|

KUAISHOU-W(1024)

Analysis:

Kuaishou continues to advance its AI strategy by expanding scenario-based AI applications across various businesses. This not only empowers value creation in each business segment but also drives improvements in organizational infrastructure efficiency, delivering high-quality operational and financial performance. In the third quarter of 2025, the Kuaishou app’s average daily active users exceeded 416 million, marking a new historical high for three consecutive quarters. Average daily time spent per daily active user reached 134.1 minutes, with total user time spent increasing 3.6% year-on-year. Total revenue for the quarter grew 14.2% year-on-year to RMB 35.6 billion, with core commercial revenue—including online marketing services and other services primarily from e-commerce—rising 19.2% year-on-year. Adjusted net profit reached RMB 5.0 billion, up 26.3% year-on-year, achieving an adjusted net profit margin of 14%, demonstrating strong operating leverage and effective cost control.

In terms of Kling AI, the group has continuously enhanced the quality of its foundational models and developed more innovative features to meet creators’ diverse needs, building a one-stop creative productivity platform that enables everyone to tell great stories with AI. At the same time, through ongoing engineering innovations, the new model has reduced video generation inference costs, lowering the per-video generation cost for creators by nearly 30% and further strengthening Kling AI’s overall cost-performance advantage. As of January 2026, Kling AI’s monthly active users have surpassed 12 million, with its annualized recurring revenue (ARR) in December 2025 reaching US$240 million; daily revenue in January 2026 grew approximately 30% month-on-month.

In the e-commerce business scenario, the group launched the end-to-end generative retrieval architecture OneSearch, achieving more precise product matching and optimized user experience, which drove an nearly 5% increase in search order volume on the mall. The application of OneRec in e-commerce scenarios contributed to a high single-digit GMV uplift in the information flow (Feed) of the e-commerce mall during the third quarter of 2025. In the live streaming business scenario, leveraging Kling AI’s capabilities, the group introduced the AI All-Things Gift customization feature, generating highly personalized real-person image gift effects that enhance user interaction and willingness to pay.

The group continues to deepen its presence in overseas markets, focusing on targeted advertising to high-value user groups and strengthening deep connections between premium platform content and core users. In the core overseas market of Brazil, user acquisition costs declined year-on-year while maintaining stable daily active user numbers, with average daily time spent per daily active user continuing to grow year-on-year. In the online marketing business, the group has continuously strengthened business resilience by actively expanding into diverse marketing client industries and improving precision matching and conversion efficiency throughout the overall marketing chain, gradually unlocking the commercialization potential of various user groups. Meanwhile, the Brazil e-commerce business has continued to improve subsidy efficiency and operational efficiency, achieving healthy year-on-year growth in transaction scale and order volume while strictly controlling ROI.(I do not hold the above stock).

Strategy:

Buy-in Price: $81.80, Target Price: $89.80, Cut Loss Price: $77.50

|

HAITIAN FLAVOUR(603288/3288)

Analysis:

The company is a leading condiment enterprise in China. Its main products include soy sauce, sauce, oyster sauce, cooking wine, vinegar and sauce, chicken essence, chicken powder, beancurd and other major series of more than 300 specifications, with an annual output value of more than 10 billion yuan, of which soy sauce accounts for the largest proportion, above 50%. In the first three quarters of 2025, the Company reported revenue of 21.628 billion yuan, a yoy increase of 6.02%; net profit attributable to the parent company reached 5.322 billion yuan, growing by 10.54% yoy. The profit growth rate significantly outpaced revenue, reflecting the effectiveness of cost optimization and the structural upgrade of high-margin product categories. In the third quarter of 2025, the gross profit margin reached 39.63%, up 3.02 percentage points yoy, primarily driven by declining prices of raw materials such as soybeans and packaging materials, along with improved smart manufacturing efficiency. Leveraging competitive advantages in scale, R&D, distribution channels, and brand strength, the Company expanded into new categories to drive growth: in the first three quarters of 2025, revenue from "other categories" such as vinegar, cooking wine, and dressing reached 7.47 billion yuan, growing 13.4% year-on-year and accounting for 34.6% of total revenue. Online channels grew at a rate of 32.11%, becoming a key breakthrough. Meanwhile, the company entered overseas markets through its sub-brand "Dianqu," focusing on Southeast Asia, Europe, and America, while promoting product localization, with the goal of increasing overseas revenue to 15% within three years.

Strategy:

Buy-in Price:¥35.0,Target Price: ¥39.70,Cut Loss Price:¥32.0

Buy-in Price:HK$30.80,Target Price: HK$34.90,Cut Loss Price:HK$28.30

|

|

JNMPT (000700 CH) - Bumper leader, entering the field of humanoid robots

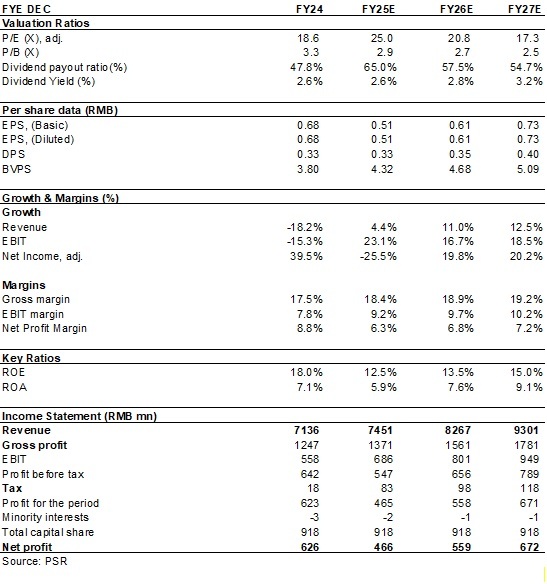

Company profileJiangnan Mould & Plastic Technology Co., Ltd. is a leading automotive parts supplier in China, with its main business focusing on the R&D, production and sales of automotive exterior systems such as bumpers and lightweight components. The Company has an annual production capacity of over 6 million sets of automotive bumpers, with production bases in Wuxi, Shanghai, Shenyang, Wuhan, Yantai, and Mexico, and R&D centres located in Beijing, Shanghai, and Jiangyin. Its associate company, BMPT, has established production bases in Beijing, Hefei, Chongqing, Chengdu, and Zhuzhou. In 2024, the Company recorded revenue of RMB7,136 million, down 18.18% yoy, and net profit of RMB626 million, up 39.46% yoy. Investment SummaryShort-Term Performance Pressure in FY2025Q3

In the first three quarters of 2025, the Company achieved revenue/net profit attributable to the parent company/net profit attributable to the parent company excluding non-recurring items of RMB5,107 million/RMB375 million/RMB346 million (RMB, the same below), representing yoy growth of -2.7%/-30.42%/-25.12%, respectively. Sales gross margin was 19.57%, up 1.15 ppts yoy. The sales volume growth from emerging EV makers helped offset the decline in sales from premium car clients, leading to Company revenue growth outperforming the industry average.

In Q3 alone, the Company recorded revenue of RMB1,708 million (up 0.52% yoy, down 5.08% qoq), net profit attributable to the parent company of RMB82 million (down 54.74% yoy, down 43.63% qoq), and net profit attributable to the parent company excluding non-recurring items of RMB104 million (down 22.7% yoy, down 0.7% qoq). Q3 gross margin was 19.6% (up 0.8 ppts yoy, up 1.2 ppts qoq), and net profit margin was 4.8% (down 5.8 ppts yoy, down 3.3 ppts qoq). Gross margin showed signs of recovery, while the decline in net profit margin was mainly due to foreign exchange losses and reduced investment income.

Coverage of High-Quality Clients and New Orders Laying the Foundation for Future Growth

The Company has a strong client portfolio, with core customers covering global premium brands and new energy vehicle manufacturers. Key clients include: BMW, Beijing Benz, SAIC Audi, a well-known North American EV maker, SAIC-GM, SAIC Volkswagen, Chery Jaguar Land Rover, Volvo, BYD, Geely, Great Wall, DFPSA, NIO, Li Auto, and XPeng. While maintaining its advantages among premium carmakers, the Company has actively expanded into the NEV segment, tapping into incremental markets both domestically and internationally. The newly secured orders provide a solid foundation for future growth.

In January 2025, the Company received project nominations for exterior parts for three models from a well-known domestic NEV client. The project is expected to start mass production in May 2026, with a 3-year lifecycle and estimated total sales of RMB1.23 billion to RMB1.32 billion.

In April and July 2025, the wholly owned subsidiary, Shenyang Minghua, received nominations for exterior part projects from a leading premium car client. These projects are expected to commence mass production in April 2027 and January 2028, respectively, with lifecycles of 8 and 5 years, and estimated total sales of RMB2.07 billion and RMB2,044 million, respectively.

In July 2025, Mexico Minghua received a nomination for an exterior part project from a well-known North American EV maker. The project is scheduled to begin mass production in January 2026, with a 5-year lifecycle and estimated total sales of RMB1,236 million. Seizing Industry Opportunities and Entering the Humanoid Robot SegmentOn 16 December 2025, the Company announced that it had signed a component procurement framework agreement with a domestic robotics company and recently received a small-batch purchase order for exterior covering parts of humanoid robots from the client. This small-batch order marks a key milestone in the Company's entry into the humanoid robot segment, signifying that its manufacturing processes and quality assurance system have gained client recognition. It also lays the groundwork for acquiring more robot clients and expanding market share in the future. Investment Thesis & ValuationWhile the Company's core business---automotive bumpers---continues to develop steadily and secure new project nominations, it is simultaneously expanding into the new field of humanoid robotics, presenting potential for business growth.

As analyzed above, we expected diluted EPS of the Company to RMB 0.51/0.61/0.73 of 2025/2026/2027. And we accordingly gave the target price to 16.45, respectively 27x P/E for 2026. "Buy" rating. (Closing price as at 29 January) Historical P/E Band

Source: Wind, Company, Phillip Securities Hong Kong Research Financials

(Closing price as at 29 January)

Click here to download PDF version...

| Recommendation on 30-1-2026 | | Recommendation | BUY (Initiation) | | Price on Recommendation Date | $ 12.680 | | Suggested purchase price | N/A | | Target Price | $ 16.450 |

| |

|

|

|

|

| Stock Code |

H share

Price |

A share

Price |

H share

discount |

| | | |

|

Information contained herein is based on sources that Phillip Securities (Hong Kong) Limited and/or its affiliates ( the “Group”) believe to be accurate. The Group does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The Group (or its employees) may have interests in relevant investment products. For details of different products’ risks, please view the Risk Disclosures Statement on http://www.phillip.com.hk.

If you DO NOT wish to receive further marketing emails from us, please click HERE to opt-out.

版權所有, 翻印必究。

Copyright(C) 2026 Phillip Securities (HK) Ltd. All Rights Reserved.

|