|

COSCO SHIP ENGY(1138)

Analysis:

COSCO Shipping Energy Transportation focuses on two core businesses: oil tanker transportation and LNG transportation. It boasts the world’s largest oil tanker fleet capacity, covering all mainstream oil tanker types, making it the most comprehensive oil tanker owner globally. As of June 30, 2025, the Group owns and controls a fleet of 157 oil tankers with a total capacity of 23.448 million deadweight tons (DWT) and has 18 oil tankers under construction with a capacity of 2.961 million DWT.

In terms of LNG transportation, as of June 30, 2025, the Group has participated in the investment and construction of 87 LNG vessels, of which 52 vessels with a capacity of 8.763 million cubic meters are operational, and 35 vessels with a capacity of 6.285 million cubic meters are under construction. Additionally, there is one bareboat-chartered LNG vessel with a capacity of 174,000 cubic meters. All operational vessels are serving long-term charters, ensuring relatively stable revenue. As the LNG vessels under investment and construction progressively become operational, the Group’s LNG transportation business has entered a harvest period.

As the oil tanker owner with the most comprehensive fleet types, the Group utilizes its owned and controlled vessels to engage in various operations, including spot market chartering, time chartering, signing Contracts of Affreightment (COA) with cargo owners, and participating in pool operations (POOL or CHINA POOL). By leveraging synergies between international and domestic trade, large and small vessels, and crude and refined oil, the Group maximizes its vessel type and route advantages. This enables it to provide end-to-end logistics solutions, including importing raw materials for international trade, domestic transshipment, refined oil transfer and export, and downstream chemical product transportation, helping clients reduce logistics costs and achieve mutually beneficial cooperation.The Group recently completed an A-share issuance to specific investors, issuing 694,444,444 shares at RMB 11.52 per share, raising net proceeds of RMB 7.979 billion. The issuance involved seven investors, including the indirect controlling shareholder COSCO Shipping Group, National Green Development Fund, China Reform Holdings, China State-Owned Enterprises Structural Adjustment Fund, Cinda Securities, Hubei Railway Development Fund, and China State-Owned Enterprises Mixed Ownership Reform Fund. The raised funds will be used to construct six VLCCs, two LNG carriers, and three Aframax crude oil tankers, expected to optimize the fleet structure and enhance the clean energy layout, securing the company’s future fleet scale and market competitiveness.

OPEC+ has accelerated production increases since April this year, which is expected to drive crude oil prices downward, encourage refineries to replenish inventories, boost crude oil trade demand, and inject momentum into the oil tanker market. Additionally, after the U.S. imposed port service fees on Chinese shipping companies and Chinese-built vessels, China retaliated by imposing special port fees on U.S.-related vessels in accordance with regulations. Against this backdrop, Chinese shipping companies like COSCO Shipping Energy Transportation will see greater strategic value.(I personally do not hold the above stock).

Strategy:

Buy-in Price: $9.90, Target Price: $10.80, Cut Loss Price: $9.40

|

LENS(6613)

Analysis:

The company was established in 2003 and relocated its headquarters to Liuyang, Hunan in 2006. In 2015, it became a one-stop precision manufacturing solution provider for the entire smart terminal industry chain. Its business covers structural components, functional modules, and whole-unit assembly for smart terminals such as smartphones and computers, smart vehicles and cockpits, smart headsets and wearables, and humanoid robots. It involves materials such as glass, metal, sapphire, ceramics, plastics, leather, fiberglass, and carbon fiber, along with supporting auxiliary materials, tooling fixtures, molds, production equipment, testing equipment, automated machinery, and its self-developed industrial internet system. In H1 2025, total revenue reached RMB 32.96 billion, representing a year-on-year increase of 14.2%. Gross profit was RMB 4.305 billion, up 17.8% year-on-year, primarily driven by increased gross profits from the smartphone and computer business as well as the smart headset and wearable business. Net profit attributable to owners of the parent was RMB 1.143 billion, a year-on-year increase of 32.7%, with earnings per share of RMB 0.23. An interim dividend of RMB 0.1 per share was declared. The smartphone and computer business accounted for 82.5% of total revenue in H1 2025, making it the primary revenue source. As a core supplier for the iPhone, the company benefited from the latest data from Counterpoint Research, which showed that sales of the iPhone 17 series in the Chinese and U.S. markets increased by 14% in the first 10 days of sales compared to the iPhone 16 series during the same period. In China, sales of the standard version nearly doubled, while demand for the Pro series remained strong in the U.S., driving up the company’s stock price. Driven by three key factors—the recovery in consumer electronics demand, Apple’s new product cycle, and the scaling up of the automotive business, the company’s performance growth momentum remains robust.

Strategy:

Buy-in Price: $26.88, Target Price: $30.20, Cut Loss Price: $25.50

|

|

Minth Group (425.HK) - Battery Box Becomes the Largest Business Segment

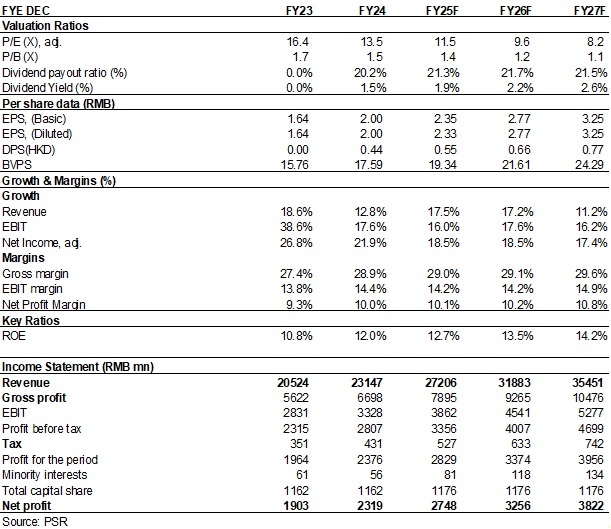

Company ProfileMinth Group is a world-renowned supplier engaged in the design, manufacturing and sales of automotive interior and exterior trim and body structure parts. The domestic market share of its core products exceeds 30%. The company has production bases in China, the United States, Mexico, Thailand, Germany, Serbia and other countries, and its customers cover major vehicle companies in the market. Based on a variety of new materials and surface treatment technologies, in recent years the company has developed new electrified and smart product lines such as aluminum power battery boxes and smart front faces, forming a series of competitive terminal products. Investment SummaryStrong Profit Growth Maintained in H1 2025, Net Profit Up Nearly 20%

Minth Group recorded revenue of RMB12.287 billion (RMB, the same below) in H1 2025, up 10.8% yoy; net profit attributable to the parent company reached RMB1.277 billion, equivalent to an increase of 19.5% yoy. The main drivers behind the profit growth include: 1) continued ramp-up of orders for NEV components such as battery boxes, leading to higher capacity utilisation; 2) incremental earnings contribution from capacity ramp-up at overseas production bases; 3) decline in unit transportation costs and favourable exchange rates. Meanwhile, the Company continued to advance its localisation strategy and implement effective cost control measures, resulting in lower expense ratios.

By region, domestic revenue was RMB4.31 billion, down 4.9% yoy, mainly due to the decline in market share of joint venture brands in China. International business remained strong, with revenue up 21.6% yoy to RMB7.98 billion, primarily driven by rapid growth in battery box and structural component businesses in the European market, as well as stable contributions from traditional exterior parts in international markets. The proportion of international business in total revenue rose by 5.2 ppts from 59.7% at the end of 2024 to 64.9%. The localisation strategy in North America, Europe and other regions has effectively reduced tariffs and geopolitical risks, while enhancing competitiveness in local markets. Battery Box Becomes the Largest Business Segment

In H1, the Company's revenue from plastic parts, metal and trims, battery boxes, and aluminium parts reached RMB2.87/2.66/3.58/2.47 billion respectively, up 0.9%/4.7%/49.8%/4.1% yoy. Their respective shares of total revenue changed by -2.3/-1.3/+7.6/-1.3 ppts yoy, to 23.3%/21.6%/29.2%/20.1%.

During the review period, the Company achieved breakthroughs in its battery box and body chassis structure businesses, with a more balanced customer mix: it broke into the structural component business for Toyota Europe, and secured chassis structure orders from multiple Chinese clients such as Great Wall and Geely; entered the battery box business of Chery for the first time and secured repeat orders from BYD; made its first breakthrough in battery box structural parts for General Motors; and continued to expand its battery box business with Stellantis and Volkswagen. In the area of smart interior and exterior parts, the Company achieved breakthroughs in bumper assembly business with Ford North America and Renault, while continuing to secure orders from clients such as Toyota, Hyundai-Kia, Changan, and General Motors. Profitability Continued to Improve SteadilyDuring the period, gross margin was approximately 28.3%, down 0.2 ppts yoy, mainly due to the rising contribution from the battery box business. The gross margins of the four major business segments were 26.1%, 28.1%, 23.0%, 32.6%, representing yoy changes of +2.0, +1.6, +2.4, -2.4 ppts, respectively. Among them, the battery box segment achieved a gross margin of 23%, moving closer to the 25% target. During the period, selling, administration and R&D expense ratios declined by 0.6, 0.1, and 0.5 ppts yoy respectively, lifting net profit margin by 0.8 ppts to 10.4%, indicating an improvement in the Company's profitability.

Operating cash flow rose by RMB 510 million yoy to RMB2.24 billion in H1 2025, reflecting sound cash flow conditions, which provide a solid basis for dividend payments and share buybacks. Capital expenditure stood at RMB902 million, down 17.5% yoy, as the Company has passed its peak investment phase and will focus on equipment upgrades and flexible transformation going forward. In H2, as several new overseas production lines continue to ramp up, overall gross margin is expected to see a slight improvement mom. New Businesses and Emerging Segments Gearing UpThe Company is actively exploring new business segments and has made forward-looking deployments in areas such as eVTOL (electric vertical take-off and landing aircraft), wireless charging for electric vehicles, and bionic robots---including core components such as electronic skin, smart masks, integrated joints, bodies, and rotors. During the period, the Company partnered with leading enterprises including EHang and Zhiyuan Robotics. Some products have completed small-batch sample deliveries to multiple customers, and some have already secured mass production orders, with revenue contribution expected to begin in 2026/2027. With the rapid development of robotaxis and autonomous driving, the wireless charging industry is projected to experience explosive growth in 2026. At the same time, leveraging its battery box technology, the Company is also focusing on the development and implementation of AI liquid-cooling system-related products, aiming to capture opportunities in the rapidly growing artificial intelligence market. ValuationThe company maintains stable overall operations, with continuous improvement in profitability, demonstrating strong risk resilience and growth adaptability. Meanwhile, the cultivation of new business areas and the expansion of new ventures are expected to foster a second growth curve, driving the company's sustainable development in the medium to long term.

We slightly revised the expected EPS for 2025/2026/2027 to 2.35/2.77/3.25 (from 2.43/2.89/3.30) yuan for the under expected GM.

We believe that it is reasonable to give the Company a valuation of 12.7/10.6/9.0 x P/E and 1.5/1.4/1.2x P/B for 2025/2026/2027, equivalent to target price of HK$ 32.6 and Accumulate rating. P/E Band

Source: Wind, Phillip Securities Hong Kong Research Financials

(Closing price as at 17 October 2025) Click here to download PDF version...

| Recommendation on 22-10-2025 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 29.480 | | Suggested purchase price | N/A | | Target Price | $ 32.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|