|

ETERNAL BEAUTY(6883)

Analysis:

Eternal Beauty primarily engages in the retail, wholesale, and distribution of perfumes, cosmetics, skincare products, personal care products, eyewear, and home fragrances in China. Unlike brand-owning perfume groups, Eternal Beauty focuses on selling and distributing products sourced from third-party brand licensors, generating revenue from these activities and providing market deployment services, such as brand management and designing and implementing customized market entry and expansion plans for these licensors. Based on 2023 retail sales, the Group is the largest perfume group in China (including Hong Kong and Macau), excluding brand-owning perfume groups.

As of March 31, 2025, the Group’s products are sold in over 400 cities across China (including Hong Kong and Macau) through more than 100 offline points of sale (POS) directly operated by the Group and over 8,000 POS operated by retail customers. Additionally, the Group sells products to offline distributors, who may further resell them to other offline retailers. Beyond offline channels, the Group also sells products online through well-known e-commerce platforms and social media platforms in China.Currently, the Group distributes products and provides market deployment for a total of 72 external brands, including Hermès, Van Cleef & Arpels, Chopard, Albion, and Laura Mercier, covering a diverse range of price points and functions to meet the varied demands of consumers in mainland China, Hong Kong, and Macau. In addition to external brands, the Group owns a proprietary brand, Santa Monica, under which it offers perfumes and eyewear.

The Group’s business and financial performance have maintained growth. Revenue increased from RMB 1.699 billion for the year ended March 31, 2023, to RMB 1.863 billion for the year ended March 31, 2024, and further to RMB 2.083 billion for the year ended March 31, 2025. Similarly, net profit grew from RMB 173 million for the year ended March 31, 2023, to RMB 206 million for the year ended March 31, 2024, and further to RMB 227 million for the year ended March 31, 2025.

The total perfume market size in China (including Hong Kong and Macau), measured by retail sales, grew from RMB 14.6 billion in 2018 to RMB 26.1 billion in 2023, with a compound annual growth rate (CAGR) of approximately 12.3%. It is projected to reach RMB 47.7 billion by 2028, with a CAGR of about 12.8% from 2023 to 2028. The mainland China perfume market grew from RMB 11.4 billion in 2018 to RMB 22.9 billion in 2023, with a CAGR of approximately 15%, and is expected to reach RMB 44.0 billion by 2028, with a CAGR of about 14%.

Strategy:

Buy-in Price: $2.18, Target Price: $2.40, Cut Loss Price: $2.08

|

YUTONG BUS(600066.CH)

Analysis:

Yutong Bus is a leading domestic bus manufacturer. Its products cover various market segments including long-distance coaches, tourist coaches, city buses, staff commuter buses, school buses, sightseeing buses, airport shuttle buses, autonomous microcirculation buses, and special-purpose vehicles, meeting market demands across different vehicle lengths from 5 metres to 18 metres. The company has maintained the number one sales volume of large and medium-sized buses in China for 22 consecutive years. In 2025Q1, Yutong Bus reported revenue of RMB6.42 billion (RMB, the same below), down 3.0% yoy, with net profit attributable to the parent company of RMB755 million, up 14.9% yoy. 25Q1 recorded net cash inflow from operating activities of RMB1.42 billion, maintaining a healthy financial position. According to the Company’s guidance at the beginning of the year, revenue for 2025 is expected to reach RMB42.133 billion, up 13.2% yoy. Operating costs and expenses are planned at RMB37.203 billion, equivalent to operating profit of RMB4.93 billion, up 62.1% yoy, reflecting strong confidence.

Strategy:

Buy-in Price: $27.27, Target Price: $31.50, Cut Loss Price: $25.00

|

|

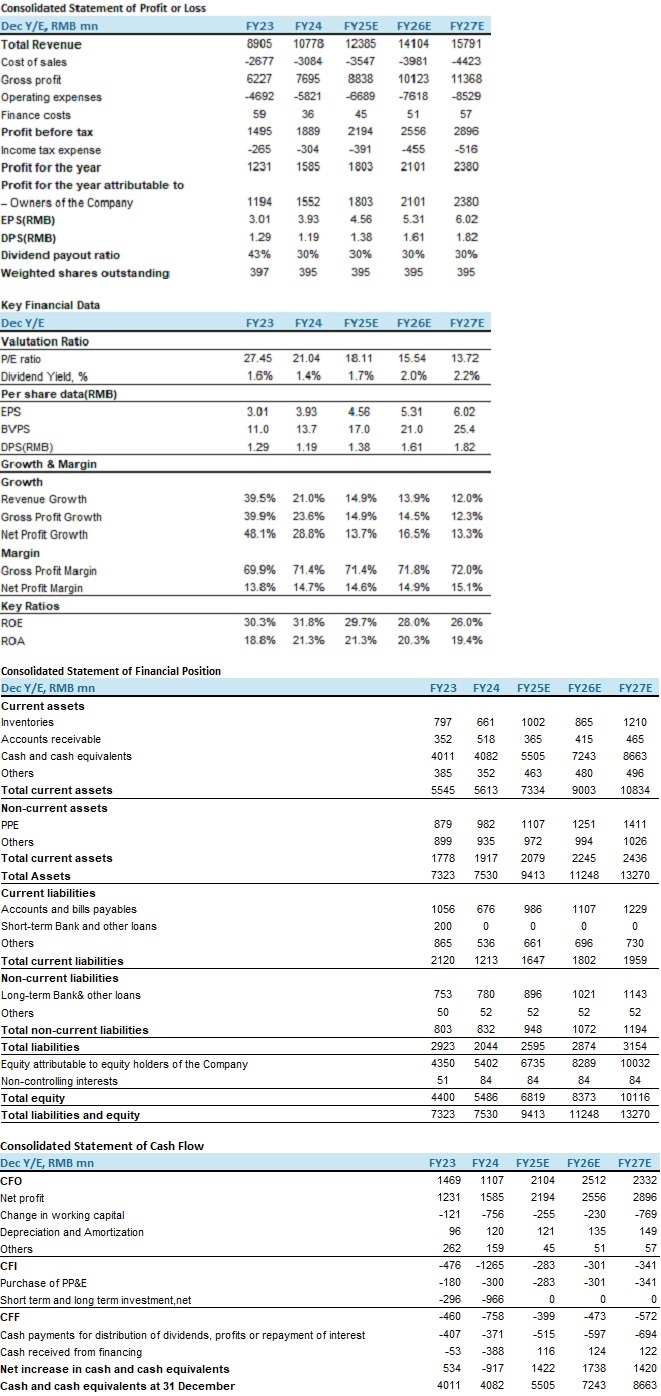

Proya Cosmetics (603605.CH) - Revenue exceeded 10 billion for the first time, and valuation remains attractive

OverviewAs a leading domestic cosmetics company, Proya Cosmetics primarily engages in R&D, production, and sales of cosmetic products. Its offerings span skincare, makeup, cleansing & personal care, and more. The company owns brands such as Proya, Hapsode, Timage, Off&Relax, CORRECTORS, INSBAHA, UZERO and Anya. Performance reviewIn 2024, the company achieved revenue of RMB 10.78 billion with a year-on-year (YoY) increase of 21.04%, surpassing the RMB 10 billion mark for the first time, primarily driven by growth in online channel revenue. Operating costs were RMB 3.08 billion (YoY +15.18%). Selling expenses reached RMB 5.16 billion (YoY +29.93%), mainly due to increased brand promotion and marketing expenses. R&D expenses were RMB 210 million (YoY +21.21%), with an R&D expense ratio of 1.95%, remaining largely flat YoY. Net profit attributable to shareholders was RMB 1.55 billion (YoY +30%). Net cash flow from operating activities was RMB 1.12 billion (YoY -24.6%), primarily due to increased payments for goods, marketing expenses, taxes, and employee compensation. Basic earnings per share (EPS) were RMB 3.93 (YoY +30.56%). In Q1 2025, the company recorded revenue of RMB 2.36 billion (YoY +8.13%). Net profit attributable to shareholders was RMB 390 million (YoY +28.87%). Net cash flow from operating activities was RMB 675 million (YoY +56.78%). Basic EPS was RMB 0.99 (YoY +30.26%). The Q1 revenue growth rate was notably slower than the full-year 2024 growth. We attribute this primarily to Q1 not being the peak season for cosmetics consumption, which is typically concentrated in the summer months (June-August) and during major year-end promotional events (October-December). Outstanding 618 Performance: Topping Platform Brand RankingsAccording to National Bureau of Statistics data, China's total retail sales of consumer goods in H1 2025 reached RMB 2,4545.8 billion (YoY +5%). Retail sales of cosmetics amounted to RMB 229.1 billion (YoY +2.9%), exceeding the H1 2024 growth rate, demonstrating the industry's resilience and sustained upward trend. Data from Qingyan Intelligence shows that the total GMV across four major platforms (Taobao/Tmall, Douyin, JD.com, Kuaishou) during the 2025 618 shopping festival period (May 13 - June 18) reached RMB 65.91 billion with a YoY increase of over 10%. This year, Tmall simplified its promotions, replacing complex tiered discounts with a straightforward ൗ% Official Instant Discount," supplemented by category and general consumption coupons. This approach maintained competitive pricing while avoiding excessive "cutthroat price competition." The company delivered an outstanding 618 performance across its brands:

Proya: Topped multiple platform rankings, including Tmall Beauty (Full Period), Douyin 618 Good Things Festival (Skincare), JD.com Domestic Beauty Brand, and Pinduoduo Domestic Beauty Brand.

Timage: Experienced strong growth across three major platforms, ranking first in Tmall Color Cosmetics, second in JD.com Domestic Color Cosmetics, and fifth in Douyin Domestic Color Cosmetics, with GMV growth 10%+, 20%+, and 30% YoY respectively. Key products like the Little Round Tube Foundation, Primer, Trio Contour Palette, and Trio Concealer topped their categories.

Off&Relax: Achieved over 148%+ YoY growth across all channels, hitting new record high. Tmall dual-store GMV grew over 110%+ YoY, Douyin dual-store GMV surged over 200%+ YoY, and JD.com dual-store GMV jumped over 270%+ YoY. Star products like the OR Anti-Hair Loss Serum, Volumizing Shampoo, and Hair Oil performed exceptionally well.

Hapsode: GMV grew 23.5% YoY on Douyin, 69% on JD.com, and 23% on Pinduoduo.

INSBAHA: Achieved over 106%+ YoY GMV growth across all platforms and is rapidly emerging as one of the company's fastest-growing new brands, poised to contribute significantly to future incremental growth. Strategic Collaboration with Bota Bio: Exploring Synthetic BiologyIn May 2025, Proya signed a strategic cooperation agreement with Bota Bio, marking its first partnership with a synthetic biology enterprise. The collaboration will focus on integrating synthetic biology and AI technologies for the innovative development and application of cosmetics and biomedical aesthetic materials. The partners aim to jointly build an innovation matrix for bio-based functional active ingredients, accelerating breakthroughs and enabling diverse applications in cosmetics and biomedical materials. This will provide consumers with more effective, green, and safe products. The collaboration is expected to enhance Proya's competitiveness in bio-based ingredient innovation, product technology barrier creation, and sustainability. Strategic Partnership with Ant Group: AI Empowering BeautyIn May 2025, Proya entered a strategic partnership with Ant Group's Beijing Digital Mali Technology Co., Ltd. Beijing Digital Mali Technology will assist Proya in enhancing consumer experience through AI-powered cloud customer service, AI smart inspection, and full-chain user experience solutions. It will also leverage AI to boost Proya's competitiveness in enterprise digital operations, energy conservation, emission reduction, and green initiatives. This collaboration is a key step in Proya's digital transformation, aiming for short-term cost reduction and efficiency gains through AI customer service and smart quality inspection, better supporting operational stability during peak sales seasons. Partnership with Top-Tier Hospital: Collaborative R&D on Mitochondrial Anti-AgingIn July 2025, the company signed an agreement with West China Hospital of Sichuan University focusing on "mitochondrial anti-aging" research. This aims to leverage cutting-edge medical research to empower cosmetic innovation, establishing a full-chain "industry-academia-research-medicine" collaborative model. Mitochondrial research is becoming a crucial frontier in tech-driven anti-aging. The partnership will integrate West China Hospital's advanced research resources to deeply investigate the intrinsic link between mitochondrial function and skin aging at the cellular level, identify key pathways and targets, accelerate R&D and screening of potent anti-aging actives, and lay a solid foundation for future product applications. However, mitochondrial anti-aging research involves complex biological mechanisms, and the path from basic research to marketable products is lengthy, carrying risks of delayed or unsuccessful technology translation. Valuation and Investment RecommendationThe competitive landscape of the beauty industry is undergoing a reshuffle. Only brands with strong product competitiveness and adept platform resource utilization will thrive. Proya possesses robust product innovation and channel operation capabilities within the domestic beauty sector. Its consistent execution of the "hot product strategy" and continuous portfolio enrichment solidify its leadership position. We anticipate the company will gradually transition from high growth to a more stable phase, but double-digit revenue growth is still expected in the near term.

We forecast the company's operating revenue for 2025-2027 at RMB 12.39 billion, RMB 14.10 billion, and RMB 15.79 billion, respectively. EPS is projected at RMB 4.56, RMB 5.31, and RMB 6.02 for 2025-2027. This translates to P/E ratios of 18.11x, 15.54x, and 13.72x for 2025-2027. We assign a target price of RMB 114, representing 25x our projected 2025 P/E, and maintain a "Buy" rating. Risk Factors1) Downward macroeconomic situation;

2) Intensified industry competition;

3) Management changes;

4) New product promotion failing to meet expectations. Financial Data

Current Price as of: 11 Aug 2025

Source: PSHK Est. Download PDF Version Here...

| Recommendation on 13-8-2025 | | Recommendation | Buy | | Price on Recommendation Date | $ 82.580 | | Suggested purchase price | N/A | | Target Price | $ 114.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|