|

ChinaSoft International (354)

Analysis:

ChinaSoft International focuses its business on industries such as power, finance, government services, transportation, public utilities, and enterprise manufacturing, developing HarmonyOS and AI-driven industry scenarios and implementation solutions. In the domestic market, it targets economically developed regions like the Greater Bay Area, Yangtze River Delta, Beijing-Tianjin-Hebei, and central-western hub regions, with deep engagement in cities including Beijing, Shenzhen, Xi’an, Guangzhou, Nanjing, Shanghai, and Chengdu, comprehensively promoting “AI+” solutions. Internationally, the company has established R&D and delivery centers in Hong Kong, Thailand, Japan, Singapore, Saudi Arabia, and the UAE, forming a joint venture, JAT, in Saudi Arabia, and successfully delivering projects in digital governance, smart cities, and smart venues.In the AI domain, the group’s business spans a complete AI technology stack, covering computing infrastructure construction and operation, data governance, model training, reasoning deployment, edge intelligence, cloud intelligence, next-generation AI-native ERP, and industry specific applications. It provides integrated services from hardware, algorithms, and platforms to solutions, forming full-stack AI capabilities to help clients fully implement and apply AI, driving business transformation. The group has established a Science and Innovation Center, leveraging DeepSeek and its overall AI service capabilities to offer a four-in-one service model: AI computing services, AI engineering implementation, AI scenario consulting, and AI agent services. It is equipped with three innovative lab environments—AILab, Enterprise Core Economics Lab, and IDSLab—to promote the transformation and application of cutting-edge technological achievements, continuously building an open AI ecosystem.The group’s computing operations and infrastructure construction are progressing steadily, optimizing configurations based on Ascend AI computing power and expanding computing capacity in Xi’an and other locations, establishing multiple computing centers. In collaboration with Huawei, it has built the Changping Digital Power Science and Innovation Center, providing a fully domestic computing foundation. Its independently developed LMBSS computing management system successfully won the bid for the Guiyang Hyper-Connected New Computing Project, further solidifying its advantage in computing operations. Additionally, in industries such as smart finance, smart energy and power, smart governance, and intelligent manufacturing, the group has launched customized solutions, earning high market recognition.Looking ahead, the group will continue to rely on its domestic computing foundation, leveraging its model factory, JointPilot, Agent-based applications, domestically controlled ERP systems, and HarmonyOS ecosystem-enabled hardware and software, along with its full-stack AI products and services, to empower intelligent upgrades in enterprise application scenarios, further enhancing enterprise productivity.

Strategy:

Buy-in price: $5.62. Target price:$ 6.00, then $ 6.2. Cut-loss price: $5.40

|

Ganfeng Lithium(1772)

Analysis:

Since September 2024, the utilization rates of leading domestic battery manufacturers have shown improvement. Since 2025, overseas orders for top lithium battery equipment companies have continued to grow, with the domestic market seeing significant recovery. Full-year domestic expectations are likely to be revised upward. Solid-state batteries have recently seen multiple catalysts: overseas companies like QuantumScape and Solid Power have made smooth technological progress, with their stock prices continuing to hit new highs, drawing intense capital market attention. On the domestic policy front, the "All-Solid-State Battery Identification Methods" released in May 2025 standardized industry benchmarks, while the newly revised "Safety Requirements for Traction Battery of Electric Vehicles" strengthened safety standards, laying a solid foundation for solid-state battery development. At the industrial level, as leading battery manufacturers gradually implement and operationalize pilot production lines for all-solid-state batteries, and with the MIIT's solid-state battery special project undergoing mid-term acceptance, the solid-state battery equipment sector is expected to be among the first to benefit.

Strategy:

Buy-in price: $30.80. Target price: $33.85. Cut-loss price: $27.90

|

|

TME (1698.HK)-ARPPU as the primary growth driver

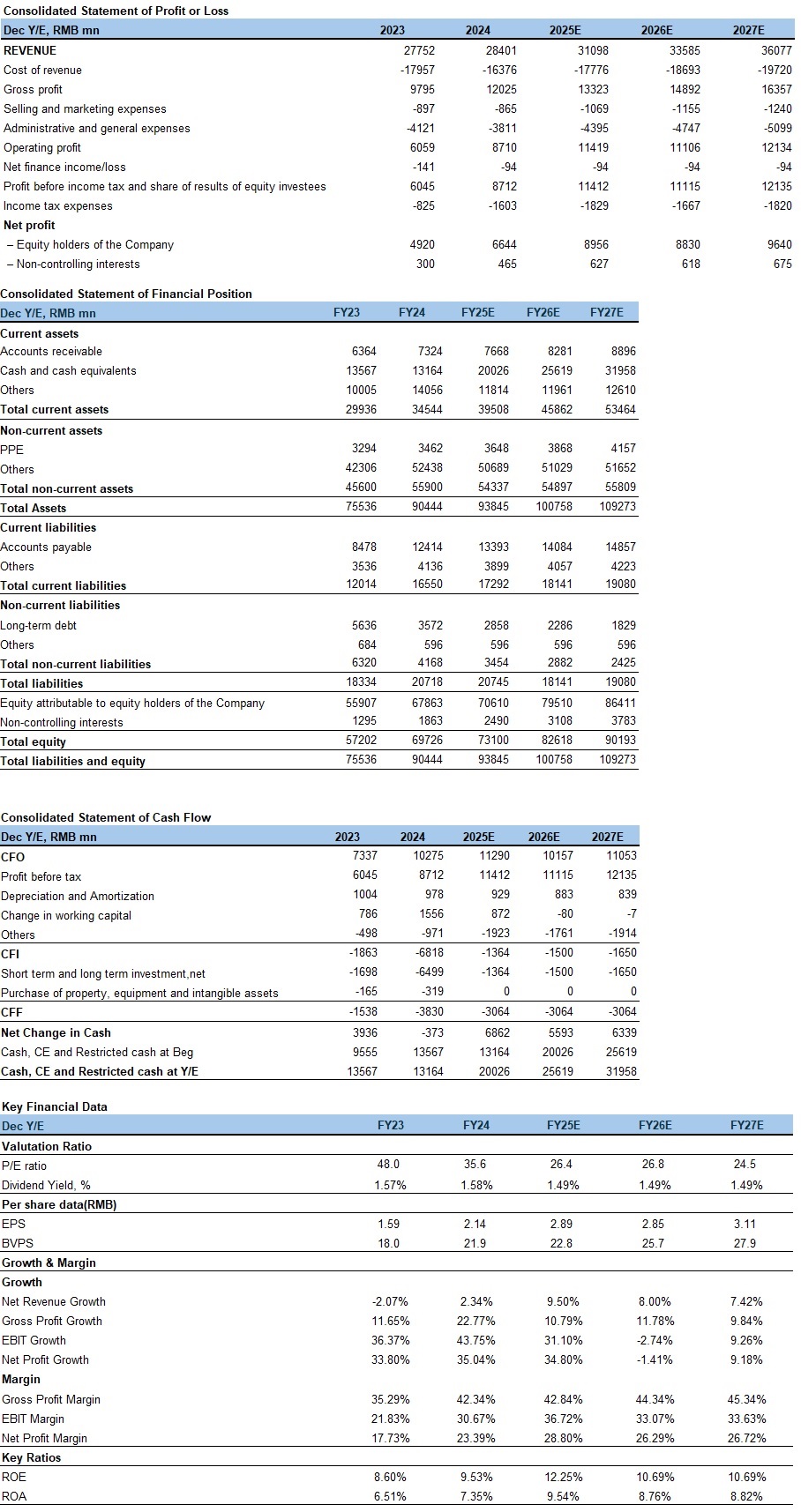

Company backgroundTencent Music Entertainment (TME) is China’s trailblazer in online music entertainment services, offering both online music and music-centric social entertainment services. The company boasts an extensive user base and operates four leading mobile music products in the domestic market: QQ Music, Kugou Music, Kuwo Music, and WeSing. TME provides users with diversified music social entertainment products, creating an all-scenario music experience that includes "discover, listen, sing, watch, perform, and socialize." This empowers users to engage in music creation, appreciation, sharing, and interaction. Financial performanceIn the first quarter of 2025, the company generated total revenue of RMB 7.4 billion, representing a year-over-year increase of 8.7%. By segment, online music service revenue reached RMB 5.8 billion, up 15.9% year-over-year, primarily driven by growth in subscription service revenue and advertising service revenue. Social entertainment service and other service revenue amounted to RMB 1.6 billion, down 11.9% year-over-year, mainly due to impacts from compliance procedures and adjustments to live-streaming features. In terms of profitability, the company’s gross profit margin rose to 44.1% in Q1 2025, largely attributable to an optimized membership mix and increased proprietary content. Operating profit surged to RMB 4.8 billion, a 146.9% year-over-year increase, primarily fueled by a one-time gain from equity obtained through an associate company. Adjusted net profit grew to RMB 2.2 billion, up 22.8% year-over-year. Concurrently, the company announced an annual dividend of USD 0.09 per ordinary share for 2024. Online Music Services: ARPPU as the Core Growth EngineIn the first quarter of 2025, online music subscription revenue reached RMB 4.2 billion, up 16.6% year-over-year, primarily driven by Super Digital Music Package (SDIP) growth and reduced promotional discounts. Advertising service revenue totaled RMB 1.6 billion, increasing 13.7% year-over-year, mainly attributable to diversified product offerings. Operationally, the number of online music paying users grew 8.3% YoY to 123 million, with the paying ratio further rising to 22.1%. Narrower promotional discounts lifted Average Revenue Per Paying User (ARPPU) by 7.5% YoY from RMB 10.6 to RMB 11.4 monthly, while Monthly Active Users (MAU) contracted 4.0% YoY to 555 million. The company stimulates deeper and broader music consumption through enriched content services, diversified membership privileges, and precision operations, driving high-quality growth in both standard and premium memberships. For non-paying users: on one front, incentive-based advertisements and interactive tasks maintain engagement while generating ad revenue; on another front, fan economy models – including digital albums, merchandise, and song rewards – create additional monetization touchpoints to enhance overall user monetization efficiency. We expect ARPPU elevation to remain the primary growth driver. Company valuationAccording to management, the company will continue optimizing its membership system, enriching exclusive benefits, and implementing precision operation strategies to drive dual growth in both SDIP scale and ARPPU. Consequently, we forecast 2025-2027 online music service revenue at RMB25.4/28.5/31.3 billion, representing YoY growth of 17%/12%/10%. Simultaneously, considering tightening regulations and plateauing traffic in the livestreaming industry, we project social entertainment service and other service revenue at RMB5.7/5.1/4.7 billion, reflecting YoY declines of 15%/10%/7%. For the full-year outlook, the dual engines of SVIP subscriptions and advertising revenue – coupled with optimized content cost control and deepened partnerships with copyright holders – will sustain momentum. Management anticipates accelerated full-year revenue growth and continued gross margin expansion. While sales expenses will increase moderately but at a slower pace than revenue growth, administrative expenses will remain stable. This will drive significant YoY improvement in net profit margin. Therefore, we project 2025-2027 total operating revenue at RMB31.1/33.6/36.1 billion, with net profit attributable to shareholders at RMB9.0/8.8/9.6 billion, translating to EPS of RMB2.89/2.85/3.11. Given the company’s high-growth profile, we select NetEase Cloud Music and Spotify as comparable companies. Applying a 30x 2025 forecasted P/E multiple yields a target price of HKD 95. Current share price implies 2025-2027 P/E multiples of 26/27/25x. We initiate coverage with a "Accumulate" rating. Risk factors1) Intensifying competition;

2) Slower-than-expected user growth;

3) Copyright risks. Financials

Current Price as of: Jul 21

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est. Download PDF version...

| Recommendation on 25-7-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 84.000 | | Suggested purchase price | N/A | | Target Price | $ 95.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|