|

ZHOU LIU FU(6168)

Analysis:

Zhou Liu Fu is engaged in the design, development, and sale of jewelry products, including gold jewelry, diamond-encrusted jewelry, and other products. Its business model integrates jewelry product development, procurement, franchising, and brand operations, connecting all aspects of the industry value chain. The company boasts a nationwide sales network and a highly recognized brand. For the first half of the year ending June 30, 2025, the group achieved revenue of RMB 3.15 billion, a 5.2% increase year-on-year. Notably, online sales channels generated RMB 1.631 billion in revenue, up 34% from the previous year, driven by optimized operational efficiency, enhanced online capabilities, and deepened partnerships with e-commerce platforms, which expanded the scale of online sales. Additionally, the strategy of offering high cost-performance products to attract younger consumers further boosted online revenue growth.

Amid rising gold prices in recent years, the group has explored lighter and more fashionable product designs, leveraging strategies such as IP collaborations and combining gold with other materials to create accessories. These efforts aim to enhance the composite attributes of products and brands, fostering greater customer loyalty, higher gross margins, and improved profitability. In the first half of 2025, offline retail sales volume and revenue from marked-price products grew by 73.2% and 44.4% year-on-year, respectively, while the gross margin for offline retail increased by 12.2 percentage points to 41.7%. This provides strong guidance for the group to further explore a virtuous cycle of complementary product, brand, and operational development for brand upgrading.

Facing macroeconomic uncertainties and pressure on terminal consumption, the group continues to encourage terminal stores to optimize and adjust their layouts, implementing a survival-of-the-fittest approach for sales outlets while focusing on improving store operational efficiency. In the first half of 2025, the group net-closed 272 stores. As of June 30, 2025, the group operated 3,760 franchised stores and 97 self-operated stores, including 21 sub-brand stores. By city tier, the store structure became more balanced, with nearly 50% of stores located in Tier 1 and Tier 2 cities. By location type, the store structure was further optimized, with over 55% of stores situated in shopping malls and department stores. The average store size also increased to approximately 110 square meters.

Looking ahead, the group will increase investment in product innovation and R&D, focusing on popular IP designs and trendy manufacturing techniques. It plans to launch upgraded versions of brand-specific product series such as “Jiuhua Dayuan” and “Yihe Xianjing” to further promote Eastern culture and the “national trend” style. Additionally, the group has several new series in development, emphasizing popular techniques like point diamonds and filigree. The group will adopt a multi-ecosystem expansion strategy, including franchised, self-operated, joint-venture, high-end, and overseas stores. It sees significant growth potential in overseas markets and plans to actively expand in Southeast Asia, having already opened six stores in Thailand, Laos, Vietnam, Cambodia, and Malaysia. Further expansion is planned in Singapore and other regions, with a target of opening 10 overseas stores by year-end. (I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $48.00, Target Price: $52.50, Cut Loss Price: $45.50

|

JD HEALTH(6618)

Analysis:

In the first half of 2025, the company reported revenue of RMB 35.3 billion (+24.5%), primarily driven by growth in product sales revenue from pharmaceutical and healthcare products. The increase in product revenue was mainly attributable to a growing number of active users, additional purchases by users, the rising online penetration rate of pharmaceutical and health product sales, and an expanded product portfolio. Net profit attributable to shareholders reached RMB 2.6 billion (+27.5%), demonstrating strong profitability resilience. Basic earnings per share were RMB 0.82 (+26.2%).

The core drivers of the company’s performance growth include the increased online penetration of pharmaceutical e-commerce, the large-scale implementation of AI technology (the "AI Jing Doctor" service has served over 50 million users), and the advantages of an omnichannel supply chain (33 pharmaceutical warehouses covering nearly 400 cities). In the long term, supportive industry policies (the "Healthy China 2030" initiative) and upgraded health consumption demand provide broad growth opportunities. However, attention should be paid to intensifying industry competition and changes in healthcare policies.

We believe that as a leading player in China’s online healthcare industry, JD Health is well-positioned to maintain its leading role in industry growth by leveraging its core strengths in pharmaceutical e-commerce, deep integration of AI technology, and omnichannel strategy.

Strategy:

Buy-in Price: $67.00, Target Price: $73.80, Cut Loss Price: $64.00

|

|

MAO GEPING (1318.HK) - Strong Performance in H1 2025 with Further Consolidation of Leading Position in the High-End Cosmetics Market

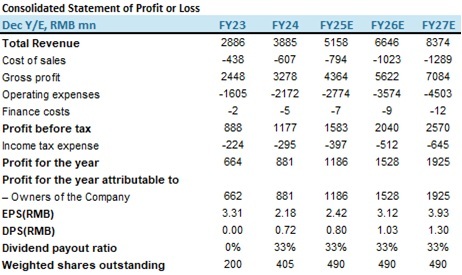

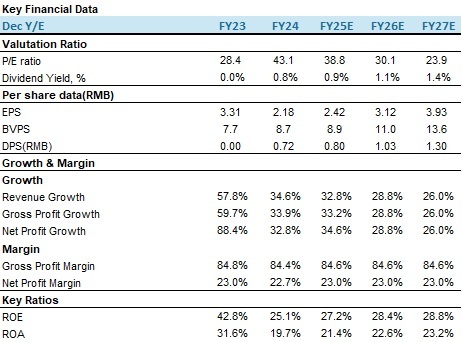

OverviewMGP primarily engages in the R&D, production, sales, and makeup skill training services under two major brands: MGPIN and ZHUIAIZHONGSHENG. Leveraging the profound aesthetic expertise, unique understanding of Eastern women's facial contours and skin characteristics, and the influence of its founder, renowned makeup artist Mr. Ma Ge Ping, the company has gradually established a strong brand advantage in the cosmetics and makeup training sectors. With an increasingly diverse product portfolio and stable growth across both online and offline channels, MGP has emerged as a leading domestic high-end beauty brand. Performance reviewIn H1 2025, the company reported revenue of RMB 2.588 billion with a year-on-year increase of 31.28%, though growth slowed compared to 2024. We attribute this primarily to the following factors:1. Intensified market competition, with strong international beauty brands such as L'Oréal and Estée Lauder, coupled with rising efforts from local beauty companies. Some competitors have also adopted strategies similar to MGP's "professional makeup artist IP" approach (e.g., Caitang under Proya, NAN beauty launched by CHICMAX in collaboration with makeup artist Chun Nan), which has partially diverted the company's target customer base.2. Natural slowdown in the growth of core businesses (including cosmetics and skincare products).3. The new fragrance business has not yet contributed significantly.Net profit attributable to shareholders reached RMB 670 million, with a year-on-year increase of 36.1%. EPS was RMB 1.37, with a year-on-year decrease of 44.3%. Stable Growth Across Online and Offline Channels, Continued Efforts in E-commerceIn H1 2025, offline revenue reached RMB 1.224 billion, up 26.6% year-on-year, accounting for 48.6% of total revenue. This was mainly due to enhanced sales and marketing efforts, increased average sales per counter, and resumed growth in sales to a high-end multinational beauty retailer. Online revenue was RMB 1.297 billion, up 39% year-on-year, accounting for 51.4% of total revenue, driven by strengthened sales and marketing activities on e-commerce platforms. As of June 30, 2025, the total number of registered members under the company's online and offline loyalty programs was approximately 13.4 million and 5.6 million respectively. The overall repurchase rate further increased to 26.8%, up 2 percentage points year-on-year. Strong Growth in Cosmetics and Skincare, Fragrance Business Begins to ContributeIn H1 2025, cosmetics sales revenue reached RMB 1.422 billion, up 31.08% year-on-year, accounting for 55% of total revenue. Skincare revenue was RMB 1.087 billion, up 33.4% year-on-year, accounting for 42% of total revenue. Revenue from the new fragrance business was RMB 11 million, accounting for 0.4% of total revenue. The newly launched high-end fragrance series, "Guo Yun Ning Xiang" and "Eastern Whisper Enlightenment," sold 35,000 units within just over a month of launch. We are optimistic about the future sustained growth of the high-end domestic fragrance business. Revenue from makeup art training and related sales was RMB 67 million, down 5.86% year-on-year, accounting for 2.6% of total revenue. This decline was mainly due to strict controls on student enrollment and class occupancy rates to improve training service quality and student satisfaction under existing training venue conditions, as well as the discontinuation of pre-exam training fees from 2025. Hero Products Continue to ShineMGP's hero products primarily fall into two categories: cosmetics and skincare. In cosmetics, its key hero products include contouring, highlighting, and foundation products. In skincare, its star products are the Luxury Caviar Facial Mask and Luxury Regenerating Black Cream. The Luxury Caviar Facial Mask achieved retail sales of over RMB 800 million in 2024. In H1 2025, the company's foundation products continued to perform strongly, with the Luxury Caviar Cushion and Luminous Light Veiling Pressed Powder each achieving retail sales of over RMB 200 million. The Luxury Caviar Facial Mask and Luxury Regenerating Black Cream achieved retail sales of over RMB 600 million and RMB 200 million respectively. According to Qingyan Intelligence data, the size of China's foundation market reached RMB 47.8 billion in the first seven months of 2025 and is expected to exceed RMB 100 billion for the full year, with year-on-year growth of over 15%. On Douyin, the foundation market saw high growth in concealer (52.81%) and highlighter (83.10%) products, forming an innovative growth triangle. This indicates that Douyin beauty users are gradually shifting toward refined foundation products. MGP's contouring, highlighting, and foundation products effectively meet consumer demands. In H1 2025, MGP's foundation products held a 3.1% market share on Tmall and 6.4% on Douyin. Its cushion products held a 9.8% market share on Tmall and 4.1% on Douyin. We believe the hero product strategy is a core pillar of the brand's success, perfectly blending its "professional makeup artist" brand DNA with market commercialization needs, carving out a unique path for high-end domestic brands. Company valuationMGP is a leading domestic high-end beauty brand, with core drivers including product premiumization under its high-end positioning, synergistic expansion across online and offline channels, and empowerment through its makeup artist brand IP. We expect the company to maintain a compound annual growth rate (CAGR) of over 25% in revenue over the next three years. However, intensified industry competition may constrain its long-term growth potential. Despite strong revenue growth in H1 2025, the pace has slowed. We forecast revenue for 2025-2027 to be RMB 5.158 billion, RMB 6.646 billion, and RMB 8.374 billion respectively, with EPS of RMB 2.42, RMB 3.12, and RMB 3.93. The current stock price corresponds to a P/E ratio of 38.8x, 30.1x, and 23.9x for 2025-2027. Based on a target 2026 P/E of 32x, we adjust the target price to HKD 108.52 and maintain an "Accumulate" rating. (Current price as of September 09) Risk factors1) The macro-economy is in a downward trend;

2) Industry competition is intensifying;

3) New product promotion is not as good as expected. Financial Data

Current Price as of: 09 Sep 2025

Source: PSHK Est. Download PDF Version...

| Recommendation on 10-9-2025 | | Recommendation | Accumulate | | Price on Recommendation Date | $ 102.000 | | Suggested purchase price | N/A | | Target Price | $ 108.520 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|