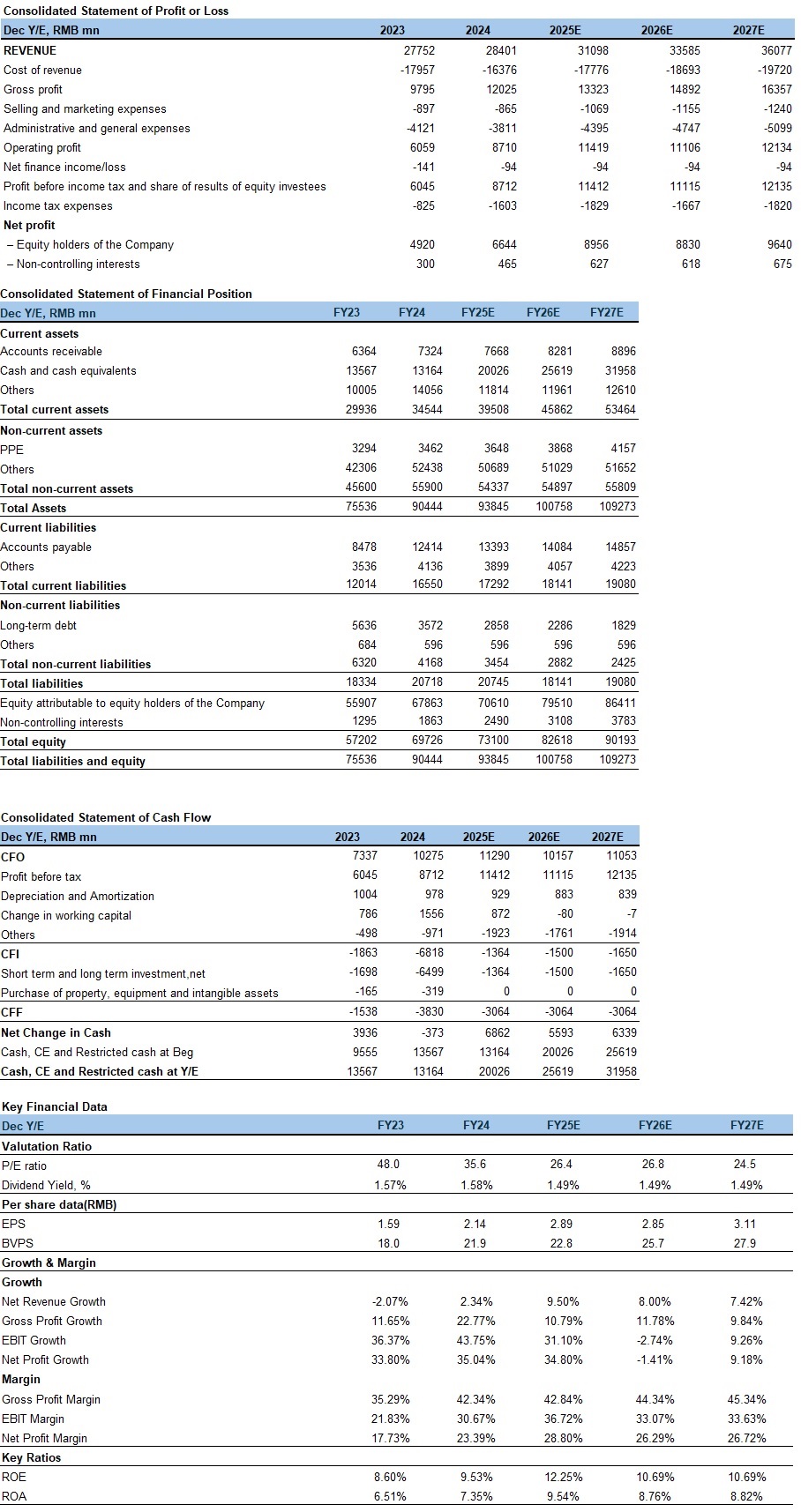

Company backgroundTencent Music Entertainment (TME) is China’s trailblazer in online music entertainment services, offering both online music and music-centric social entertainment services. The company boasts an extensive user base and operates four leading mobile music products in the domestic market: QQ Music, Kugou Music, Kuwo Music, and WeSing. TME provides users with diversified music social entertainment products, creating an all-scenario music experience that includes "discover, listen, sing, watch, perform, and socialize." This empowers users to engage in music creation, appreciation, sharing, and interaction. Financial performanceIn the first quarter of 2025, the company generated total revenue of RMB 7.4 billion, representing a year-over-year increase of 8.7%. By segment, online music service revenue reached RMB 5.8 billion, up 15.9% year-over-year, primarily driven by growth in subscription service revenue and advertising service revenue. Social entertainment service and other service revenue amounted to RMB 1.6 billion, down 11.9% year-over-year, mainly due to impacts from compliance procedures and adjustments to live-streaming features. In terms of profitability, the company’s gross profit margin rose to 44.1% in Q1 2025, largely attributable to an optimized membership mix and increased proprietary content. Operating profit surged to RMB 4.8 billion, a 146.9% year-over-year increase, primarily fueled by a one-time gain from equity obtained through an associate company. Adjusted net profit grew to RMB 2.2 billion, up 22.8% year-over-year. Concurrently, the company announced an annual dividend of USD 0.09 per ordinary share for 2024. Online Music Services: ARPPU as the Core Growth EngineIn the first quarter of 2025, online music subscription revenue reached RMB 4.2 billion, up 16.6% year-over-year, primarily driven by Super Digital Music Package (SDIP) growth and reduced promotional discounts. Advertising service revenue totaled RMB 1.6 billion, increasing 13.7% year-over-year, mainly attributable to diversified product offerings. Operationally, the number of online music paying users grew 8.3% YoY to 123 million, with the paying ratio further rising to 22.1%. Narrower promotional discounts lifted Average Revenue Per Paying User (ARPPU) by 7.5% YoY from RMB 10.6 to RMB 11.4 monthly, while Monthly Active Users (MAU) contracted 4.0% YoY to 555 million. The company stimulates deeper and broader music consumption through enriched content services, diversified membership privileges, and precision operations, driving high-quality growth in both standard and premium memberships. For non-paying users: on one front, incentive-based advertisements and interactive tasks maintain engagement while generating ad revenue; on another front, fan economy models – including digital albums, merchandise, and song rewards – create additional monetization touchpoints to enhance overall user monetization efficiency. We expect ARPPU elevation to remain the primary growth driver. Company valuationAccording to management, the company will continue optimizing its membership system, enriching exclusive benefits, and implementing precision operation strategies to drive dual growth in both SDIP scale and ARPPU. Consequently, we forecast 2025-2027 online music service revenue at RMB25.4/28.5/31.3 billion, representing YoY growth of 17%/12%/10%. Simultaneously, considering tightening regulations and plateauing traffic in the livestreaming industry, we project social entertainment service and other service revenue at RMB5.7/5.1/4.7 billion, reflecting YoY declines of 15%/10%/7%. For the full-year outlook, the dual engines of SVIP subscriptions and advertising revenue – coupled with optimized content cost control and deepened partnerships with copyright holders – will sustain momentum. Management anticipates accelerated full-year revenue growth and continued gross margin expansion. While sales expenses will increase moderately but at a slower pace than revenue growth, administrative expenses will remain stable. This will drive significant YoY improvement in net profit margin. Therefore, we project 2025-2027 total operating revenue at RMB31.1/33.6/36.1 billion, with net profit attributable to shareholders at RMB9.0/8.8/9.6 billion, translating to EPS of RMB2.89/2.85/3.11. Given the company’s high-growth profile, we select NetEase Cloud Music and Spotify as comparable companies. Applying a 30x 2025 forecasted P/E multiple yields a target price of HKD 95. Current share price implies 2025-2027 P/E multiples of 26/27/25x. We initiate coverage with a "Accumulate" rating. Risk factors1) Intensifying competition;

2) Slower-than-expected user growth;

3) Copyright risks. Financials

Current Price as of: Jul 21

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est. Download PDF version...

| Recommendation on 24-7-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 84.000 | | Suggested purchase price | N/A | | Target Price | $ 95.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|