|

IMMUNOTECH-B(6978)

Analysis:

IMMUNOTECH is a biopharmaceutical company focused on the research, development, and commercialization of T-cell immunotherapy. Its Core Product Candidate, EAL, is a multi-target cellular immunotherapy with over ten years of clinical application history, showing therapeutic effects against various cancers. Research on EAL began in 2006, during which the company refined cell culture systems and methods, developing a proprietary technology platform with independent intellectual property rights for producing EAL cells.EAL is a broad-spectrum anti-tumor cellular immunotherapy derived from T-cells extracted from a patient’s peripheral blood, which are then activated and expanded using the company’s patented methods. Following discussions with the Center for Drug Evaluation (CDE), in February 2025, the CDE permitted IMMUNOTECH to submit an application for EAL’s conditional approval. In March 2025, EAL was included in China’s priority review and approval list, and its conditional New Drug Application (NDA) is currently under review by the National Medical Products Administration’s CDE.The company operates a research and production center in Beijing, covering approximately 27,604 square meters, which includes a quality testing building and cleanroom laboratories. These facilities support the preclinical and clinical development of cellular immunotherapy products and are equipped to handle early-stage production needs following regulatory approval. All facilities have received cleanroom inspection reports from the Beijing Institute for Drug Control. To address EAL’s six-hour transportation radius, IMMUNOTECH plans to establish additional R&D and production centers in densely populated regions of China to accelerate clinical trials and meet future commercialization demands.In addition to advancing EAL’s commercialization, IMMUNOTECH is committed to investing in its CAR-T and TCR-T cell product pipelines and enhancing its technology platform to develop new cellular immunotherapies tailored to different tumor types and stages, as well as improving the efficacy of existing treatments. Alongside organic growth, the company aims to expand strategic partnerships, pursue sales, technology transfers, and collaborations for its existing and pipeline products. IMMUNOTECH will also explore new development opportunities in cellular immunotherapy, including potential mergers, acquisitions, and strategic cooperation. (I do not hold the aforementioned stock)

Strategy:

Buy-in Price: $5.00, Target Price: $5.45, Cut Loss Price: $4.75

|

WEIMOB INC(2013)

Analysis:

On the news front, recently, Weimob Group announced its interim performance for 2025, with revenue of approximately RMB 775.5 million, representing a year-on-year increase of 7.8%. Adjusted revenue was also approximately RMB 775.5 million. Gross profit was about RMB 582 million, up 1.1% year-on-year, while adjusted gross profit reached approximately RMB 583 million, a significant increase of 36.1% year-on-year. Adjusted net profit was RMB 16.9 million, marking the first profit turnaround since 2021. According to the announcement, the company has continuously refined and iterated its AI products, helping merchants achieve full-process intelligence from store setup and operational management to marketing deployment. It has launched an AI product matrix including WAI SaaS, WAI Pro, and WIME to intelligently enhance efficiency for merchants. In the first half of 2025, revenue from AI products amounted to approximately RMB 34 million.

Strategy:

Buy-in Price: $2.75, Target Price: $3.03, Cut Loss Price: $2.49

|

|

Geely (175.HK) - Core Net Profit Doubling, Overseas Expansion Continues

Company ProfileGeely is one of the leading enterprises in China's self-brand passenger vehicles manufacturers. The Company's products include six major brands: Geely, Geometry, Lynk, Zeekr, Livan, and Galaxy, covering the A0 to C-class passenger vehicles market. Investment SummaryStrong H1 Results With Core Net Profit Doubling YoY

Geely Auto announced its interim results for 2025. In H1 2025, total revenue reached RMB150.28 billion (RMB, the same below), up 26.5% yoy, marking a record high. Net profit attributable to the parent company was RMB9.29 billion, down 13.9% yoy. Excluding foreign exchange gains, impairment losses, and gains from deemed disposal of subsidiaries in 2024, core net profit attributable to the parent company was RMB6.66 billion, up 102% yoy.

In Q2 alone, the Company reported revenue of RMB77.79 billion, up 28.4% yoy and 7.3% mom. We estimate that core net profit attributable to the parent company, excluding foreign exchange gains and one-off items, was approximately RMB3.18 billion, up 127% yoy and down 8.7% mom. Slight Decline in Gross Margin, But Lower Expense Ratios

In H1 2025, the Company's overall gross margin declined by 0.3ppts yoy to 16.4%, mainly due to a higher sales proportion of economy NEVs and intensified industry price competition. However, this was partially offset by economies of scale and improved profitability of GEA architecture products. Zeekr's gross margin reached 19.7%, with Q1 and Q2 margins at 18.8% and 20.5%, respectively, reflecting emerging synergies following the February integration of Zeekr and LYNK & CO.

On the expense side, selling expense ratio and administration expense ratio dropped by 1.0ppts and 0.7ppts yoy to 5.6% and 1.9%, respectively, reflecting benefits from economies of scale and channel integration. R&D investment decreased 8.6% yoy to RMB8.35 billion, mainly focused on NEV and intelligent technologies. R&D expense ratio declined by 1.1ppts yoy to 6.6%, indicating synergies from the integration.

Despite a drop in ASP of RMB14 thousand yoy to RMB96 thousand per vehicle, the Company achieved a 37% yoy increase in core net profit per vehicle attributable to the parent company, reaching RMB4,724. Rapid NEV Sales Growth, Share Exceeding 50%

In H1, the Company's total vehicle sales reached 1,409 thousand units, up 47.4% yoy, significantly outperforming the 13% yoy growth in China's passenger car market. NEV sales totalled 725 thousand units, up 126.5% yoy, accounting for 51.5% of total sales (48.2% in Q1 and 54.7% in Q2). ICE vehicle sales rose 7.5% yoy, showing stable growth. Given strong performance, the Company raised its full-year sales target to 3,000 thousand units, equivalent to an increase from 25% to 38%.

By brand, Geely brand sales totalled 1,164 thousand units, up 56.99% yoy (including 548 thousand units from the Galaxy series, up 232% yoy). Zeekr sales reached 91 thousand units, up 3.3% yoy, and LYNK & CO sales were 154 thousand units, up 22.3% yoy. Overseas Expansion Continues to Deepen

In H1, the Company exported 184 thousand units, down 7.7% yoy, mainly due to weakness in Eastern European markets. However, NEV exports surged 146% yoy to 40 thousand units. Currently, exports account for only 13% of Geely's total sales, indicating significant room for growth. The Company has established five overseas regions---Europe, Latin America and Africa, Middle East and Asia, ASEAN, and Eastern Europe---to accelerate its internationalisation strategy across organisational structure, resource allocation, after-sales service, and product planning. With models such as the Galaxy E5, Starship 7, and Starwish entering overseas markets in H2, alongside accelerated promotion of premium models like LYNK & CO 08 and Z10, Zeekr 7X and 009, overseas sales are expected to regain strong growth momentum. Zeekr Privatization Accelerates Strategic Integration

On 15 July, the Company announced plans to privatise and delist Zeekr (ZK.N) from the NYSE, after which Zeekr will become a wholly owned subsidiary. Zeekr shareholders can choose between USD2.687 per share or 1.23 newly issued Geely Auto shares per Zeekr share. The Company will pay up to USD2.399 billion or issue up to 1.089 billion Geely Auto shares, equivalent to 11% of the current share capital.

The Zeekr privatization is a key step in Geely's return to its "One Geely" strategy, signalling a shift from multi-brand expansion to centralised operations. The consolidation aims to enhance strategic synergy and business integration among sub-brands, eliminate internal competition, reduce redundant investments, complement sales networks, and improve supply chain efficiency to drive cost reduction and efficiency gains. Going forward, the Company is expected to continue benefiting from technological synergies and cost optimization.

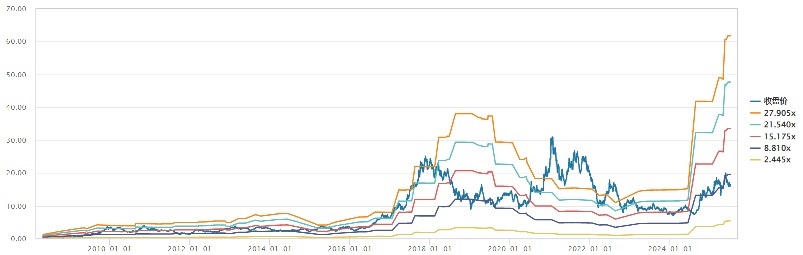

In 2025, the Company plans to launch 10 new models, including 5 under the Galaxy brand, 3 under Zeekr brand, and 2 under LYNK & CO brand. The already launched Starshine 8, LYNK & CO 900, and Zeekr 007GT have received positive market feedback, showing strong potential to become blockbuster models. Noteworthy launches expected in H2 include the Galaxy A7 and M9, Zeekr 9X and 8X, and LYNK & CO 10EM-P. These, together with growing momentum in overseas markets driven by new model rollouts, are expected to drive performance in the second half. Investment ThesisWe revised our financial forecast and target price to HK$24.3, equivalent to 14.4/12/9.6x P/E ratio in 2025/2026/2027, and we give the rating of Buy. (Closing price as at 25 August) Geely’s P/E Band trend

Source: Wind, Company, Phillip Securities Hong Kong Research Risk Factors1) Progress of new production line is below expectations;

2) Electric power tools sales fall short of expectations;

3) Macroeconomic downturn affects product demand;

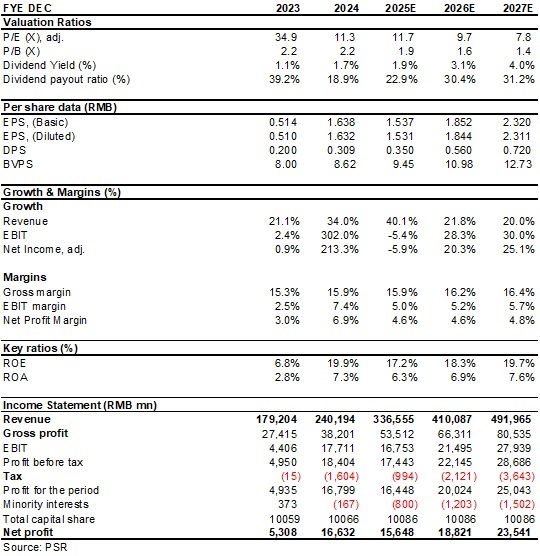

4) Sharply rising raw material prices or sharply falling product prices. Financial Data

(Closing price as at 25 August 2025) Download PDF Version Here...

| Recommendation on 26-8-2025 | | Recommendation | BUY (Maintain) | | Price on Recommendation Date | $ 19.710 | | Suggested purchase price | N/A | | Target Price | $ 24.300 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|