|

Shanghai Electric(2727)

Analysis:

Shanghai Electric is primarily engaged in the design, manufacture, and sale of energy equipment (including nuclear power equipment, energy storage equipment, coal-fired power generation and supporting equipment, gas-fired power generation equipment, wind power equipment, hydrogen energy equipment, photovoltaic equipment, high-end chemical equipment, and providing grid and industrial intelligent power supply system solutions) and industrial equipment (including elevators, large and medium-sized motors, intelligent manufacturing equipment, industrial basic components, industrialized construction equipment, and integrated services such as energy, environmental protection, and automation engineering and services). In the first half of 2025, the group achieved new orders worth RMB 109.8 billion, including RMB 60.04 billion in energy equipment (of which: RMB 20.08 billion in coal-fired power generation equipment, RMB 6.77 billion in nuclear power equipment, RMB 13.9 billion in wind power equipment, and RMB 7.46 billion in energy storage equipment), RMB 22.82 billion in industrial equipment, and RMB 26.95 billion in integrated services.The group actively seizes opportunities in national energy policies, serving the construction of new power systems. In the nuclear power sector, it has mastered key equipment manufacturing and inspection technologies. In the coal-fired power generation sector, it continues to focus on the “three-transformation linkage” market for coal power, maintaining the global record for the lowest coal consumption in coal-fired power units. In the gas turbine sector, the group is the only domestic supplier with mature full-lifecycle supply and service capabilities for heavy-duty gas turbines. In the wind power sector, Shanghai Electric Wind Power Group, a subsidiary, has leading domestic capabilities in wind turbine design and manufacturing, building China’s largest offshore wind power sample database and creating several benchmark offshore wind power projects. Through technological innovation, product diversification, and industrial chain integration, it has developed an onshore product matrix covering 1.25–11MW, addressing various complex terrains. In the energy storage sector, the group is actively developing technologies such as compressed air energy storage and flow battery energy storage, building a collaborative ecosystem for diverse energy storage industries and providing multi-scenario energy storage solutions.In the industrial basic components sector, the group’s blade business has expanded from traditional coal-fired steam turbine blades to aviation, aerospace, and gas turbine blades, upgrading from energy blades to high-end products such as aviation blades, critical core components, and hot-end components, becoming a leading manufacturer of key components in the “two-machine” (aviation and gas turbine) sector. In the aviation assembly manufacturing line sector, the group leverages its extreme manufacturing capabilities and integrated equipment strengths to provide safe, controllable, and intelligent solutions for high-end manufacturing users, such as aircraft manufacturing and aero-engine production. In the robotics sector, the group adopts a dual-driven approach of “independent R&D + ecosystem collaboration,” initially establishing an industrial chain covering industrial robots, specialized robots, and intelligent robots.(I do not hold the aforementioned stock)

Strategy:

Buy price: HK$3.85, target price: HK$4.1, stop-loss price: HK$3.65

|

Horizon Robotics(9660)

Analysis:

To date, Horizon Robotics has established partnerships with over 40 global automakers and brands, including all of China's top ten automotive companies. The company has launched over 200 mass-production models and secured design wins for more than 400 models. Its Journey series of in-vehicle intelligent computing solutions have achieved cumulative shipments exceeding 10 million units in pre-installation applications. In 2024, Horizon Robotics maintained its leading position in the domestic autonomous passenger vehicle intelligent driving computing solutions market, capturing a 33.97% market share among independent Chinese brands. The company raised funds through a top-up shares placement model, issuing 639 million new shares (representing 4.6% of the current total share capital) at a price of HKD 9.99 per share. The total proceeds from the placement amounted to approximately HKD 6.34 billion, with net proceeds of about HKD 5.8 billion after deducting expenses, marking one of the company's largest single fundraising efforts in recent years.

Strategy:

Buy price: $9.50, Target price: $10.45, stop-loss price: $8.75

|

|

Zhongding Group (000887.CH) - Expanding Liquid Cooling and Robot Business to Explore Growth Opportunities

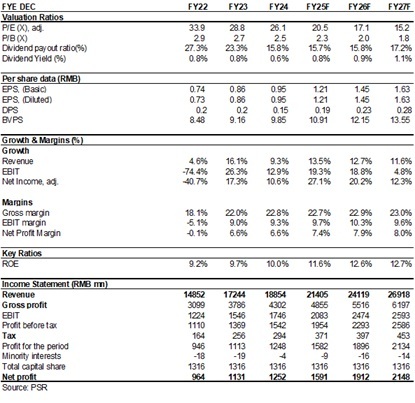

Company profileThe company was founded in 1980 and is a multinational private enterprise group primarily focused on automotive components. Since 2008, the company has expanded its business through overseas acquisitions. Currently, its main business segments include intelligent chassis systems (encompassing air suspension systems and lightweight chassis systems), thermal management systems, sealing systems, and the humanoid robot business. In 2024, the company achieved a revenue of RMB18,854 million (RMB, the same below), a yoy increase of 9.33%, with domestic and overseas revenue shares at 51.71% and 48.29%, respectively. The net profit was RMB1,254 million, a yoy increase of 10.63%. Investment SummaryStable Growth in the First Half of 2025

In the first half of 2025, the company recorded revenue of RMB9,846 million, net profit attributable to the parent company of RMB817 million, and net profit excluding non-recurring items of RMB780 million, with yoy growth rates of +1.83%, +14.11%, and +21.53%, respectively. The gross margin was 23.58%, a yoy increase of 1.35 percentage points. In the second quarter of 2025, the company recorded revenue of RMB4,992 million, net profit attributable to the parent company of RMB415 million, and net profit excluding non-recurring items of RMB414 million, with yoy growth rates of +0.31%, +16.74%, and +21.61%, respectively. Stable Growth in Traditional Businesses and Rapid Development of New Businesses

In recent years, the company has actively expanded into the new energy vehicle (NEV) sector, focusing on intelligent chassis systems. It has also achieved international leadership in several new energy sectors, including thermal management systems, lightweight chassis systems, and air suspension systems. In the first half of 2025, the revenue from cooling systems (thermal management), rubber business, sealing systems, lightweight chassis, and air suspension systems reached RMB2,606 million, RMB2,043 million, RMB1,942 million, RMB1,546 million, and RMB568 million, respectively, with yoy growth rates of +2.77%, +5.88%, +0.27%, +8.08%, and -0.66%. In the first half of the year, the company's sales in the new energy sector reached RMB3,762 million, accounting for 39.56% of its automotive business revenue, with domestic new energy sector sales reaching RMB2,887 million, accounting for 52.94% of domestic revenue.

In terms of orders, air suspension systems, lightweight chassis, and cooling systems have received orders amounting to RMB15.8 billion, RMB5.5 billion, and RMB7.1 billion, respectively. Internationalization Strategy Reaching Harvest Phase

Since 2008, the company's internationalization strategy has gradually entered a harvest phase. From 2014 to 2018, through a series of overseas acquisitions, such as Germany's KACO and France's TFH, the company accelerated its international expansion. As of the first half of 2025, the company's production share in Asia, Europe, and the Americas was 65.41%, 25.04%, and 9.55%, respectively. By effectively integrating global resources, the company has quickly improved its technology, brand, profitability, and customer base, achieving dual-wheel drive through internal growth and external expansion. Actively Expanding Liquid Cooling and Robot Business to Explore Growth OpportunitiesBuilding on its automotive thermal management business, the company is actively expanding into energy storage thermal management, and supercomputing center thermal management. In the energy storage field, it has launched a series of liquid cooling units and immersion liquid cooling units. In the supercomputing center thermal management field, its main product is the CDU (cold liquid distribution unit). In the future, based on actual needs, the company plans to gradually apply immersion technology to supercomputing center thermal management and is currently accelerating customer engagement.

In the robot business, the company has completed its industrial layout in joint assemblies, harmonic reducers, planetary reducers, and force sensors through its subsidiaries, such as Anhui Ruisibo and Xinghui Sensing. The company's rubber products have already been matched, and lightweight skeletons have been sent to customers for sampling, ultimately aiming to achieve production and manufacturing of robot joint assembly products. The company and its subsidiaries have signed strategic cooperation agreements with Shenzhen Zhongqing Robot Technology Co., Ltd. and EFFORT Intelligent Equipment Co., Ltd. It has also signed project intention cooperation agreements with Shenzhen Zhuji Power Technology Co., Ltd., forming an upstream and downstream industrial chain layout to promote the development of robot body manufacturing and OEM business. Investment ThesisThe company's automotive business remains stable, while it actively explores liquid cooling and robot business opportunities. We are highly optimistic about the company's development prospects.

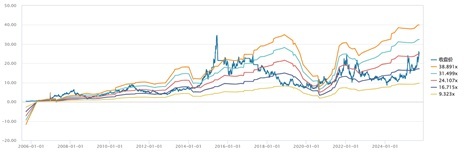

As for valuation, we expected diluted EPS of the Company to RMB 1.21/1.45/1.63 of 2025/2026/2027. And we accordingly gave the target price to RMB 29, respectively 24/20/17.8x P/E for 2025/2026/2027. "Accumulate" rating. Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Source: Wind, Company, Phillip Securities Hong Kong Research Risk Factors1) Progress of new production line is below expectations;

2) Overseas market risk;

3) Macroeconomic downturn affects product demand;

4) Sharply rising raw material prices or sharply falling product prices. Financials

(Closing price as at 26 September) Click here to download PDF version...

| Recommendation on 30-9-2025 | | Recommendation | Accumulate (Initiation) | | Suggested purchase price | $ 24.79 | | Target Price | $ 29.000 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|