|

ANGELALIGN(6699)

Analysis:

Angelalign Technology primarily focuses on providing digital orthodontic solutions, driven by a dual-engine strategy of “digitalization and globalization.” In the Chinese market, the group strategically expands its sales and clinical medical teams based on the developmental characteristics of different city tiers. It offers medical service support to various types of dental professionals, including case diagnosis assistance, 3D treatment plan interpretation, and follow-up monitoring recommendations, ensuring the quality of each case. The group’s medical design and customer service teams have upgraded to a “7×12-hour” service model to promptly address user needs. In 2024, the group achieved approximately 218,700 clear aligner case shipments in China, maintaining its leading market position. In global markets outside China, the group emphasizes enhancing doctors’ user experience, maintaining high-quality medical design support, and ensuring stable delivery cycles. In 2024, it achieved about 140,700 clear aligner case shipments globally, spanning over 50 countries.

In terms of products, in the field of early-stage orthodontic treatment, the group promotes the concept of “Teeth-bone-muscle Three-in-one Solution” and abide by the principles of “age-based treatment” and “symptom-specific treatment”. It focuses on comprehensive oral health management for children and adolescents, driving rapid growth in its “children’s edition” product line. In the field of adult orthodontic treatment, the group prioritizes correction efficiency and effectiveness, offering high-quality treatment plans and medical services. Technologically, the group leverages computer technology to advance digital orthodontics, from initial patient consultations and assisted diagnoses to treatment planning, production, and process monitoring. In the first half of last year, it launched a series of digital tools to enhance dentists’ diagnostic capabilities, including iSmile Maker, iDiagnose, Live Now, Movement Evaluation and Progress Analysis. In the second half, it introduced new treatment plan design features, such as Flexible Virtual Jump, Modify Passive Aligners, Enter Figures to Modify Tooth, angelButton Collision Detection and Auto Save. These tools help dentists comprehensively review and modify cases, optimizing workflows. In January this year, the international version of the iOrtho App was officially launched, retaining standard features like case submission and management, 3D treatment planning review and approval, and introducing new mobile-terminal functionalities, including portrait and intraoral photograph and local upload of intraoral scans and CBCT data.

The group will announce its interim results on August 25 (next Monday). It previously issued a profit alert, expecting net profit for the first half of this year to range from approximately USD 13.4 million to USD 14.8 million, a 538% to 604% increase compared to approximately USD 2.1 million in the same period of 2024. This is primarily due to strategic price adjustments in its core China business to address intense competition, sustained revenue growth outside China, delayed progress in establishing overseas production facilities leading to lower investment and operating expenses in the first half of 2025, and a low profit base in the first half of 2024.(I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $68.00, Target Price: $74.00, Cut Loss Price: $65.00

|

ZTE(763)

Analysis:

In Q1 2025, the company reported operating revenue of RMB32.97 billion with a year-on-year increase of 7.82%. Net profit attributable to shareholders was RMB2.45 billion, down 10.5% YoY. Net cash flow from operating activities amounted to RMB1.85 billion with a decrease of 37.93% YoY. EPS stood at RMB0.51, declining by 10.53% YoY.

Amid the ongoing global surge in AI infrastructure development, demand for AI data center (AIDC) supporting facilities has risen significantly. Analysis indicates that next-generation computing power chips consume substantially more power, driving higher requirements for data center power systems and liquid cooling technologies. Domestic power supply, liquid cooling, and energy storage enterprises are poised to benefit substantially, with strong expectations for order growth. To capture opportunities presented by large-scale AI models, ZTE has intensified R&D in foundational AI computing products and launched a full-stack, full-scenario intelligent computing solution. For data centers, the company is building comprehensive full-stack solutions and end-to-end delivery capabilities tailored for AI computing scenarios. Innovations include a full suite of self-developed liquid cooling products—such as immersion cooling, cold plate cooling, External Cooling Exchange Units (EDU), and blind-mate cabinets—alongside modular Air Handling Units (AHU) and integrated power modules. These advancements are expected to unlock new growth potential.

Strategy:

Buy-in Price: $28.50, Target Price: $31.78, Cut Loss Price: $26.94

|

|

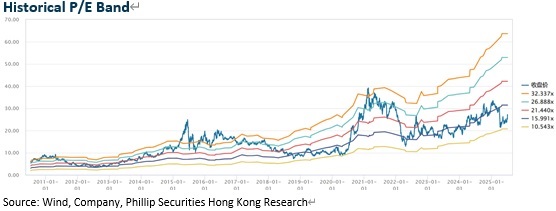

Great Star Industrial (002444.CH) - Breakthrough in Power Tools

Company profileThe Company was established in 1993, starting with OEM of hand tools. In 2009, it launched its first proprietary brand, Workpro, and began transitioning from original design manufacturer (ODM) to original brand manufacturer (OBM). At the same time, it continued overseas acquisitions to expand its brand portfolio, driving continuous growth in scale. Currently, the Company's products are mainly targeted at Europe and the United States. In 2024, overseas revenue accounted for 95%. Its products mainly include hand tools, power tools and industrial tools, with revenue of RMB10.07 billion (RMB, the same below), RMB1.44 billion and RMB3.23 billion, respectively. Among them, OBM and ODM revenue accounted for 47.92% and 51.67%. Investment SummarySteady Growth in Results

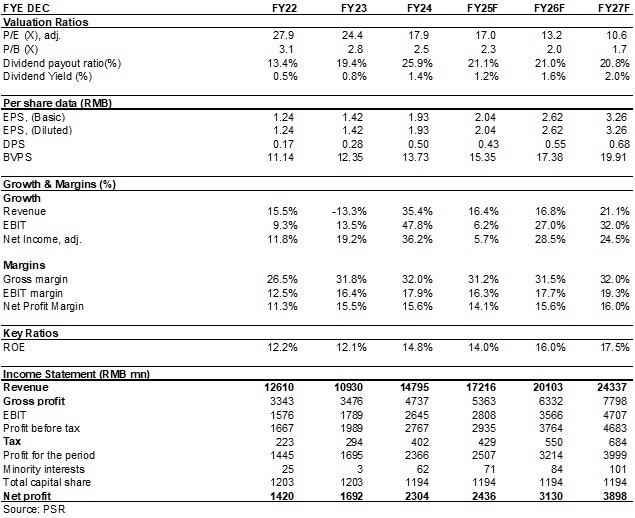

In 2024, the Company achieved revenue of approximately RMB14.80 billion, up 35.37% yoy; net profit attributable to the parent company of RMB2.30 billion, up 36.18% yoy; and a gross margin of 32.01%. Over the past five years since 2019, revenue and net profit have recorded an average growth rate of 17.5% and 20.6%, respectively.

On July 10, the Company issued a result forecast, expecting H1 2025 net profit attributable to the parent company to be RMB1.25-1.37 billion, representing an estimated increase of 5%-15%; net profit attributable to the parent company excluding non-recurring items is expected to be RMB1.27-1.39 billion, up approximately 5%-15%, equivalent to a Q2 net profit attributable to the parent company growth midpoint of 9.2%, better than market expectations.

Although U.S. tariffs negatively impacted production capacity utilization for approximately 40 days in Q2, affecting order delivery and revenue, it is expected that Q2 revenue compared with the same period last year remained almost the same. However, the Company improved its gross margin through cross-border e-commerce sales and increased sales of new products, particularly power tools. As a result, Q2 net profit attributable to the parent company is expected to grow, demonstrating strong growth potential. Breakthrough in Power Tools

According to Frost & Sullivan, from 2022 to 2026, the global CAGR for power tools will exceed 6%, while the CAGR for hand tools will be 3%-4%, with powered products significantly outperforming non-powered ones. Since 2021, the Company has positioned power tools as a strategic business, and in 2024 achieved breakthroughs in 20V lithium battery tools in mainstream markets. It subsequently announced two major international retail customer orders for lithium battery power tools and related accessories, with total annual procurement values equivalent to no less than USD30 million and USD15 million, respectively. Notably, the first order required production and delivery in Vietnam for the U.S. market, marking the Company's first power tool order produced and delivered outside China, and validating its global supply capabilities with top-tier clients. The second order, from Europe, marked the Company's debut in the European power tools market. Global Capacity Layout to Respond Quickly to Market DemandSince 2018, the Company has accelerated its overseas capacity layout through self-built plants in Southeast Asia and acquisitions in Europe and the U.S. Currently, it operates 23 production bases worldwide, including 11 in China, 3 in Southeast Asia, 6 in Europe, and 3 in the U.S. The global supply chain system not only improves responsiveness to sudden market demands but also strengthens resilience against global trade barriers. In Q2 2025, due to the impact of the U.S. "Reciprocal Tariffs" policy, production capacity was restricted for about 40 days, significantly affecting order delivery and revenue. However, with the Vietnam production base, the Company partially avoided tariff risks. Now, the third phase of the Vietnam base is already in operation, and the fourth phase is under construction, with full coverage of Southeast Asia's shipments to the U.S. expected by the end of 2025. This arrangement reduces cost pressures from China-U.S. trade frictions and lays a solid foundation for future growth. In addition, the 20% tariff agreement between Vietnam and the U.S., which is lower than China's export tariff to the U.S., will help further consolidate the Company's competitiveness in global markets. Investment ThesisThe Company's revenue is concentrated in Europe and the U.S., and in the future, it will leverage capacity relocation to establish a complete trade chain of "R&D in China -- Manufacturing in Southeast Asia -- Sales in Europe and the U.S." We are optimistic about the long-term development of the Company and expect EPS to be 2.04/2.62/3.26 yuan respectively for 2025/2026/2027. We offer a target price of 39.4 yuan, respectively 19.3/15/12.1x P/E for 2025/2026/2027, and an "Accumulate" rating.

Risk Factors1) Progress of new production line is below expectations;

2) Electric power tools sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financial Data

(Closing price as at 14 August 2025) Download PDF Version Here...

| Recommendation on 19-8-2025 | | Recommendation | Accumulate (Initiation) | | Price on Recommendation Date | $ 34.620 | | Suggested purchase price | N/A | | Target Price | $ 39.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|