|

XTALPI(2228)

Analysis:

XtalPi Holdings primarily engages in providing research and development solutions and services for pharmaceuticals and materials science. By leveraging an AI+robotics model, the company has created a unique industry “flywheel” of “high-throughput experimentation, high-quality data, and high-intelligence models.” Its robotic laboratory platform operates 24/7, rapidly accumulating high-quality data used to train the group’s various AI models. These models are applied in stages such as target identification, virtual screening, synthesis strategy recommendations, prediction of synthesis reaction outcomes, patent searches, and structured data organization. The group is transforming traditional R&D approaches, driving a paradigm shift in pharmaceutical and materials development. Its models currently empower R&D personnel in daily operations, accelerating delivery processes, overcoming bottlenecks in drug discovery and new material molecule development, and significantly expanding the explorable chemical space.

The group recently announced that, as of the end of June 2025, its indirectly wholly-owned subsidiary, Shenzhen XtalPi Technology, entered into a definitive agreement with DoveTree Medicines LLC and its affiliates. Under this agreement, the Group will utilize its end-to-end AI+robotics drug discovery platform to discover and develop small molecule and antibody drug candidates for multiple targets selected by DoveTree, primarily in oncology, immunology and inflammatory diseases, neurological disorders, and metabolic disorders. DoveTree will gain exclusive global development and commercialization rights for these products. The Group has received an upfront payment of US$51 million under the agreement, with the potential for an additional US$49 million in further payments, up to US$5.89 billion in potential regulatory and commercial milestone payments, and royalties in the single-digit percentage range based on the products’ annual net sales.

Earlier, the group completed the acquisition of Liverpool ChiroChem (LCC), further enhancing the capabilities of its AI+robotics intelligent autonomous experimentation platform in chemical space exploration. This strengthens its ability to serve clients in domestic and international drug discovery, new material development, and high-value chemical sectors. Founded in 2014 at the University of Liverpool, LCC has focused on designing and synthesizing novel molecules, particularly new chiral molecules. Its PACE (Parallel Automated Chiral Engine) technology platform integrates AI software with automation, enabling virtual screening of target molecules in a chiral chemical library of hundreds of millions of molecules, followed by efficient synthesis and physical testing with automated equipment. The platform serves multinational pharmaceutical companies and specialized biotech firms across the US, Europe, and Asia. Additionally, LCC has developed comprehensive technical solutions in high-throughput, microscale molecular library construction, complementing the Group’s large-scale molecular library technology.

Strategy:

Buy-in Price: $7.20, Target Price: $8.00, Cut Loss Price: $6.80

|

CHERVON(2285)

Analysis:

The Company is a leading global supplier of electric tools and outdoor power equipment ("OPE"). Its business is divided into OBM and ODM modes. Under the OBM mode, the Company has five brands represented by EGO, and it sells to end consumers through multiple channels such as Lowe's, Wal Mart, ACE Hardware and other large retail chains, professional distributors and e-commerce. In 2020, EGO ranked third among the top 10 global electric OPE brands, and in 2023, EGO ranked first among the mainstream DC OPE brands on North American e-commerce platforms. The company announced a projected increase in performance for the first half of 2025, recording a net profit of 90-100 million US dollars, a year-on-year increase of 46-62%. Faced with tariff risks, the company plans to ship 40% of its products to the North American market from Vietnam by the end of 2025. By 2026, its self built production capacity will basically cover its revenue from the United States, and short-term disturbances will not affect the long-term competitiveness of the company's products.

Strategy:

Buy-in Price: $21.15, Target Price: $24.31, Cut Loss Price: $19.50

|

|

Pop Mart (09992.HK) - Labubu Drives Explosive Growth in Overseas Markets

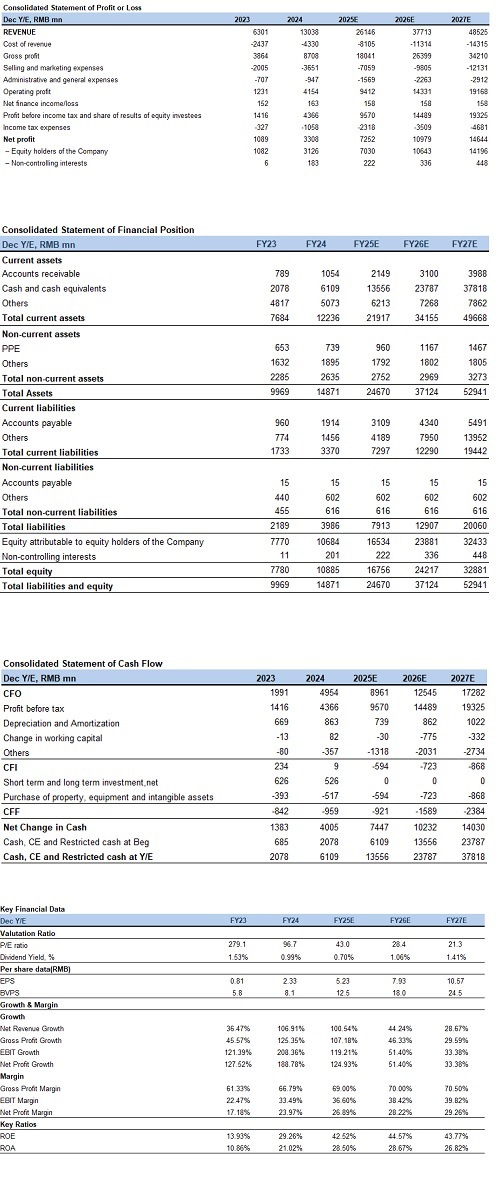

Company BackgroundPOP MART is a leading Chinese trend culture entertainment company, founded in 2010 and headquartered in Beijing. Centered around designer toys, the company has built an integrated operation platform spanning the entire industry chain—covering IP incubation and operation, trendy toy retail, theme parks and experiences, and digital entertainment. POP MART boasts a portfolio of popular IP characters such as Molly, DIMOO, and SKULLPANDA, distributing products through both online and offline channels with a strong following among young consumers. Financial PerformanceIn 2024, the company achieved total revenue of RMB 13.0 billion, representing a 106.9% year-over-year increase. Operating profit surged 237.6% to RMB 4.2 billion, while net profit attributable to shareholders rose 188.8% to RMB 3.1 billion. Gross profit margin expanded by 5.5 percentage points to 66.8%, primarily driven by optimized product mix and higher contribution from overseas high-margin businesses. Geographically, mainland China revenue grew 52.3% to RMB 8.0 billion, with retail stores (RMB 3.8 billion, +43.8%), online sales (RMB 2.7 billion, +76.9%), and robot stores (RMB 700 million, +26.4%) all posting strong growth. Revenue from Hong Kong, Macau, Taiwan and overseas markets soared 375.2% to RMB 5.1 billion, fueled by explosive expansion in retail stores (RMB 2.9 billion, +404.0%) and online channels (RMB 1.5 billion, +834.0%). For the first half of 2025, the company projects revenue growth of no less than 200.0% (implying RMB 13.7 billion) and operating profit growth exceeding 350.0% (RMB 4.3 billion), with net profit margin expected to surpass 30.0%, a historical high. This accelerated performance stems from heightened recognition of the company's IP portfolio, increasing overseas revenue contribution, and sustained cost optimization efforts. Core New IP Launches Propel Explosive Overseas GrowthFollowing the market frenzy driven by its Monster series in Q4 2024, POP MART launched the Labubu 3.0 designer toy series in April 2025. Throughout Q2, Labubu 3.0 continued fueling explosive overseas growth—maintaining Q1's 475%-480% YoY surge—as celebrity endorsements and social media buzz amplified IP popularity, sustaining rapid international revenue expansion. In Q1 2025, North American sales skyrocketed nearly ninefold (895%-900% YoY), while European revenue jumped over sixfold (600%-605% YoY), significantly outpacing Southeast Asia's 345%-350% growth. This validates the company's Western-focused strategy, with management projecting North American sales to match 2020 group-wide levels (RMB 2.5 billion) by year-end. Despite implementing 12%-27% price hikes in North America since mid-April 2025 to offset tariffs, sales momentum remains robust, demonstrating both low consumer price sensitivity and strong pricing power. We believe rising contributions from premium-priced overseas markets will further enhance overall profitability. Accelerated Offline Store ExpansionOn physical retail expansion, 39 new stores opened in H1 2025, with the US (17 stores), Indonesia (6), and Thailand (5) leading the rollout—accelerating POP MART's strategic shift toward offline growth. Strong Online Channel PerformanceDigitally, FastMoss data shows TikTok channel GMV reached RMB 498 million in H1 2025, dominated by the US (RMB 336 million), Thailand (RMB 67 million), and Philippines (RMB 29 million). Overseas Success Fuels Domestic Growth AccelerationLeveraging the global buzz around Labubu 3.0, we project POP MART's domestic sales growth will further accelerate from May-June 2025 (versus April levels), driving Q2 China revenue growth to outpace Q1 (+95%-100% YoY). Investment RecommendationWhile POP MART's flagship IPs typically experience short-term spikes (~2 years) followed by deceleration, we believe the company's integrated operational capabilities—spanning channel management, content development, and product innovation—can sustain value release during IP traffic peaks, transforming "blockbusters" into enduring icons. As a pioneer and leader in trendsetting toys and commercialization, the company leverages its full-industry-chain advantages to develop and monetize IPs across multiple dimensions. Its product category expansion has shown significant results, while overseas business has entered a new phase of accelerated growth. Accordingly, we forecast the company's 2025-2027 revenue at RMB 26.1/37.7/48.5 billion, with net profit attributable to shareholders at RMB 7.0/10.6/14.2 billion, translating to EPS of RMB 5.23/7.93/10.57. Given its high growth potential, we apply a 55x P/E multiple to our 2025 earnings estimate, arriving at a target price of HKD 316. The current share price implies 2025-2027 P/E multiples of 48x/32x/24x, and we assign an "Accumulate" rating. Risk Factors1) Intensifying competition;

2) Slower-than-expected overseas expansion;

3) Deteriorated market demand. Financial Data

(Closing price as of: Aug 7)

Exchange rate: HKD/RMB = 0.91

Source: PSHK Est. Download PDF Version Here...

| Recommendation on 12-8-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 278.800 | | Suggested purchase price | N/A | | Target Price | $ 316.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|