|

HWORLD-S(1179)

Analysis:

H World Group announced its Q2 2025 results, with revenue up 4.5% year-on-year to RMB 6.4 billion, near the upper end of its prior guidance of 1% to 5% growth compared to Q2 2024. Managed and franchised revenue rose 22.8% to RMB 2.9 billion, exceeding the upper end of the 18% to 22% growth guidance. Revenue from the Legacy-Huazhu segment was RMB 5.1 billion, up 5.7%, above the midpoint of the 3% to 7% growth guidance. Revenue from the Legacy-DH segment was RMB 1.3 billion, up 0.1%.

As of June 30, 2025, the group operated 12,137 hotels (1,184,915 rooms). Q2 hotel turnover grew 15% to RMB 26.9 billion. Excluding Legacy-DH, hotel turnover increased 15.6%, while Legacy-DH’s turnover grew 8.9%. Net profit attributable to shareholders was RMB 1.5 billion, up 36.4% year-on-year and 67.8% quarter-on-quarter. Q2 EBITDA (non-GAAP) was RMB 2.5 billion, up 31.6% year-on-year and 56.3% quarter-on-quarter. Operating profit margin was 27.8%, up 2.2 percentage points from 25.6% in Q2 2024, driven by higher contributions from managed and franchised operations, aligning with the group’s asset-light expansion strategy. The board declared a cash dividend of approximately USD 250 million, or USD 0.081 per share.

In Q2, the group opened 595 hotels and is on track to meet its 2025 target of opening 2,300 hotels. It will continue to enhance hotel operations, focus on cost reduction and efficiency, and expand its asset-light portfolio. For Q3 2025, H World Group expects revenue growth of 2% to 6% compared to Q3 2024, or 4% to 8% excluding DH. Managed and franchised revenue is expected to grow 20% to 24% in Q3 2025. (I holds no shares in the mentioned stock.)

Strategy:

Buy-in Price: $27.50, Target Price: $30.00, Cut Loss Price: $26.00

|

PEGBIO CO-B(2565)

Analysis:

The State Council has in principle approved the "China (Jiangsu) Pilot Free Trade Zone Biopharmaceutical Full Industry Chain Open Innovation Development Plan," emphasizing the need to pioneer integrated exploration, promote open innovation across the entire biopharmaceutical industry chain, and drive gains in the pharmaceutical sector. As an innovative pharmaceutical company focused on metabolic diseases, PegBio's investment value hinges on the commercialization progress of its core product, PB-119. The company has an early presence in the GLP-1 drug development landscape. It expects PB-119 to receive NDA approval and enter the commercialization phase in China by 2025, which would likely lead to profitability. Additionally, the company has completed a Phase II clinical trial for PB-119 targeting type 2 diabetes mellitus (T2DM) in the United States. We believe that, benefiting from policy support and earnings expectations driving valuation recovery, pharmaceutical stocks still have room for short-term gains.

Strategy:

Buy-in Price: $33.40, Target Price: $37.00, Cut Loss Price: $31.80

|

|

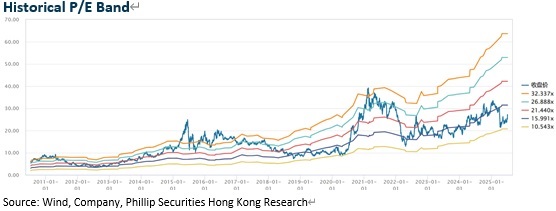

Great Star Industrial (002444.CH) - Breakthrough in Power Tools

Company profileThe Company was established in 1993, starting with OEM of hand tools. In 2009, it launched its first proprietary brand, Workpro, and began transitioning from original design manufacturer (ODM) to original brand manufacturer (OBM). At the same time, it continued overseas acquisitions to expand its brand portfolio, driving continuous growth in scale. Currently, the Company's products are mainly targeted at Europe and the United States. In 2024, overseas revenue accounted for 95%. Its products mainly include hand tools, power tools and industrial tools, with revenue of RMB10.07 billion (RMB, the same below), RMB1.44 billion and RMB3.23 billion, respectively. Among them, OBM and ODM revenue accounted for 47.92% and 51.67%. Investment SummarySteady Growth in Results

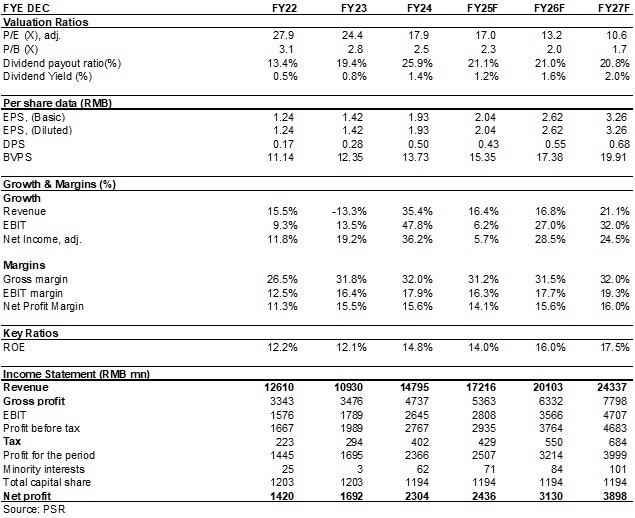

In 2024, the Company achieved revenue of approximately RMB14.80 billion, up 35.37% yoy; net profit attributable to the parent company of RMB2.30 billion, up 36.18% yoy; and a gross margin of 32.01%. Over the past five years since 2019, revenue and net profit have recorded an average growth rate of 17.5% and 20.6%, respectively.

On July 10, the Company issued a result forecast, expecting H1 2025 net profit attributable to the parent company to be RMB1.25-1.37 billion, representing an estimated increase of 5%-15%; net profit attributable to the parent company excluding non-recurring items is expected to be RMB1.27-1.39 billion, up approximately 5%-15%, equivalent to a Q2 net profit attributable to the parent company growth midpoint of 9.2%, better than market expectations.

Although U.S. tariffs negatively impacted production capacity utilization for approximately 40 days in Q2, affecting order delivery and revenue, it is expected that Q2 revenue compared with the same period last year remained almost the same. However, the Company improved its gross margin through cross-border e-commerce sales and increased sales of new products, particularly power tools. As a result, Q2 net profit attributable to the parent company is expected to grow, demonstrating strong growth potential. Breakthrough in Power Tools

According to Frost & Sullivan, from 2022 to 2026, the global CAGR for power tools will exceed 6%, while the CAGR for hand tools will be 3%-4%, with powered products significantly outperforming non-powered ones. Since 2021, the Company has positioned power tools as a strategic business, and in 2024 achieved breakthroughs in 20V lithium battery tools in mainstream markets. It subsequently announced two major international retail customer orders for lithium battery power tools and related accessories, with total annual procurement values equivalent to no less than USD30 million and USD15 million, respectively. Notably, the first order required production and delivery in Vietnam for the U.S. market, marking the Company's first power tool order produced and delivered outside China, and validating its global supply capabilities with top-tier clients. The second order, from Europe, marked the Company's debut in the European power tools market. Global Capacity Layout to Respond Quickly to Market DemandSince 2018, the Company has accelerated its overseas capacity layout through self-built plants in Southeast Asia and acquisitions in Europe and the U.S. Currently, it operates 23 production bases worldwide, including 11 in China, 3 in Southeast Asia, 6 in Europe, and 3 in the U.S. The global supply chain system not only improves responsiveness to sudden market demands but also strengthens resilience against global trade barriers. In Q2 2025, due to the impact of the U.S. "Reciprocal Tariffs" policy, production capacity was restricted for about 40 days, significantly affecting order delivery and revenue. However, with the Vietnam production base, the Company partially avoided tariff risks. Now, the third phase of the Vietnam base is already in operation, and the fourth phase is under construction, with full coverage of Southeast Asia's shipments to the U.S. expected by the end of 2025. This arrangement reduces cost pressures from China-U.S. trade frictions and lays a solid foundation for future growth. In addition, the 20% tariff agreement between Vietnam and the U.S., which is lower than China's export tariff to the U.S., will help further consolidate the Company's competitiveness in global markets. Investment ThesisThe Company's revenue is concentrated in Europe and the U.S., and in the future, it will leverage capacity relocation to establish a complete trade chain of "R&D in China -- Manufacturing in Southeast Asia -- Sales in Europe and the U.S." We are optimistic about the long-term development of the Company and expect EPS to be 2.04/2.62/3.26 yuan respectively for 2025/2026/2027. We offer a target price of 39.4 yuan, respectively 19.3/15/12.1x P/E for 2025/2026/2027, and an "Accumulate" rating.

Risk Factors1) Progress of new production line is below expectations;

2) Electric power tools sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financial Data

(Closing price as at 14 August 2025) Download PDF Version Here...

| Recommendation on 25-8-2025 | | Recommendation | Accumulate (Initiation) | | Price on Recommendation Date | $ 34.620 | | Suggested purchase price | N/A | | Target Price | $ 39.400 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|