|

MEDTIDE(3880)

Analysis:

MEDTIDE primarily focuses on providing significant Contract Research, Development, and Manufacturing Organization (CRDMO) services, specializing in synthetic peptide production and offering end-to-end services from early discovery, preclinical research, and clinical development to commercial production. Based on 2023 sales revenue, the group is the world’s third-largest peptide-focused CRDMO, with a market share of 1.5%. The group has established an extensive project pipeline, with 1,217 ongoing CRO projects and 332 ongoing CDMO projects as of December 31, 2024. The group’s main services include (i) CRO services, specifically peptide New Chemical Entity (NCE) discovery and synthesis, and (ii) CDMO services, including peptide Chemistry, Manufacturing, and Controls (CMC) development and commercial production. The group primarily focuses on providing Active Pharmaceutical Ingredients (APIs) to clients rather than finished drugs. Clients combine the APIs with excipients to create the final dosage form, determining the appropriate dosage form, delivery route, and formulation for use in clinical trials or commercial sales. The group has established stable customer relationships and service coverage in over 50 countries, including major markets such as China, the United States, Japan, Europe, South Korea, and Australia.According to Frost & Sullivan, the global peptide therapeutics market grew from $60.7 billion in 2018 to $89.5 billion in 2023, with a compound annual growth rate (CAGR) of 8.1%, and is projected to reach $261.2 billion by 2032, with a CAGR of 12.6%. Approximately 70% of the global peptide therapeutics market, driven by pharmaceutical and biotech companies, outsources clinical development and production to third-party service providers, significantly higher than the 30% to 40% for biologics. This reliance on third-party providers has led to rapid growth in the global peptide CRDMO market, which increased from $1.6 billion in 2018 to $3.1 billion in 2023, with a CAGR of 14.8%, and is expected to grow further to $18.8 billion by 2032, with a CAGR of 22%. Currently, 76 non-insulin peptide drugs have received regulatory approval globally. Among them, GLP-1 has become a major driver of the rapid growth in the global peptide therapeutics market. The global GLP-1 market grew from $9.3 billion in 2018 to $38.9 billion in 2023, with a CAGR of 33.2%, and is projected to reach $129.9 billion by 2032, with a CAGR of 14.3%. If semaglutide’s patents in China and the United States expire in 2026 and 2032, respectively, it could lead to an increase in generics, potentially driving higher demand for APIs, as well as CRO and CDMO services for the discovery and development of more advanced NCEs.(I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $34.50, Target Price: $37.50, Cut Loss Price: $33.00

|

SF INTRA-CITY(9699)

Analysis:

The company is China`s leading third-party on-demand delivery service platform, providing all-scenario, end-to-end intra-city delivery solutions. It has become one of the preferred service providers for local lifestyle on-demand delivery, serving 650,000 active merchants (a YoY increase of nearly 40%) and over 23.41 million active consumers. Its business network covers more than 2,300 cities and counties nationwide, catering to diverse on-demand delivery needs across various scenarios. In 2024, the company achieved: Revenue of RMB 15.75 billion, up 27.1% YoY; operating costs of RMB 14.68 billion, up 26.6% YoY; gross profit of RMB 1.07 billion, up 34.8% YoY; gross margin rose to 6.8% – marking seven consecutive years of growth and profitability had been strengthened; net profit attributable to owners of the parent company of RMB 132 million, surging 161.8% YoY. The company continues to deepen collaborations with major traffic platforms, comprehensively serving on-demand needs in live-streaming e-commerce, supermarket hourly delivery, and food delivery. Leveraging its full-scenario advantages, it has upgraded product capabilities for key verticals like bubble tea, supermarkets, and pharmaceuticals, delivering seamless instant retail experiences for commercial clients. Last year, the company integrated AI foundation models from multiple leading domestic providers, driving operational digitization and AI-powered intelligent decision-making across all business segments. With JD.com`s entry into the food delivery market – forming a three-way rivalry with Meituan and Ele.me – major chains (e.g., Luckin Coffee, Sam`s Club) increasingly favor independent third-party delivery to avoid platform lock-in risks. SF Intra-City capitalizes on its neutral positioning, with Key Account (KA) client expansion becoming its core growth driver. SF implements a "courier + autonomous vehicle" hybrid delivery network. By May 2025, its autonomous fleet reached 200 vehicles, covering 38 cities with over 10,000 monthly active routes, significantly boosting operational efficiency. Additionally, the company is actively expanding into lower-tier cities, steadily increasing its coverage in these emerging markets.

Strategy:

Buy-in Price: $16.96, Target Price: $18.94, Cut Loss Price: $15.80

|

|

JIANGXI COPPER (358.HK) - The work plan for stabilizing growth in key industries will be released soon, boosting market sentiment

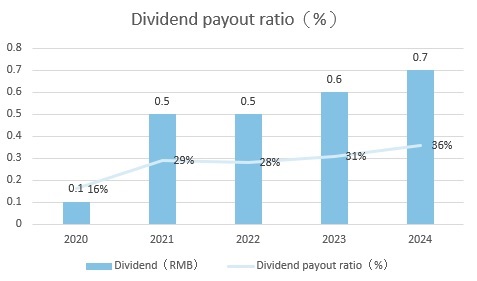

Company ProfileJiangxi Copper is a leading copper producer in China, primarily engaged in copper mining, smelting, processing, and sales. The company boasts abundant copper resource reserves and advanced production technologies. Its products include copper concentrates, copper cathodes, and copper materials, which are widely used in industries such as power, construction, and transportation. Performance HighlightsIn Q1 2025 (According to Chinese accounting standards), the company's revenue was RMB 111.61 billion, down 8.9% year-on-year; net profit attributable to shareholders after deducting non-recurring items was RMB 2.48 billion, up 37.08% year-on-year, mainly due to the fair value changes in financial assets and liabilities and related disposal gains and losses; EPS was RMB 0.57, up 14% year-on-year; net operating cash flow was RMB 558 million, up 109.2% year-on-year, mainly due to the increase in notes payable and accounts payable. In 2024, the company's revenue was RMB 519.25 billion, down 0.21% year-on-year; net profit attributable to shareholders was RMB 6.9 billion, up 2.3% year-on-year; EPS was RMB 2.00, up 2.56% year-on-year; dividend per share was RMB 0.7 in 2024, and the dividend payout ratio has increased for three consecutive years, indicating that the company attaches importance to shareholder returns. Chart 1: Dividend payout ratio

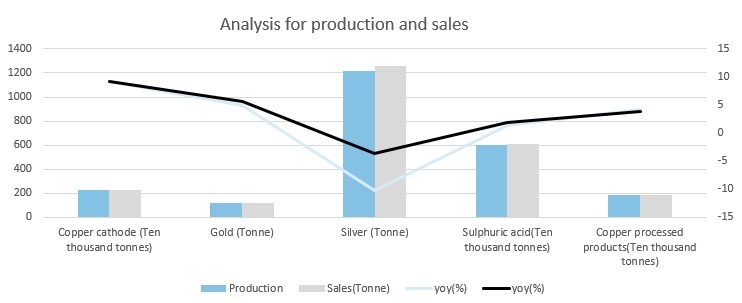

Resources: Annual Report, PSHK Copper and gold production grew steadilyIn 2024, the company's cathode copper production was 2.29 million tonnes with a year-on-year increase of 9.28%, and sales were 2.29 million tonnes with a year-on-year increase of 9.24%; gold production was 118.26 tonnes with a year-on-year increase of 4.99%, and sales were 119.09 tonnes with a year-on-year increase of 5.65%. The company gave guidance on the production and operation plan for 2025: production of 200,000 tonnes of copper concentrate, 2.37 million tonnes of copper cathode, 139 tonnes of gold, 1,243 tonnes of silver, 6.53 million tonnes of sulphuric acid and 2.01 million tonnes of copper processing materials. Chart 2: Analysis for production and sales

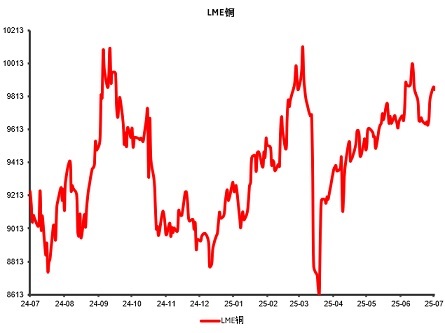

Resources: Annual Report, PSHK The Aynak copper mine project has been restarted, and the company's production capacity is expected to be further expandedThe Mes Aynak copper mine project in Afghanistan, in which the company participated, is a key part of China's overseas resource layout. However, due to factors such as safety and cultural protection, the project has gone through 16 years of twists and turns and was finally restarted in July 2024. The company holds a 25% stake in the project, with MCC Group as the lead party and both parties jointly operating. The Mes Aynak copper mine is the world's second largest undeveloped copper mine, with proven resources of 662 million tonnes, copper metal resources of approximately 11.08 million tonnes, and an average grade of 1.67%. After reaching full production, it is expected to produce 220,000 tonnes of refined copper annually, which is expected to further expand the company's production capacity and alleviate China's copper resource consumption gap. Becoming the largest single shareholder of SolGoldIn March 2025, Jiangxi Copper (Hong Kong) Investment Co., Ltd., a wholly-owned subsidiary of the Company, signed a share purchase agreement with SolGold Canada Inc. ("SolGold Canada"), whereby Jiangxi Copper Hong Kong Investment purchased 157 million shares (approximately 5.24% of its issued shares) of SolGold Plc (SolGold), a listed company in London and Toronto, held by SolGold Canada, for a total transaction price of US$18.07 million. Prior to this transaction, Jiangxi Copper Hong Kong Investment already held 209 million shares of SolGold. After the completion of this transaction, Jiangxi Copper Hong Kong Investment will hold a total of 366 million shares of SolGold (approximately 12.19% of its issued shares). After this transaction, Jiangxi Copper will become the largest single shareholder of SolGold. SolGold is a mineral exploration and development company headquartered in Perth, Australia. The core asset is 100% equity of the Cascabel project in Ecuador. The Alpala mineral deposit, the main project, currently has the following proven, controlled and inferred resources: 12.2 million tonnes of copper, 30.5 million ounces of gold, and 102.3 million ounces of silver, of which the proven and probable reserves are: 3.2 million tonnes of copper, 9.4 million ounces of gold, and 28 million ounces of silver. The project has completed a pre-feasibility study. Sol Gold also has dozens of exploration projects at different stages in Ecuador and other places. Jiangxi Copper said that this transaction is in line with the company's development strategy, which will help enhance the company's industry status and help the two companies complement each other's strengths, develop synergistically and enhance their value. Successful deployment in KazakhstanThe Bakuta Tungsten Mine Project is one of the key projects in the capacity cooperation framework between China and Kazakhstan. The project is jointly funded by Jiangxi Copper Group Co., Ltd., Hengzhao International (Hong Kong) Co., Ltd., and China Railway Construction Corporation Limited. The project company in Kazakhstan is Jetsu Tungsten Industry Co., Ltd. The Bakuta Tungsten Mine has a tungsten ore reserve of about 120 million tonnes. It is designed to adopt open-pit mining with an annual mining scale of 3.3 million tonnes. Two years after it is put into production, the mining scale will be increased to 4.95 million tonnes per year through the use of waste disposal technology. The first phase of the Bakuta Tungsten Mine project is expected to achieve commercial production in Q3 2025, and the second phase of the expansion plan is expected to start in Q1 2027, indicating that the company has successfully laid out in Kazakhstan and has taken a further step in its international layout. Investment ThesisThe International Copper Study Group (ICSG) released its monthly report on June 24th, showing that global copper mine production increased by approximately 2% year-over-year to 7.53 million tonnes in the first four months of 2025, with concentrate production increasing by 2.2%. Global refined copper production increased by approximately 3.2% year-over-year to 9.42 million tonnes, and global apparent refined copper demand increased by approximately 3.3% year-over-year to 9.18 million tonnes, with supply slightly exceeding demand. The ICSG's Global Copper Mine and Refined Copper Market Outlook (2025–2026) report indicates that global refined copper production is projected to grow by 2.9% in 2025 and 1.5% in 2026. Global refined copper consumption is projected to grow by 2.4% in 2025, reaching 28 million tonnes. Global refined copper consumption is projected to reach 28.52 million tonnes in 2026. The global refined copper market is projected to have a surplus of 289,000 tonnes in 2025 and 209,000 tonnes in 2026. We believe that while the refined copper market may experience an oversupply by 2025, demand remains strong. New energy vehicles and home appliance consumption, benefiting from the trade-in policy, will become key growth drivers for global copper consumption. Due to the recent impact of the Sino-US trade war, China has reduced its imports of scrap copper from the United States, which is expected to further increase China's refined copper consumption. The Ministry of Industry and Information Technology recently held a press conference, announcing the implementation of a new round of work plans to stabilize growth in ten key industries, including steel, nonferrous metals, and petrochemicals. This plan aims to promote structural adjustments, optimize supply, and eliminate outdated production capacity in key sectors, boosting market sentiment and potentially supporting copper prices in the short term. Chart 3: Price of LME Copper

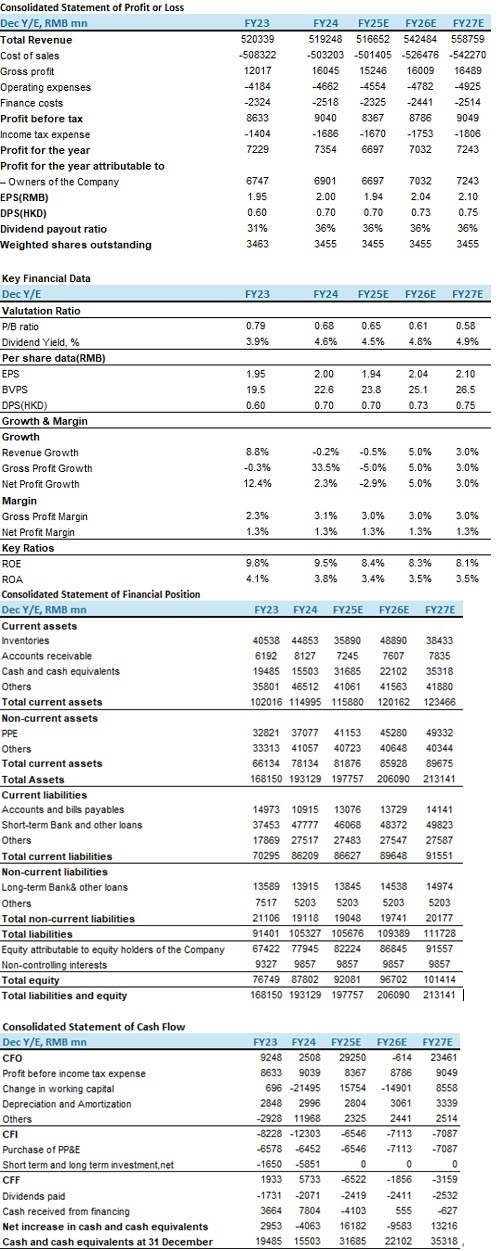

Resources: WIND, PSHK We forecast the company's operating revenue to reach 516.65 billion yuan, 542.48 billion yuan, and 558.76 billion yuan in 2025-2027 respectively. BVPS are 23.8, 25.1, and 26.5 yuan, corresponding to P/B of 0.65x, 0.61x, and 0.58x. We believe the company has medium-term growth potential and assign a target price of HK$18.22 in 2025, corresponding to a P/B of 0.7x. We maintain the “Accumulate" rating. (Current price as of July 29) Risk Factors1) Changes in the macroeconomic environment;

2) Market environment changes;

3) Product price fluctuations;

4) Impact of safety incidents;

5) Exchange rate fluctuations;

6) Product substitution risks;

7) Environmental risks. Financials

Current Price as of: 29 Jul

Source: PSHK Est. Download PDF version...

| Recommendation on 1-8-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 16.800 | | Suggested purchase price | N/A | | Target Price | $ 18.220 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|