Company Profile

Yutong Bus is a leading domestic bus manufacturer. Its products cover various market segments including long-distance coaches, tourist coaches, city buses, staff commuter buses, school buses, sightseeing buses, airport shuttle buses, autonomous microcirculation buses, and special-purpose vehicles, meeting market demands across different vehicle lengths from 5 metres to 18 metres. The company has maintained the number one sales volume of large and medium-sized buses in China for 22 consecutive years, securing its industry-leading position.

Investment Summary

Stable Growth in First Quarter Results

In the first quarter of 2025, Yutong Bus reported revenue of RMB6.42 billion (RMB, the same below), down 3.0% yoy, with net profit attributable to the parent company of RMB755 million, up 14.9% yoy, and net profit attributable to the parent company excluding non-recurring items of RMB642 million, up 12.5% yoy.

Gross Margin Declined, Net Profit Margin Rose

In the first quarter, the company sold a total of 9,011 buses, up 16.6% yoy. However, due to a decrease in the proportion of large and medium-sized buses, which typically have higher unit prices, the ASP dropped by RMB144 thousand or 16.8% yoy to RMB712 thousand. The proportion of large and medium-sized buses in the first quarter was 80.6%, down 9.5 ppts yoy. Gross margin fell by 2.6 ppts yoy to 18.9%.

The period expense ratio was 10.8%, up 0.35 ppts yoy, with selling, administration, R&D, and financial expense ratios at 3.36%, 2.78%, 4.57%, and 0.12%, respectively, down 0.13, 0.04, 0.13, and up 0.65 ppts yoy, respectively. Benefiting from the reversal of bad debt provisions on accounts receivable, the Company recorded a combined gain of RMB280 million from credit and asset impairment, up RMB250 million yoy, significantly boosting its results. As a result, the net profit margin attributable to the parent company rose by 1.83 ppts yoy to 11.76%. In the first quarter, the Company recorded net cash inflow from operating activities of RMB1.42 billion, maintaining a healthy financial position.

According to the Company’s guidance at the beginning of the year, revenue for 2025 is expected to reach RMB42.133 billion, up 13.2% yoy. Operating costs and expenses are planned at RMB37.203 billion, equivalent to operating profit of RMB4.93 billion, up 62.1% yoy, reflecting strong confidence.

Policy-Driven Vehicle Replacement Expected to Continue in H2

Since 2024, China has intensified efforts in implementing the vehicle replacement policy. In July 2024, the Ministry of Transport issued the Implementation Rules for Subsidies for the Renewal of New Energy City Buses and Power Batteries, granting an average subsidy of RMB80 thousand per new energy city bus, and RMB42 thousand per battery replacement. In January and April 2025, two batches totalling RMB162 billion in central government funds were allocated to support the implementation of the vehicle replacement policy. A further RMB138 billion is scheduled for phased release in Q3 and Q4.

At the same time, the pilot programme for full electrification in the public sector continues to stimulate demand in the new energy bus market. Multiple cities including Shanghai have introduced targets to increase the proportion of new energy buses. In H1 2025, domestic sales of new energy buses reached 80.3 thousand units, up 52.4% yoy, with a penetration rate of 30%.

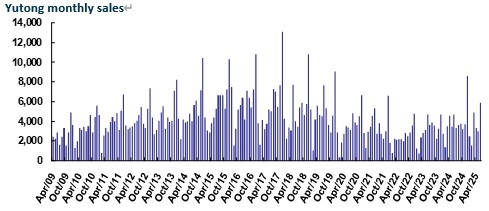

Since the beginning of this year, sales in the domestic large and medium bus market have remained stable. From January to June, 52.1 thousand large and medium buses were sold, up 2.1% yoy, including 32.1 thousand large buses, up 0.2% yoy, and 20 thousand medium buses, up 5.3% yoy. In H2, supported by the vehicle replacement policy, peak tourism season, and export growth, sales of large and medium buses are expected to continue increasing. In H1 2025, the Company sold 12 thousand buses, up 3.7% yoy, outpacing the industry average and reflecting that leading enterprises with competitive advantages are the first to benefit.

Source: Company, Phillip Securities Hong Kong Research

Overseas Market Expected to Unlock Growth Potential

Since 2023, the Company’s overseas sales have grown significantly, with the proportion continuously rising. The higher ASP in overseas markets has also driven up the Company’s overall unit revenue year by year. In 2015, the Company’s overseas revenue was RMB3.64 billion, accounting for 12.3%, while in 2024, overseas revenue rose to RMB15.20 billion, accounting for 40.8%.

According to data from the China Bus Statistics Information Network, in H1 2025, China exported 36 thousand large, medium, and light buses, up 29.2% yoy, including 22 thousand large and medium buses, up 16.5% yoy. Meanwhile, exports of new energy buses surged to 8,843 units, up 108.9% yoy, showing strong momentum. Demand for new energy buses in Europe is expected to grow rapidly, while segmented markets such as group buses in the Middle East, city buses in Latin America, and tourist buses in Southeast Asia are still experiencing recovery-driven growth.

In H1 2025, Yutong Bus exported a total of 60,200 thousand units, down 7.38% yoy, mainly due to fluctuations in delivery schedules. While the yoy growth rate in July is expected to turn positive. The Company’s first overseas new energy commercial vehicle plant is being established in Qatar, adopting a KD factory model. It is scheduled for completion and commencement of production by the end of 2025. The plant is initially designed with an annual production capacity of 300 units, expandable to 1,000 units. Looking ahead, with the full recovery of the global economy and international tourism activities, the overseas bus market is expected to continue growing. Currently, the overall penetration rate of overseas new energy buses is only around 10%, leaving significant room for future growth.

Investment Thesis

The Company’s leading position remains solid, with significant economies of scale, mature technology, strong brand recognition, and supply chain advantages. Its performance is expected to sustain steady growth. Yutong has always placed importance on shareholder returns. Since its listing, the Company has maintained a cumulative payout ratio of 77.9%, highlighting its long-term investment value.

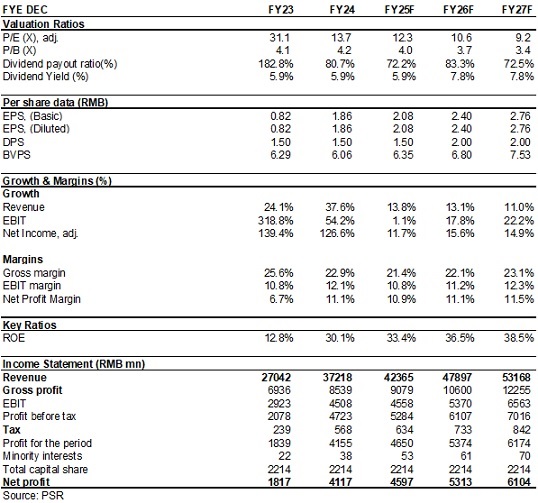

We forecast that the company’s EPS in 2025/2026/2027 will be RMB2.08/2.40/2.76 yuan, our target price is set unchanged at RMB31.3. It is equivalent to a prospective 2025/2026/2027 PE of 15.1/13.0/11.4x respectively. We give “BUY” rating. (Closing price as at 25 July)

Source: Wind, Phillip Securities Hong Kong Research

Risk Factors

1) New energy vehicle development falling short of expectations;

2) Macroeconomic downturn affecting bus demand;

3) Overseas market risks.

Financials

(Closing price as at 25 July)

Download PDF version...