|

TONGCHENGTRAVEL(780)

Analysis:

Tongcheng Travel announced its second-quarter results for 2025. During this period, China’s tourism industry maintained strong growth momentum, with increasing demand for experiential travel as younger tourists sought unique, immersive experiences both domestically and internationally. Despite a dynamic market environment, the group leveraged deep user insights and continuously optimized products and services to swiftly seize new opportunities. As a one-stop platform, the group provides comprehensive travel-related products and services. As of June 30, 2025, its online platform offered over 475,000 flight routes operated by more than 770 domestic and international airlines and agents, over 4.1 million hotel and non-standard accommodation options worldwide, approximately 160,000 bus routes, more than 880 ferry routes, and ticket services for over 10,000 tourist attractions. By offering a wide range of travel products and effective user engagement strategies, the group achieved sustained growth in both its user base and user value. In the second quarter, the group’s average monthly paying users grew 9.2% year-on-year to 46.4 million.

The group reported revenue of RMB 4.669 billion for the second quarter, a 10% increase from the second quarter of 2024. Adjusted EBITDA rose 29.7% to RMB 1.185 billion, with the adjusted EBITDA margin improving from 21.5% in Q2 2024 to 25.4% in Q2 2025. By business segment, accommodation revenue grew 15.2% to RMB 1.371 billion. The group actively tapped into emerging accommodation booking scenarios such as weekend getaways, concerts, and sports events, driving average daily room nights to a record high. Additionally, by focusing on high-value users and expanding in lower-tier cities, the group further increased its market share and competitiveness in these regions. In the international hotel business, efforts were made to deepen partnerships with global suppliers and strengthen operations in popular outbound travel destinations for Chinese tourists.

Transportation ticketing services revenue rose 7.9% to RMB 1.881 billion, primarily driven by an enriched supply of value-added products and services. Other business revenue surged 27.5% to RMB 755 million, propelled by strong performance in hotel management services. The group’s asset-light hotel management business continued to expand its coverage in China, with over 2,700 hotels in operation under its platform by the end of June 2025, and an additional 1,500 hotels in the pipeline. However, the vacation business was impacted by safety concerns in Southeast Asia, resulting in an 8% revenue decline to RMB 661 million. Looking ahead, the group will continue to focus on its core online travel platform business, striving to enhance market share and brand influence. While consolidating its position in the domestic market, it will vigorously promote outbound travel to boost its international presence and strengthen its hotel management business to increase its influence in the tourism industry chain.(I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $21.00, Target Price: $23.20, Cut Loss Price: $20.00

|

POP MART(9992)

Analysis:

Pop Mart announced its financial results for the first half of 2025, with revenue reaching RMB 13.876 billion (Chinese yuan, same below), a year-on-year increase of 204.4%; net profit attributable to owners of the parent company was RMB 4.574 billion, up 396.5% year-on-year; EPS was RMB 3.44, representing a growth of 395.3% compared to the same period last year. In the first half of 2025, a total of 13 artist IPs generated revenue exceeding RMB 100 million, with THE MONSTERS, MOLLY, SKULLPANDA, CRYBABY, and DIMOO achieving revenues of RMB 4.814 billion, RMB 1.357 billion, RMB 1.221 billion, RMB 1.218 billion, and RMB 1.105 billion, respectively, during the reporting period. LABUBU, with its unique style and appeal, has entered the ranks of world-class IPs, becoming one of the most popular IPs globally in the first half of 2025. Revenue from plush products reached RMB 6.1392 billion, a year-on-year increase of 1,276.2%, accounting for 44.2% of total revenue.

Strategy:

Buy-in Price: $308.00, Target Price: $340.00, Cut Loss Price: $287.00

|

|

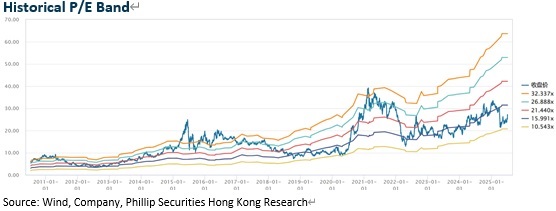

Great Star Industrial (002444.CH) - Breakthrough in Power Tools

Company profileThe Company was established in 1993, starting with OEM of hand tools. In 2009, it launched its first proprietary brand, Workpro, and began transitioning from original design manufacturer (ODM) to original brand manufacturer (OBM). At the same time, it continued overseas acquisitions to expand its brand portfolio, driving continuous growth in scale. Currently, the Company's products are mainly targeted at Europe and the United States. In 2024, overseas revenue accounted for 95%. Its products mainly include hand tools, power tools and industrial tools, with revenue of RMB10.07 billion (RMB, the same below), RMB1.44 billion and RMB3.23 billion, respectively. Among them, OBM and ODM revenue accounted for 47.92% and 51.67%. Investment SummarySteady Growth in Results

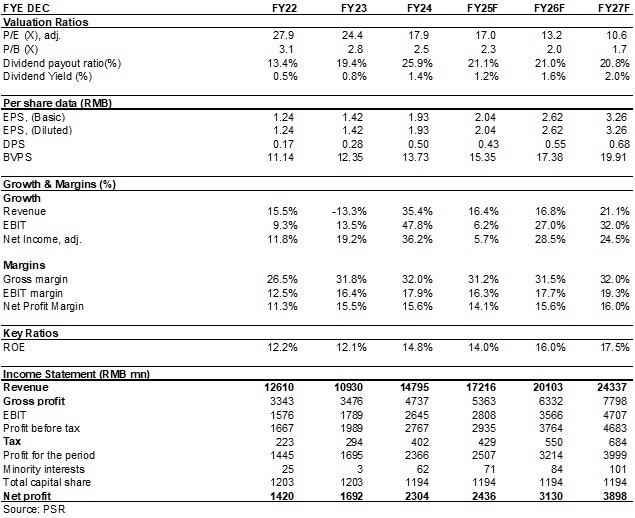

In 2024, the Company achieved revenue of approximately RMB14.80 billion, up 35.37% yoy; net profit attributable to the parent company of RMB2.30 billion, up 36.18% yoy; and a gross margin of 32.01%. Over the past five years since 2019, revenue and net profit have recorded an average growth rate of 17.5% and 20.6%, respectively.

On July 10, the Company issued a result forecast, expecting H1 2025 net profit attributable to the parent company to be RMB1.25-1.37 billion, representing an estimated increase of 5%-15%; net profit attributable to the parent company excluding non-recurring items is expected to be RMB1.27-1.39 billion, up approximately 5%-15%, equivalent to a Q2 net profit attributable to the parent company growth midpoint of 9.2%, better than market expectations.

Although U.S. tariffs negatively impacted production capacity utilization for approximately 40 days in Q2, affecting order delivery and revenue, it is expected that Q2 revenue compared with the same period last year remained almost the same. However, the Company improved its gross margin through cross-border e-commerce sales and increased sales of new products, particularly power tools. As a result, Q2 net profit attributable to the parent company is expected to grow, demonstrating strong growth potential. Breakthrough in Power Tools

According to Frost & Sullivan, from 2022 to 2026, the global CAGR for power tools will exceed 6%, while the CAGR for hand tools will be 3%-4%, with powered products significantly outperforming non-powered ones. Since 2021, the Company has positioned power tools as a strategic business, and in 2024 achieved breakthroughs in 20V lithium battery tools in mainstream markets. It subsequently announced two major international retail customer orders for lithium battery power tools and related accessories, with total annual procurement values equivalent to no less than USD30 million and USD15 million, respectively. Notably, the first order required production and delivery in Vietnam for the U.S. market, marking the Company's first power tool order produced and delivered outside China, and validating its global supply capabilities with top-tier clients. The second order, from Europe, marked the Company's debut in the European power tools market. Global Capacity Layout to Respond Quickly to Market DemandSince 2018, the Company has accelerated its overseas capacity layout through self-built plants in Southeast Asia and acquisitions in Europe and the U.S. Currently, it operates 23 production bases worldwide, including 11 in China, 3 in Southeast Asia, 6 in Europe, and 3 in the U.S. The global supply chain system not only improves responsiveness to sudden market demands but also strengthens resilience against global trade barriers. In Q2 2025, due to the impact of the U.S. "Reciprocal Tariffs" policy, production capacity was restricted for about 40 days, significantly affecting order delivery and revenue. However, with the Vietnam production base, the Company partially avoided tariff risks. Now, the third phase of the Vietnam base is already in operation, and the fourth phase is under construction, with full coverage of Southeast Asia's shipments to the U.S. expected by the end of 2025. This arrangement reduces cost pressures from China-U.S. trade frictions and lays a solid foundation for future growth. In addition, the 20% tariff agreement between Vietnam and the U.S., which is lower than China's export tariff to the U.S., will help further consolidate the Company's competitiveness in global markets. Investment ThesisThe Company's revenue is concentrated in Europe and the U.S., and in the future, it will leverage capacity relocation to establish a complete trade chain of "R&D in China -- Manufacturing in Southeast Asia -- Sales in Europe and the U.S." We are optimistic about the long-term development of the Company and expect EPS to be 2.04/2.62/3.26 yuan respectively for 2025/2026/2027. We offer a target price of 39.4 yuan, respectively 19.3/15/12.1x P/E for 2025/2026/2027, and an "Accumulate" rating.

Risk Factors1) Progress of new production line is below expectations;

2) Electric power tools sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financial Data

(Closing price as at 14 August 2025) Download PDF Version Here...

| Recommendation on 21-8-2025 | | Recommendation | Accumulate (Initiation) | | Price on Recommendation Date | $ 34.620 | | Suggested purchase price | N/A | | Target Price | $ 39.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|