|

CANSINOBIO(6185)

Analysis:

CanSino Biologics’ mission is to develop, produce, and commercialize high-quality, innovative, and affordable vaccines. Its vaccine product pipeline is strategically aimed at targeting large and underserved global markets, which can be summarized into three categories: (i) global innovative vaccines to address unmet medical needs worldwide; (ii) first-in-China vaccines with higher quality to replace current mainstream vaccines in China; and (iii) preclinical vaccines candidates.

The Group’s five products in the commercialization stage include Menhycia, Menphecia, Convidecia, Convidecia Air, and Ad5-EBOV. Menhycia is the first-in-China and the first MCV4 to receive new drug marketing approval, not only narrowing the gap between China and developed countries in this field but also meeting China’s demand for high-end vaccines in this area, providing a superior solution for preventing meningococcal disease in infants and young children. Menphecia is China’s best bivalent meningococcal vaccine, with Phase III clinical trials showing better safety in the 3-month-old group and better immunogenicity in the 6- to 23-month-old group compared to other major MCV2 products currently approved in China. Convidecia is a vaccine constructed using genetic engineering methods, with a replication-defective type 5 adenovirus as the vector, expressing the novel coronavirus S antigen, for preventing COVID-19 disease. Convidecia Air is the world’s first inhaled COVID vaccine using nebulized recombinant virus as the vector. It not only stimulates humoral and cellular immunity but also induces mucosal immunity, effectively achieving triple comprehensive protection, without the need for intramuscular injection during the process. Ad5-EBOV uses adenovirus vector technology to induce an immune response against Ebola virus disease. Compared to existing global Ebola virus vaccines and investigational vaccines, Ad5-EBOV has several key advantages: (i) as a lyophilized formulation proven to be stable for 12 months at 2°C to 8°C, it offers better stability; (ii) it is an inactivated non-replicating viral vector vaccine with fewer safety concerns; and (iii) it is a potential broad-spectrum protective vaccine against Zaire Ebola virus.

For the year ended December 31, 2024, the Group achieved revenue of approximately RMB 824 million, a significant increase of 139% compared to 2023, mainly due to the Group fully leveraging the advantages of being the only MCV4 product in the Chinese market, achieving substantial sales growth. This product holds a leading position in the market and, through precise marketing, continues to increase product penetration, driving sustained sales growth. Looking ahead, the Group will be committed to continuing the commercialization of Menhycia and Minaixi, and will continue to advance the exploration and development of new investigational vaccines through strategic collaborations combining internal R&D with external partners. At the same time, it will actively seek potential global collaborations and acquisitions, continuously expanding industrialization and commercialization coverage in countries and regions such as Southeast Asia, the Middle East, and Latin America, accelerating the enhancement of international market competitiveness. (I do not hold the above-mentioned stock).

Strategy:

Buy-in Price:HK$42, Target Price:HK$47, Cut Loss Price: HK$39.5

|

WUXI APPTEC(2359)

Analysis:

Since 2025, the government has repeatedly proposed policies to optimize centralized drug procurement and support innovative drugs, while the commercial insurance innovative drug catalog is imminent, indicating a favorable pharmaceutical policy environment. The eleventh round of national drug centralized procurement has commenced its drug information reporting phase. The rules and price reduction rates for this round are expected to be optimized, with a focus on "anti-involution"—no longer anchored to the lowest price—strict quality control, and scientific selection of procurement varieties. The company's long-term value is anchored in its globalized production capacity layout and technological iteration capabilities. Following the expected launch of production bases in Singapore and the United States in 2026-2027, global capacity will increase by 30%, effectively mitigating geopolitical impacts on capacity allocation. The TIDES (oligonucleotide and peptide therapeutics) business achieved a 70% year-on-year revenue growth in the first half of the year, with a 103.9% increase in order backlog, demonstrating that the new technology platform has formed economies of scale.

Strategy:

Buy-in Price:$98.45,Target Price: $108.30,Cut Loss Price: $89.00

|

|

TME (1698.HK) - ARPPU as the primary growth driver

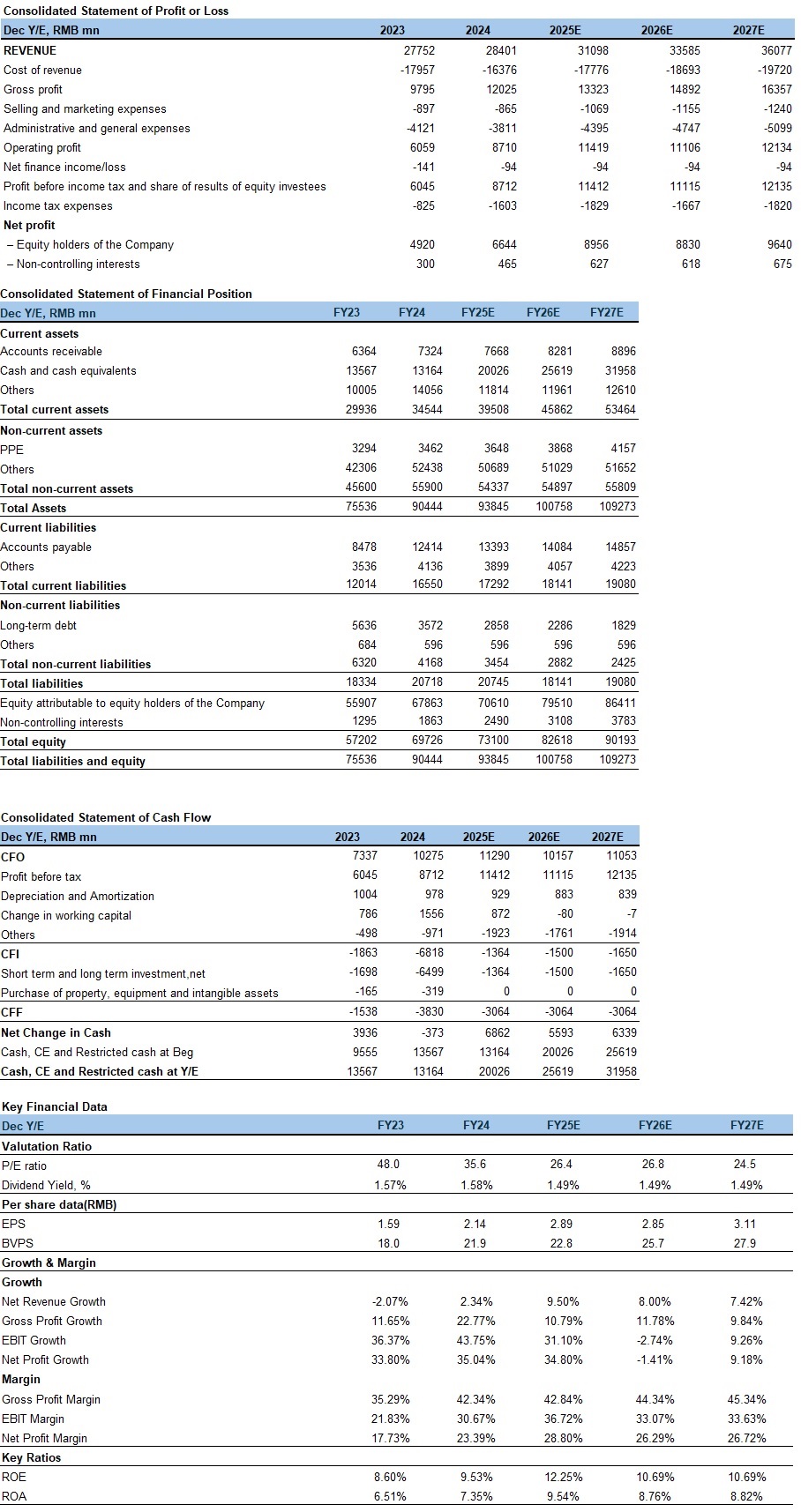

Company backgroundTencent Music Entertainment (TME) is China’s trailblazer in online music entertainment services, offering both online music and music-centric social entertainment services. The company boasts an extensive user base and operates four leading mobile music products in the domestic market: QQ Music, Kugou Music, Kuwo Music, and WeSing. TME provides users with diversified music social entertainment products, creating an all-scenario music experience that includes "discover, listen, sing, watch, perform, and socialize." This empowers users to engage in music creation, appreciation, sharing, and interaction. Financial performanceIn the first quarter of 2025, the company generated total revenue of RMB 7.4 billion, representing a year-over-year increase of 8.7%. By segment, online music service revenue reached RMB 5.8 billion, up 15.9% year-over-year, primarily driven by growth in subscription service revenue and advertising service revenue. Social entertainment service and other service revenue amounted to RMB 1.6 billion, down 11.9% year-over-year, mainly due to impacts from compliance procedures and adjustments to live-streaming features. In terms of profitability, the company’s gross profit margin rose to 44.1% in Q1 2025, largely attributable to an optimized membership mix and increased proprietary content. Operating profit surged to RMB 4.8 billion, a 146.9% year-over-year increase, primarily fueled by a one-time gain from equity obtained through an associate company. Adjusted net profit grew to RMB 2.2 billion, up 22.8% year-over-year. Concurrently, the company announced an annual dividend of USD 0.09 per ordinary share for 2024. Online Music Services: ARPPU as the Core Growth EngineIn the first quarter of 2025, online music subscription revenue reached RMB 4.2 billion, up 16.6% year-over-year, primarily driven by Super Digital Music Package (SDIP) growth and reduced promotional discounts. Advertising service revenue totaled RMB 1.6 billion, increasing 13.7% year-over-year, mainly attributable to diversified product offerings. Operationally, the number of online music paying users grew 8.3% YoY to 123 million, with the paying ratio further rising to 22.1%. Narrower promotional discounts lifted Average Revenue Per Paying User (ARPPU) by 7.5% YoY from RMB 10.6 to RMB 11.4 monthly, while Monthly Active Users (MAU) contracted 4.0% YoY to 555 million. The company stimulates deeper and broader music consumption through enriched content services, diversified membership privileges, and precision operations, driving high-quality growth in both standard and premium memberships. For non-paying users: on one front, incentive-based advertisements and interactive tasks maintain engagement while generating ad revenue; on another front, fan economy models – including digital albums, merchandise, and song rewards – create additional monetization touchpoints to enhance overall user monetization efficiency. We expect ARPPU elevation to remain the primary growth driver. Company valuationAccording to management, the company will continue optimizing its membership system, enriching exclusive benefits, and implementing precision operation strategies to drive dual growth in both SDIP scale and ARPPU. Consequently, we forecast 2025-2027 online music service revenue at RMB25.4/28.5/31.3 billion, representing YoY growth of 17%/12%/10%. Simultaneously, considering tightening regulations and plateauing traffic in the livestreaming industry, we project social entertainment service and other service revenue at RMB5.7/5.1/4.7 billion, reflecting YoY declines of 15%/10%/7%. For the full-year outlook, the dual engines of SVIP subscriptions and advertising revenue – coupled with optimized content cost control and deepened partnerships with copyright holders – will sustain momentum. Management anticipates accelerated full-year revenue growth and continued gross margin expansion. While sales expenses will increase moderately but at a slower pace than revenue growth, administrative expenses will remain stable. This will drive significant YoY improvement in net profit margin. Therefore, we project 2025-2027 total operating revenue at RMB31.1/33.6/36.1 billion, with net profit attributable to shareholders at RMB9.0/8.8/9.6 billion, translating to EPS of RMB2.89/2.85/3.11. Given the company’s high-growth profile, we select NetEase Cloud Music and Spotify as comparable companies. Applying a 30x 2025 forecasted P/E multiple yields a target price of HKD 95. Current share price implies 2025-2027 P/E multiples of 26/27/25x. We initiate coverage with a "Accumulate" rating. Risk factors1) Intensifying competition;

2) Slower-than-expected user growth;

3) Copyright risks. Financials

Current Price as of: Jul 21

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est. Download PDF version...

| Recommendation on 28-7-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 84.000 | | Suggested purchase price | N/A | | Target Price | $ 95.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|