|

SICC(2631)

Analysis:

SICC is primarily engaged in the research, development, manufacturing, and sales of silicon carbide (SiC) substrates. It is one of the few companies globally capable of mass-producing 8-inch SiC substrates and among the first to commercialize SiC substrates ranging from 2 inches to 8 inches. It is also a pioneer in launching 12-inch SiC substrates. According to the Strategic Emerging Industries Classification (2018) issued by the National Bureau of Statistics, its products fall under “1.2.3 High-Energy Storage and Key Electronic Materials Manufacturing” and “3.4.3.1 Semiconductor Crystal Manufacturing,” making it a strategically important emerging industry strongly encouraged and supported by the state.

Silicon carbide is a compound material composed of carbon and silicon elements, characterized by high hardness and excellent physical and chemical properties. SiC materials offer features such as high voltage resistance, high-frequency performance, high thermal conductivity, high-temperature stability, and high refractive index, making them a critical material for cost reduction and efficiency improvement across various industries. Compared to silicon-based semiconductors, wide-bandgap semiconductors represented by SiC and gallium nitride (GaN) exhibit superior performance from material to device levels, with characteristics including high frequency, high efficiency, high power, high voltage resistance, and high-temperature durability. These qualities position them as a key direction for the future development of the semiconductor industry. In particular, SiC demonstrates unique physical and chemical properties, such as high bandgap width, high breakdown electric field strength, high electron saturation drift velocity, and high thermal conductivity, making it critical in applications like power electronic devices. These attributes give SiC significant advantages in high-performance applications such as electric vehicles and photovoltaics, especially in terms of stability and durability.

SiC substrates are widely used in downstream products such as power semiconductor devices, radio-frequency semiconductor devices, optical waveguides, TF-SAW filters, and heat dissipation components. Key application industries include electric vehicles, photovoltaic and energy storage systems, power grids, rail transit, communications, AI glasses, smartphones, and semiconductor lasers. As a substrate manufacturer, SICC is an upstream participant in the SiC semiconductor device industry chain, playing a critical role in converting raw materials into substrate products for downstream use. The company continues to enhance the production capacity and output of its core products. Its Jinan factory has steadily increased capacity through technological and process improvements, while its Shanghai Lingang factory achieved its planned annual production capacity of 300,000 conductive substrates by mid-2024, ahead of schedule. It is now advancing its second-phase capacity expansion plan, with the combined designed capacity of both factories exceeding 400,000 substrates.(I do not hold the aforementioned stock.)

Strategy:

Buy-in Price: $47.00, Target Price: $52.00, Cut Loss Price: $44.50

|

ZIJIN MINING(2899)

Analysis:

In the first half of 2025, the company reported revenue of RMB 167.71 billion (up 11.5% year-on-year). The production of its primary mineral products continued to grow steadily: Mineral copper output reached 570,000 tonnes, a 9% increase YoY; Mineral gold output amounted to 41 tonnes, up 16% YoY; Mineral silver output totaled 224 tonnes, a 6% increase YoY; Mineral zinc (lead) output was 200,000 tonnes, and lithium carbonate equivalent production reached 7,315 tonnes. Benefiting from higher production volumes, elevated prices, and cost optimization, the overall gross profit margin of the company’s mineral products increased by 3 percentage points YoY to 60.23%. Net profit attributable to shareholders reached RMB 23.29 billion (up 54.41% YoY). EPS was RMB 0.877 (up 52.79% YoY). Net cash flow from operating activities amounted to RMB 28.8 billion (up 41% YoY), primarily driven by higher gross profit from mineral product sales, reflecting ample and stable cash flow. Growing expectations of interest rate cuts, coupled with escalating tensions in the Middle East, have catalyzed a rise in gold prices. Meanwhile, persistent supply-side issues in copper have kept copper prices strong amid fluctuations. We believe that Zijin Mining benefits from the dual drivers of gold and copper, with abundant resource reserves, robust profitability, and prominent growth visibility, making it a valuable long-term investment.

Strategy:

Buy-in Price: $29.00, Target Price: $32.00, Cut Loss Price: $27.20

|

|

ADD Industry (603089 CH) - Effective Cost Rate Control Boosted Net Profit Margin,with Overseas Plant to Commence Production Soon

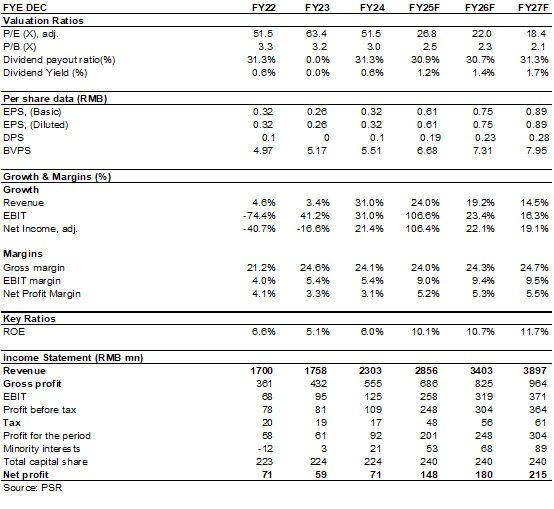

Company ProfileADD Industry was established in 1994, specialising in the field of shock absorbers of the automotive suspension system. It has nearly 20 thousand product models covering most vehicle types worldwide and is a leading enterprise in China's shock absorber industry. At present, its business mainly includes shock absorbers of the automotive suspension system, automotive rubber damping products, as well as engine sealing components and other auto parts. In 2024, revenue reached RMB2,303 million (RMB, the same below), up 31.0% yoy, with overseas sales accounting for 82%. Net profit attributable to the parent company was RMB71 million, and net profit attributable to the parent company excluding non-recurring items was RMB64 million, up 21.4% and 22.2% yoy, respectively. Investment SummaryStrong Growth in H1 2025 Results

The Company released its 2025 semi-annual report. In H1 2025, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB1,356 million/RMB119 million/RMB69 million, up 39.62%/420.67%/269.37% yoy, respectively. In Q2 2025 alone, the Company reported revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB740 million/RMB89 million/RMB41 million, up +34.62%/+1113.3%/+914.6% yoy, respectively. Effective Cost Rate Control Boosted Net Profit Margin

According to the semi-annual report, gross margin was 24.29%, down 0.53 ppts yoy, remaining broadly stable, while gross profit increased by RMB88.4 million yoy. Period cost rate declined 3.2 ppts yoy to 12.6%, with sales/administration/R&D/financial cost rates down by-1.8/-1.3/+0.01/-0.2 ppts yoy, respectively, showing significant benefits from scale effect and cost control. In addition, the Company disposed of a piece of plant land during the period, recording a one-off disposal gain of RMB55 million, which also contributed to earnings growth. Net profit margin rose 7.07 ppts to 10.16%, and net profit margin excluding non-recurring items rose 3.16 ppts to 5.08%. Meanwhile, net cash flow from operating activities surged 412.6% yoy, reflecting continuous improvement in earnings quality. Capacity Upgrade and Value Chain Integration

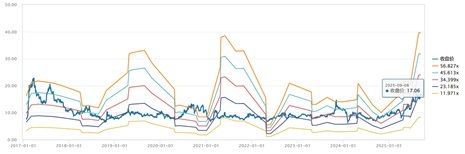

The Company is actively promoting capacity upgrading with its "Zhengyu Intelligent Manufacturing Park" as a platform. By the end of the reporting period, the Park had achieved a significant increase in production capacity, and the intelligent factory capacity matrix had been gradually established. The new Park not only significantly shortened the order delivery cycle but also formed an integrated "R&D--Intelligent Manufacturing--Delivery" closed-loop system, consolidating the Company's capability for rapid product iteration and continuously strengthening its technological moat in the industry. In terms of vertical integration, the Park extended the industrial chain upstream and has begun mass production of self-made high-precision stamping parts, high-precision piston rods, solenoid valves and other key shock absorber components, achieving in-house production of core parts. The deep extension of the industrial chain effectively reduced product defect rates, further optimised production costs, and established a rapid response mechanism, perfectly meeting the global customers' flexible customisation and high-frequency turnover demand for "multi-variety, small-batch, multi-batch" one-stop procurement. Global Deployment Accelerating Capacity Expansion, with Overseas Plant to Commence Production SoonThe Company's intelligent manufacturing base in Thailand has already entered large-scale production, and investment will continue to be increased to expand capacity. At present, the Company's capacity expansion is entering an accelerated phase. Capacity was RMB1.7 billion in 2023 and is expected to reach RMB4.4 billion by 2027, an expansion of 2.5 times in four years. The Company has a production capacity of RMB3.4 billion in China and a capacity of RMB1.0 billion in Thailand, further strengthening its global delivery capability. Investment ThesisAs a leading enterprise in the domestic shock absorber industry, the Company has achieved in-house production of core components through the construction of intelligent manufacturing parks, enhancing its vertical integration capability. Such technological barriers and economies of scale enable it to occupy a favourable position in the global automotive after-market. With global vehicle ownership exceeding 1.6 billion units, equivalent to demand for over 800 million shock absorbers, and a market size of about RMB70 billion, the Company is well positioned to continue benefiting from this trend.As for valuation, we expected diluted EPS of the Company to RMB 0.61/0.75/0.89 of 2025/2026/2027. And we accordingly gave the target price to RMB18.78, respectively 31/25/21x P/E for 2025/2026/2027. "Accumulate" rating. (Closing price as at 10 September) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Risk Factors1) Progress of new production line is below expectations;

2) Overseas market risk;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financial Data

(Closing price as at 10 September 2025) Click to download PDF version...

| Recommendation on 11-9-2025 | | Recommendation | Accumulate (Initiation) | | Price on Recommendation Date | $ 16.480 | | Suggested purchase price | N/A | | Target Price | $ 18.780 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|