|

Eternal Beauty(6883)

Analysis:

Eternal Beauty engages in the retail, wholesale, and distribution of perfumes, skincare products, makeup, personal care products, eyewear, and home fragrances in China (including Hong Kong and Macau). It primarily generates revenue by selling and distributing products procured from third-party brand licensors. The group possesses a vast and diversified portfolio of iconic brands, encompassing not only perfumes but also makeup, skincare, personal care products, eyewear, and home fragrances, with the products mainly originating from Europe, Japan, and the United States. As of September 30, 2025, the group’s external brand portfolio covers a total of 74 brands, including 53 perfume brands, 22 home fragrance brands, 17 skincare brands, 10 personal care brands, 8 eyewear brands, and 6 makeup brands. In addition to managing external brands, the group is actively developing its own brand, Santa Monica. Building on the existing series, it launched five upgraded perfumes and two fragrance candles in 2025, taking the first step into the home fragrance sector, which will further enrich the own-brand product portfolio.

The group sells to over 400 cities in mainland China, Hong Kong, and Macau through distributors and more than 8,000 online and offline self-operated and retailer points of sale. Perfume Box is the group’s self-operated retail brand, encompassing online stores and offline sales channels, primarily selling perfumes and fragrance-related products directly to consumers in Perfume Box stores. As of September 30, 2025, the group has opened 7 PERFUME BOX offline stores nationwide, covering strategically important Chinese cities such as Shanghai, Shenzhen, and Nanjing. The layout strategy focuses on core areas with strong consumption power and high fashion awareness, aiming to accelerate brand image establishment and market penetration. The group continues to adhere to the “multi-brand + omni-channel” business model, building a widespread sales network and consumer touchpoints through comprehensive brand management and omni-channel sales services. As of September 30, 2025, the group’s membership has exceeded 2.5 million people.

In an increasingly competitive market environment, the group strives to overcome the impact of market price wars on its business through cost optimization, operational efficiency improvements, resource allocation to high-growth areas, and actively introducing diversified brands into the market. For the six months ended September 30, 2025, operating profit increased by 21.2% year-on-year to RMB 164 million, while profit grew by 15.3% to RMB 133 million. China’s “olfactory economy” has developed rapidly in recent years, with the importance of perfumes in consumers’ daily lives continuing to rise. According to Frost & Sullivan data, China’s perfume market is expected to reach approximately RMB 44 billion by 2028 and will maintain steady growth. The group will pursue a dual-track parallel development approach: on one hand, continuing to expand its international brand portfolio, with a focus on introducing more leading international high-end home fragrance and niche fragrance brands. On the other hand, continuing to build a systematic own-brand incubation platform to cultivate a diversified brand matrix with market competitiveness. Its stock price has been consolidating between HK$1.83 and HK$2.25 for nearly half a year. If it confirms a breakout above HK$2.25, it could target HK$2.5. (I do not hold the aforementioned stock)

Strategy:

Buy-in price: HK$2.15, target price: HK$2.5, stop-loss price: HK$2

|

China Life(2628 / 601628)

Analysis:

China Life Insurance (hereinafter referred to as "CL") is a leading enterprise in the domestic life insurance industry and the largest life insurance company in China. It has the most extensive distribution network in China consisting of insurance marketers, group insurance salesmen and professional and part-time agencies. The controlling shareholder of CL Group is the Ministry of Finance of China.

In the first three quarters of 2025, CL recorded revenue of 537.9 billion yuan, up 25.9% yoy; net profit attributable to the parent company was 167.8 billion yuan, up 60.5% yoy; net assets attributable to the parent company reached 625.83 billion yuan, an increase of 22.8% from the beginning of the year; the weighted average return on net assets was 29.3%, up 9.3% yoy; new business value under comparable model grew by 41.8% yoy; and the annualized total investment return was 6.4%, up 1.0 percentage point yoy. Driven by significant investment gains, total investment returns in Q3 2025 surged 73.3% yoy, while the three-quarter total investment returns reached 368.551 billion yuan, marking a 41.0% yoy increase. Looking ahead, with the trend of continuously increasing the proportion of equity allocation in the secondary market, the high elasticity value of the company's performance is expected to emerge.

Strategy:

Buy-in price: HK$ 27.75, target price: HK$31.4, stop-loss price: HK$25.8

Buy-in price: RMB 45.3, target price: RMB 51.2, stop-loss price: RMB 42.1

|

|

Investment SummaryFirst Half Profit of HK$3.65 Billion, Essentially Flat

According to Cathay Pacific Airways(CX) FY2025 interim results, it recorded revenue of HK$54.309 billion (HKD, the same below), a yoy increase of 9.5% for the first half of the year. However, profit growth was weak, primarily due to pressure on passenger yield and the expanded losses of its low-cost subsidiary. Net profit amounted to HK$3.651 billion, with a yoy increase of just 1.1%. Basic earnings per share (EPS) for ordinary shares were 56.7 Hong Kong cents, with a dividend of 20 Hong Kong cents per share, representing a dividend payout ratio of 35%. This marks the second consecutive year of interim dividends since the pandemic recovery.

Strong Recovery Momentum in Business Indicators, but Yield Falls from High Levels

During the reporting period, yoy experienced strong recovery momentum in its business volume. Passenger capacity (available seat kilometres, ASK) grew by 26.3% yoy, and revenue passenger kilometres (RPK) surged by 30.0%. The number of passengers carried reached 13,600 thousand, and the passenger load factor increased by 2.4 percentage points to 84.8%, higher than the pre-pandemic level of 84.2%.

As global capacity supply recovered, market competition intensified, and ticket prices retreated from historical highs. yoy's unit revenue per passenger kilometre (yield) dropped sharply by 12.3% yoy to 60.4 Hong Kong cents (still higher than the pre-pandemic level of 54.9 Hong Kong cents), with particularly large declines of 17.5% and 14.3%, respectively, on routes to the Americas and North Asia. Additionally, the company expanded its long-haul network and increased low-yield routes, which further diluted overall yield levels. This led to revenue growth being offset by pricing pressure. The group's passenger service revenue was HK$37.21 billion, a 12.7% yoy increase, but the growth rate was slower than the increase in passenger volume.

In the cargo sector, although tonnage increased by 11.4%, the cargo load factor declined by 1.3 percentage points yoy to 58.6%, and yield decreased slightly by 3.4% to HK$2.59 (still higher than the pre-pandemic level of HK$1.88). The company's diversified layout and adjustments to its global network helped it cope with the changes, easing the groups pressure. The group's passenger stable, growing by 1.2% yoy to HK$12.76 billion.

Hong Kong Express, a subsidiary, faced challenges due to a decline in demand for Japanese tourism caused by earthquake rumors, as well as the impact of a new route cultivation period. Additionally, intensified competition in the low-cost market and falling ticket prices on short-haul routes negatively affected performance. Hong Kong Express' passenger yield dropped by 21.6% yoy, and its pre-tax profit turned into a loss of HK$524 million (compared to a profit of HK$66 million in the same period last year). Additionally, the share of profits from associates (mostly from its stake in Air China) recorded a loss of HK$180 million, though this represented a reduction in losses by HK$160 million yoy, partially offsetting the operational pressures from the subsidiary. Falling Fuel Prices Benefit Costs, Unit Costs Diluted

According to the consolidated financial statements, yoy's cost structure for the first half of 2025 showed the following characteristics: fuel costs benefitted from a 14.3% drop in fuel prices, rising only 3.5% yoy, which led to an 11.0% decrease in fuel cost per ATK. Non-fuel costs, driven by expanded capacity, increased by 14.2% yoy to HK$33.71 billion. Employee costs, onboard service costs, and ground service costs grew by 20.7%, 32%, and 23%, respectively, reflecting increased manpower and higher route and maintenance expenses.

The expansion of capacity helped dilute unit costs, with unit ATK costs decreasing by 4.1% yoy and unit non-fuel costs dropping by 0.9%. However, the relative rigidity of costs, the pressure of new route cultivation periods, and the decline in unit yields weakened marginal profitability.

Other expenses showed a slight increase, with net financial expenses growing by 1.5% yoy, while aircraft depreciation and rental expenses decreased by 6.9%, reflecting the fleet optimisation effects. Fleet Efficiency Improvements and Cost Optimisation will be the Key ConcernIn its interim report, yoy highlighted the successful integration with Hong Kong International Airport's three-runway system, becoming one of the first base carriers to achieve full runway coordinated operations. This significantly improved its flight punctuality rate to 92.3%. As of mid-2025, yoy's fleet comprised 234 aircraft, and it plans to purchase 14 more Boeing 777-9 aircraft to strengthen its long-haul network, with expected deliveries by 2034 or earlier, further enhancing its long-range capacity.

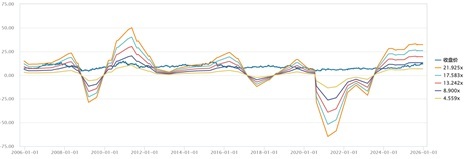

From July to October 2025, yoy continued to see strong passenger demand, with the cumulative number of passengers reaching 27,000 thousand, a 26.1% yoy increase. In October, the monthly load factor rose to 86%, a new high for the period, driven by holidays and business activities such as National Day, Mid-Autumn Festival, and the Canton Fair. In terms of cargo, the cumulative tonnage from July to October grew by 7.6% yoy, with October cargo tonnage surpassing 150 thousand tonnes, a 12% increase from the previous month. The "Cathay Fresh Cargo" and "Cathay Priority Cargo" services saw strong demand, supporting cargo resilience. Hong Kong Express' passenger volume in October increased by 32% yoy, with capacity and demand growing in sync, showing the initial success of network diversification. With fleet efficiency improvements and cost optimisation, along with strong Christmas season bookings, profitability in the second half is expected to recover. However, the sustainability of demand recovery on Japanese routes remains to be observed. Investment thesisWe revised the EPS forecast of Cathay to be HK$1.20/1.40/1.63 in 2025/2026/2027. Based on the revised financial forecast, we lift target price to HK$12.6 for the Company, equivalent to 2025/2026/2027E 10.5/9.0/7.5 x P/E, the Accumulate rating. (Closing price as at 11 December) CX's P/E trend

Source: wind, Phillip Securities Hong Kong Research CX's P/B trend

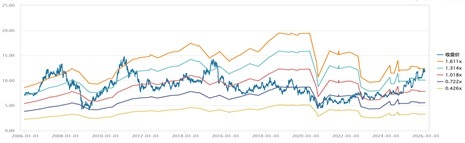

Source: Company, Wind, Phillip Securities Hong Kong Research RiskSurging oil price

Unfavorable Exchange fluctuations

Weaker Demand affected by economy

Fiercer ticket competition

War, Epidemic, etc Financials

(Closing price as at 11 December 2025) Click here to download PDF version...

| Recommendation on 16-12-2025 | | Recommendation | Accumulate (Downgrade) | | Price on Recommendation Date | $ 11.790 | | Suggested purchase price | N/A | | Target Price | $ 12.600 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2025 Phillip Securities (HK) Ltd. All Rights Reserved.

|